Ekonomska profesija nosi zelo velik del krivde glede skepse glede podnebnih sprememb. Prvi in splošni problem ekonomske profesije pri soočanju z ekonomiko podnebnih sprememb je, da prevladujoča neoklasična ekonomska paradigma sploh ni primerna za obravnavo problema klimatskih sprememb.

Na kratko, neoklasična ekonomija temelji na optimizacijskem obnašanju racionalnih posameznikov, pri čemer so odločitve sprejete na ravni zadnjega, mejnega posameznika. Tako kot naj bi bila optimalna višina plače določena na ravni mejne prouduktivnosti zadnjega delavca, ki je dobil službo, tako naj bi se odločitev glede ravnanja v primeru podnebnih sprememb zgodila na podlagi preračuna stroškov in koristi zadnjega racionalnega subjekta. Se pravi, ko bodo podnebne spremembe postale tako drastične, da bodo prinesle neto negativne učinke mejnemu subjektu. Kar pomeni, da lahko počakamo, da se bo planet segrel za 3 stopinje in da bodo v tistem trenutku subjekti spoznali, da je njihova ekonomska računica zdaj postala negativna. Do takrat pa lahko počakamo.

Mnogi, tudi nekateri ugledni ekonomisti (kot sta Olivier Blanchard in Larry Summers) ter uradniki v centralnih bankah, so zagnali paniko ob porastu tekoče inflacije po koncu tretjega vala epidemije. Razlog naj bi bil premočan stimulus, ki ga je Bidenova administracija v okviru $1,900 milijard težkega paketa, namenila za zagon ameriškega gospodarstva. Vendar pa, kot sem pisal že pred časom, ta panika ni bila upravičena. Porast inflacije je bil namreč globalni fenomen, ne samo ameriški. Razlogi pa se skrivajo predvsem v ozkih grlih v dobavnih verigah, ki ne morejo dobaviti dovolj surovin in komponent po ponovnem zagonu gospodarstev, predvsem v avtomobilski industriji in gradbeništvu, nato v porastu cen energentov ter v prebuditvi potrošniškega povpraševanja, predvsem po potovanjih in turističnih aranžmajih. Vsi ti cenovni šoki so tranzitorne, prehodne narave in nimajo trajne osnove.

Ekonomisti Cecilia Rouse, Jeffery Zhang, and Ernie Tedeschi v Svetu ekonomskih svetovalcev (CEA) predsednika Josepha Bidena so pripravili zelo dober pregled zgodovinskih epizod visoke inflacije. Ugotavljajo, da je bila vsaka specifična in nobena primerljiva s sedanjo

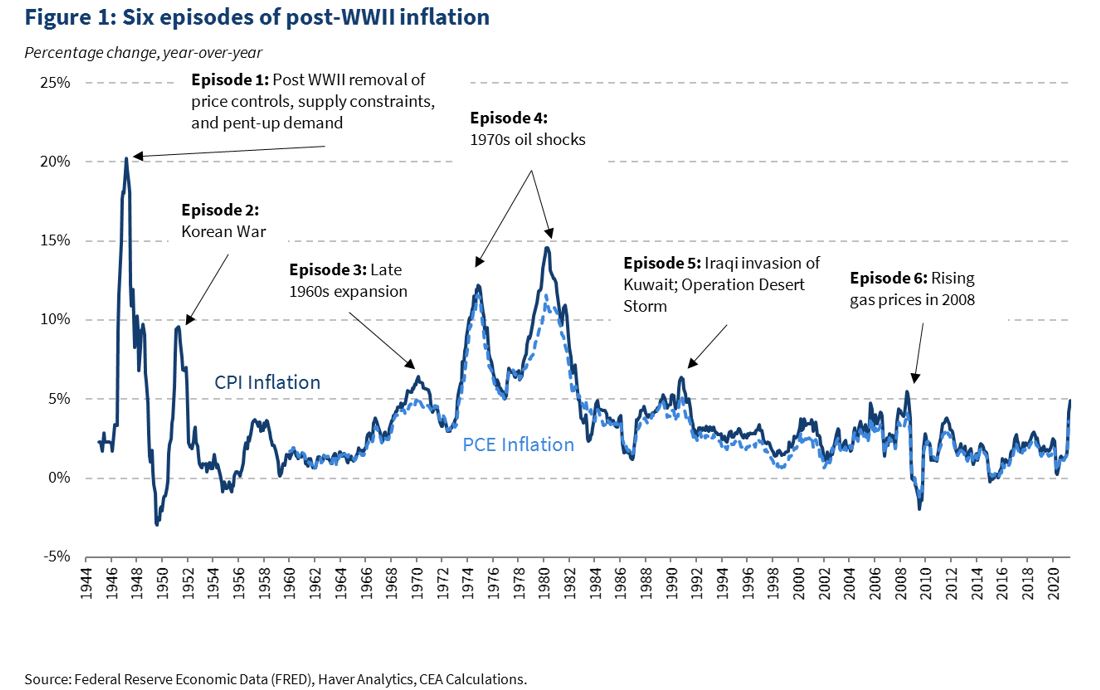

In this blog post, we examine previous periods of heightened inflation and see what they can teach us about inflation in 2021. Figure 1 shows a time series of two commonly used measures of inflation: Consumer Price Index(CPI) and Personal Consumption Expenditures (PCE). Since World War II, there have been six periods in which inflation—as measured by CPI—was 5 percent or higher. This occurred in 1946–48, 1950–51, 1969–71, 1973–82, and 2008. We first present a high-level overview of each of the previous six inflationary episodes and then turn our attention to the years following World War II—an episode that has strong similarities to what is occurring in the current environment.

Six Inflationary Episodes

Episode 1: July 1946–October 1948

Milton Friedman and Anna Jacobson Schwartz (1980)observe that World War II ushered in a period of inflation comparable to the inflationary episodes that occurred during the Civil War and World War I.[1]Prices also surged after World War II ended. In 1947, inflation jumped to over 20 percent, as shown in Figure 1.According to the Bureau of Labor Statistics (BLS), the rapid post-war inflationary episode was caused by the elimination of price controls, supply shortages, and pent-up demand.

Episode 2: December 1950–December 1951

The Korean War started in June 1950 and hostilities ceased in July 1953. Prices had been declining in the months prior to the war because of a mild recession, but rebounded with thereturn to wartime status. Demand jumped as households—reminded of rationing and supply shortages during World War II—rushed to purchase goods. In addition, some consumer production shifted back to military material, and price controls were reinstated. Notably, in the post-Korean War years, when price controls were removed, inflation did not jump the way it did following World War II.

Episode 3: March 1969–January 1971

This inflationary episode was caused by a booming economy, which increased prices. From 1965 through 1969, for instance,real quarterly GDP growthaveraged 4.8 percent at an annual rate. Inflation fell after President Nixon instituted a freeze on wages and prices.

Episode 4: April 1973–October 1982

In the 1970s, the United States experienced its longest stretch of heightened inflation because of two surges in oil prices. The first was caused by an oil embargo implemented by the Organization of Arab Petroleum Exporting Countries (OPEC). The second surge was caused by a decline in oil production due to the Iranian Revolution and the Iran–Iraq War. In 1979, Paul Volcker became the Chair of the Federal Reserve and began his well-known campaign of hiking interest rates to bring inflation under control.

Episode 5: April 1989–May 1991

This fifth inflationary episode occurred when Iraq invaded Kuwait, leading to the first Gulf War. The price of crude oil increased significantly due to heightened uncertainty, leading to a short bout of high inflation.

Episode 6: July 2008–August 2008

In 2008, the CPI rose above 5 percent for two months due to skyrocketing gas prices. One barrel ofWest Texas Intermediate crude oilcost more than $140 in July 2008 compared to $70 just a year earlier.

Pent-up demand and supply chain disruptions

The three most recent inflationary episodes were largely a function of oil shocks; in contrast, pandemic price dynamics have not been primarily driven by oil supply, though we continue to closely monitor ongoing energy price behavior. In addition, oil prices have a different relationship with the American economy than in the past, as the United States became a net annual petroleumexporterin 2020 anduses an increasing share of renewablesfor its energy consumption. The episode from 1969–71 is also different because the economy was growing quickly at nearly 5 percent per year for half a decade, which is not the case at present. The episode during the Korean War is a closer comparison, as households rushed to buy goods in anticipation of a supply shortage. While households are consuming more today in the aftermath of COVID due to pent-up demand, they are not hoarding in anticipation of a supply shortage. Also, while many industries face supply constraints, there is not a broad push to shift production away from consumer goods.

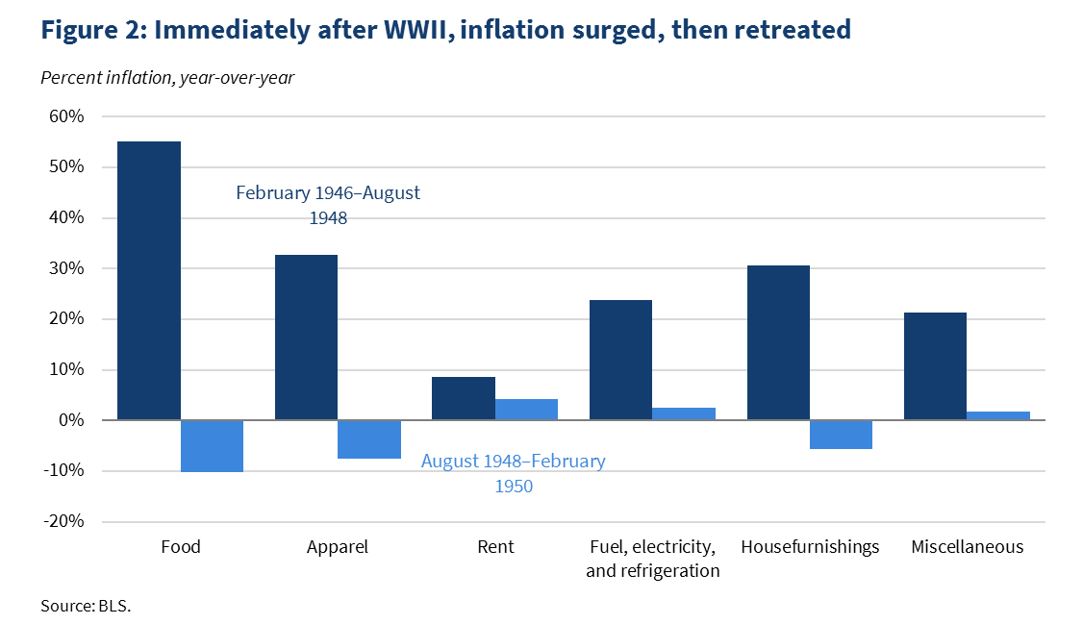

The period right after World War II potentially provides the most relevant case study, as the rapid post-war inflationary episode was caused by the elimination of price controls, supply shortages, and pent-up demand. Figure 2 shows the change in prices in the five years following World War II.

Not surprisingly, supplies were running low or were exhausted entirely during the war. Families had trouble buying cars and household appliances because they were essentially unavailable.According to the BLS, “[by] 1943, many durable goods, such as refrigerators and radios, were also dropped from the [CPI] as their stocks were exhausted.” Instead of focusing on consumer or industrial durable goods, manufacturing capabilities were concentrated on military production. Today’s shortage of durable goods is similar—a national crisis necessitated disrupting normal production processes. Instead of redirecting resources to support a war effort, however, manufacturing capabilities were temporarily shut down or reduced to avoid COVID contagion.

Pent-up demand also put upward pressure on prices following World War II. During the war, households were limited by thewidespread rationing of consumer goods. The government rationed foods such as sugar, coffee, meat, and cheese as well as durable goods like automobiles, tires, gasoline, and shoes. Personal savings increased significantly and were spent soon after the war ended. Between 1945 and 1949,a population of roughly 140 millionAmericans purchased20 million refrigerators, 21.4 million cars, and 5.5 million stoves. During COVID, businesses were shut down and households mostly stayed indoors. Expenditures on entertainment, dining at restaurants, and travel fell dramatically (from March 20–26, 2020, the entire U.S. box office made roughly$5,000 as compared to $200 millionduring the same week in 2019). Personal savings increased during the pandemic as well, and nowretail salesare booming.

One substantial difference between the inflation dynamics of World War II and today is that price controls were a wartime policy tool that were not implemented during COVID. Those price controls reduced the price level 30 percent below what it would have been otherwise, according to PaulEvans (1982). When the caps were lifted in 1946, prices climbed significantly. For example, food prices alone rose 13.8 percent in Julyafter food price controls expired on June 30th.

According to BenjaminCaplan (1956), the inflationary episode after World War II ended after two years as domestic and foreign supply chains normalized and consumer demand began to level off. (Caplan also observes that private fixed investment started to decline, which contributed to the decline in prices and caused the economy to fall into a mild recession, with real GDP declining by 1.5 percent).

The role of expectations

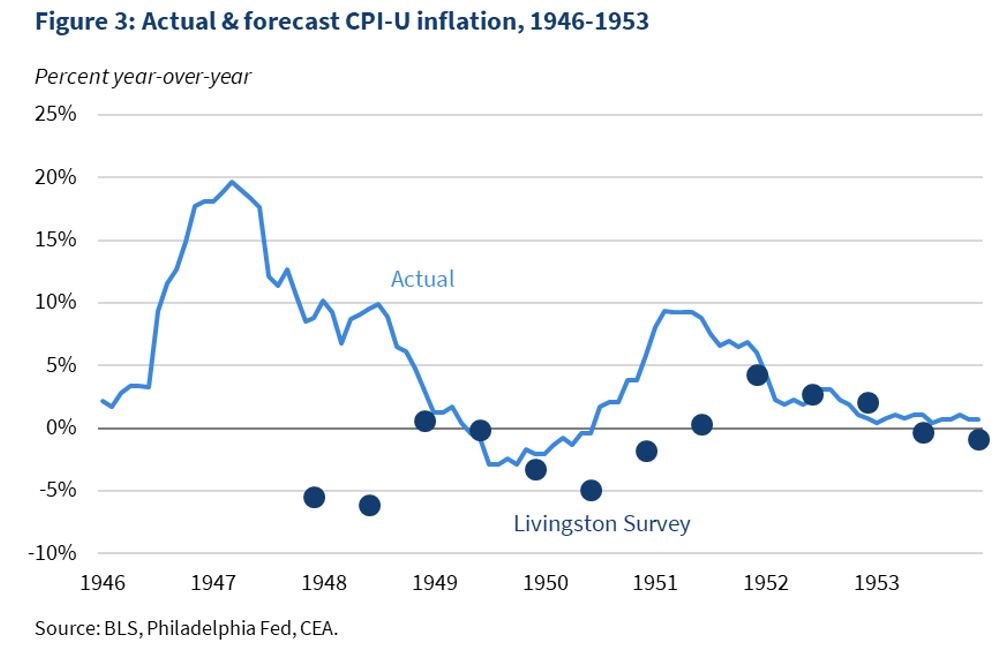

If actual inflation is affected by inflation expectations—and if expectations are in part formed by recent experiences (what economists call “adaptive” expectations)—then one risk is that transitory supply constraints and pent-up demand could have more persistent effects by raising longer-run expectations of inflation. On the other hand, businesses and consumers may “see through” supply disruptions and not change their longer-run expectations significantly.

The United States of 1946 did not have nearly as many ways of gauging inflation expectations as we do today, but the limited data we have suggest Americans at the time were aware of the transitory nature of their inflationary episode. The Livingston Survey of economic forecasters—begun in June 1946 by a columnist for the Philadelphia Inquirer and run today by the Federal Reserve Bank of Philadelphia—shows that forecasters expected low or even negative inflation over the 1947–1951 period (see Figure 3 below). While actual inflation often came in higher during this time—and early expectations surveys like Livingston should be interpreted with caution due to difficulties in knowing how respondents were calibrating their expectations—respondents did not appear to persistently mark up their short-run inflation forecasts due to the transitory inflation episodes of World War II and the Korean War.

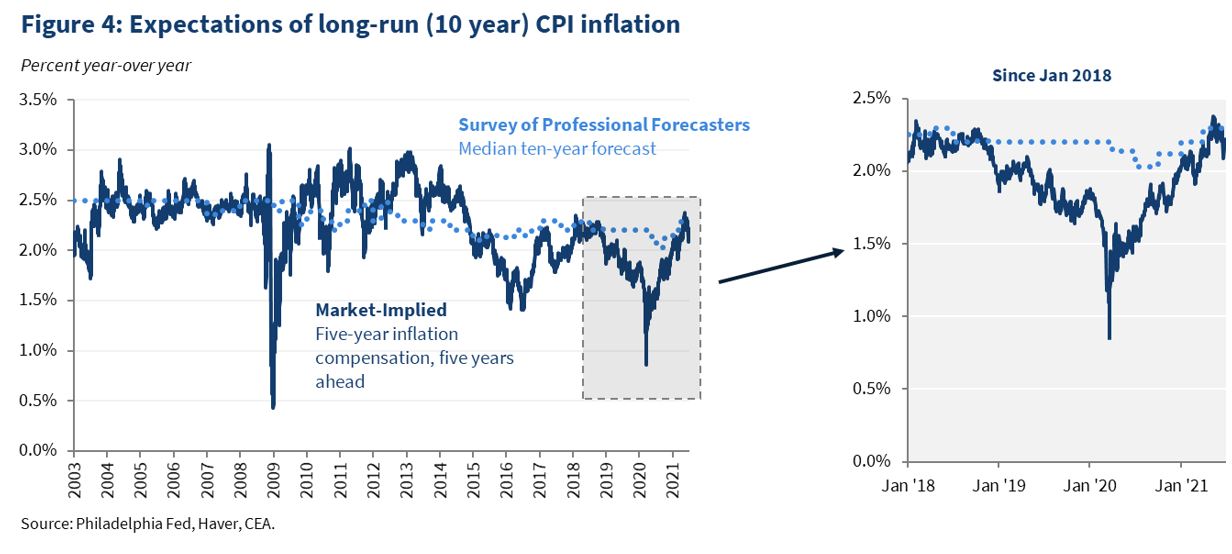

Today, we have metrics measuring longer-run inflation expectations in the form of surveys and market-based measures. If transitory inflation pressures were spilling over into longer-run expectations, we would anticipate seeing these measures rise to historically high levels. However, as Figure 4 below shows, both market-based measures like the five-year, five-year inflation break-evens, and survey-based measures like the ten-year expectations in the Survey of Professional Forecasters, have broadly recovered from pandemic-lows to levels more consistent with pre-pandemic expectations.

Conclusion

No single historical episode is a perfect template for current events. But when looking for historical parallels, it is useful to concentrate on inflationary episodes that contained supply chain disruptions and a spike in consumer demand after a period of temporary suppression. The inflationary period after World War II is likely a better comparison for the current economic situation than the 1970s and suggests that inflation could quickly decline once supply chains are fully online and pent-up demand levels off. The CEA will continue to carefully gauge the trajectory of inflation.

Ko govorimo o normalni državi, ki jo zaslužimo in ki jo želimo nazaj, bi morali v resnici razumeti, kaj je kvintesenca normalne države. Po mojem je to delovanje v smislu varovanja javnega dobrega. Torej stalno doseganje, da se pri vsaki temi vidi, da se je izbrala smer in cilji, ki morda niso nikomur 100% všeč, ampak hkrati nismo nikogar ignorirali in da nihče ni potegnil krajšega konca. Kar pomeni, da mora imeti politični akter najprej pri sebi definirano, kakšne koncepte prepozna kot koncepte javnega dobrega. In težava je, da pri naših političnih akterjih umanjkajo koncepti.

Za razumevanje, kaj sem mislila s »konceptom«, sem poiskala sedaj žezgodovinski pogovor med Alijem Žerdinom in Janezom Markešem iz davnega začetka marca 2020(ne vem, zakaj ga na YT ni) . Ob vseh kislih nasmeških, ki vam bo tale pogovor vzbudil, opozarjam na tisto, kar Janez Markeš razlaga od 3. do 5. minute, ko sesuva idejo takrat še kandidata za ministra za obrambo Mateja Tonina. Slednji se je lani zavzemal za ukinitev profesionalne vojske in uvedbo naborništva, kamor bi vključil tudi vardiste (ojoj). Markeš tule genialno poantira v smislu: če država pričakuje, da bo za njo nekdo odložil leto svojega življenja, potem mora ta ista država tudi nekaj nuditi tej generaciji, recimo zaposlitev, šolanje, možnosti osamosvojitve od staršev. Skozi pogovor potem Markeš še sarkastično navrže, da je »Tonin pokazal, kakšen je njegov koncept. Nima ga.«

V zadnjem času smo lahko v več medijih prebrali objavo statističnega urada o številu oseb pod pragom revščine v Sloveniji. Podatek, da v Sloveniji pod tem pragom živi kar 243 tisoč ljudi (podatki za leto 2019), je bil za večino presenetljiva in tudi skrb zbujajoč. Da je po 30 letih samostojne Slovenije kar četrt milijona ali 12 % vseh prebivalcev opredeljenih kot revnih, vsekakor ni bil cilj osamosvojitve in še manj pričakovanj. Posebno ob predpostavki, da nekdaj (v bivši državi) revnih pač ni bilo.

Takšne informacije se seveda potem hitro porabijo za tekoče politične potrebe, za iskanje krivcev in kazanje s prstom ter za kak udaren članek v medijih – seveda pa se ne odrazijo v kaki posebni aktivnosti ljudi in institucij odgovornih za to področje. Temu je seveda razlog tudi v tem, da ta kazalec vseeno ne pove, koliko ljudi je dejansko revnih, temveč je rezultat izračuna dohodkov po posebni metodologiji izračuna praga revščine. Torej nivoja dohodkov za katere se v skladu mednarodno določeno metodologijo opredeli, da so meja za “prehod” v revščino (v tveganje revščine).

Namen članka je zato nekoliko podrobneje pojasniti, kaj pomeni teh 240 tisoč “revnih” Slovencev in kakšen je ta kazalec socialne politike v primerjavi z drugimi državami Evropske Unije.

V oddajiNa tretjem, je Robert Golob ponovil ničkolikokrat ponovljeno neresnično trditev, da solarne “samooskrbe” ne plačujemo sosedje. Pa poglejmo, kako je s tem v resnici.

Hm, enako bi se lahko vprašali glede ideološke in kadrovske naslednice slovenske komunistične partije, t.j. Janševe SDS: je SDS stranka za delovne ljudi ali stranka, ki favorizira kapital?

Seveda je to zgolj retorično vprašanje, saj njeni ukrepi jasno kažejo v smeri favoriziranja kapitala pred ljudmi.

It’s 100 years today since the Chinese Communist Party (CCP) was first formed by just 50 members, mostly intellectuals, but including railway and mine workers. 100 years later to the day, the official membership figure is 95m and there are 4.8m party branches. This is surely the largest political party the world has ever seen. A quarter of the membership is under 35 years; 29% are female, up from 12% in 1949 and over half of members have college degrees (that means half don’t!).

In 2021, is the CCP a party of and for capitalists or of and for workers? The short answer is that it is neither. But the long answer is more complex.

The CCP was led at first by two intellectuals, Chen Duxiu and Li Dazhao, with the help of the Communist International (Comintern). These leaders saw the CCP as the party for the Chinese…

Eden izmed ključnih postulatov makroekonomske revolucije, ki so jo konec 1970-ih let izvedli čikaški makroekonomisti, so bila racionalna pričakovanja. Torej da so subjekti popolno informirani, da vidijo vnaprej v daljno prihodnost in da se ne motijo sistematično. Znotraj tega pa seveda, da imajo menedžerji racionalna pričakovanja glede inflacije: spremljajo ukrepe centralne banke in natanko predvidijo njihove učinke na inflacijo, zato vedno vedo, kakšna bo prava inflacija v prihodnosti in se glede nje se ne motijo sistematično.

No, ta zgodba je seveda samo pravljica. Pravljica iz učbenikov makroekonomije. V resnici menedžerji in še manj običajni ljudje ne spremljajo ukrepov centralne banke in jih ne razumejo in se jim zato tudi sanja ne, kakšna bo prava stopnja inflacije jutri, čez en mesec, čez leto dni ali čez 5 let. Sistematično se motijo glede nje. Sistematično jo precenjujejo. To kaže tudi zadnja empirična študija, ki so jo naredili ekonomisti Bernardo Candia, Olivier Coibion, and Yuriy Gorodnichenko v “The Inflation Expectations of US Firms: Evidence from a New Survey“. Dve tretjini menedžerjev sploh ne ve, kakšen je inflacijski cilj ameriške centralne banke.

Pred dvema letoma sem zaradi komplikacij z antibiotiki pristala na hematološki kliniki UKC Ljubljana. Antibiotik, ki sem ga jemala, je imel zelo redek stranski učinek (1:10.000) krvnih zapletov in moj zaplet se je imenoval nevtropenija. Po petih dneh vrhunske obravnave, ki je vključevala sodelovanje strokovnjakov hematološke in infekcijske klinike, sem šla domov, v šestih mesecih sem svojo krvno sliko popravila. Zdaj imam v kartoteki navedeno, katerih antibiotikov ne smem jemati. Skratka, sem na svoji koži doživela, kaj pomeni, da doživiš redke neželene stranske učinke. Se pač zgodi. Še vedno sem nepopisno hvaležna Flemmingu, da ni počistil laboratorijskega materiala in je posledično iznašel penicilin. Ne pade na misel, da bi kategorično zavračala jemanje antibiotikov, samo z zdravnico sva sedaj bolj pri izbiri zdravila, če je slednje potrebno.

Sem pa v tistih petih dnevih odvrtela vse svoje življenje in vse spomine. Med njimi so bili tudi spomini, ko sem hodila v bolnišnice na obiske. Kako sem se šla leta 1997 poslovit od na smrt bolne prijateljice, pa kako sem dolga leta obiskovala teto in seveda sem podoživela vse situacije, ko sem v bolnišnici obiskovala očeta. Ti spomini so en sladko-grenak koktajl, ki v človeku pušča sledi. Ta koktajl te nauči, da v pogledu bolnega človeka vidiš, če še obstaja iskrica in volja do življenja in te tudi naučijo, da prepoznaš, kdaj te volje ni več. In naučiš se, kako te zmrazi, ko vidiš, da te iskre ni več. In prav je, da človek pusti, da ga tak koktajl formira. Če ne, si preprosto ena navadna reva, ki beži pred življenjem. Ker so lekcije, ki jih je treba osvojiti, če jih ne osvojiš, te počakajo, če ne prej, takrat ko greš prvič takoj za žaro v vrsti pogrebcev.

You must be logged in to post a comment.