Aleš Praprotnik

Glavni ekonomist agencije Standard & Poor’s (S&P) Paul Sheard je pred kratkim objavil dober tekst z naslovom Repeat after me: Banks cannot and do not ‘lend out’ reserves, v katerem na razumljiv in zgoščen način ovrže mit o multiplikaciji kredita in razčiščuje nejasnosti glede tega, kaj ustvarjajo centralne banke, kaj posojajo banke in pomen kvantitativnega sproščanja (QE). Sam sem pred časom že pisal o tej temi, kjer sem navedel citate številnih centralnih bankirjev in ekonomistov (tudi z Banke za mednarodne poravnave) o vlogi centralnobančnih rezerv in ustvarjanju kredita v bankah. Sedaj se njim (ter regulatorjem, kot je npr. bivši šef FSA Adair Turner) pridružuje še glavni ekonomist S&P. Poglejmo si nekatera njegova ključna opažanja:

“Banks lend by simultaneously creating a loan asset and a deposit liability on their balance sheet. That is why it is called credit “creation”– credit is created literally out of thin air (or with the stroke of a keyboard). The loan is not created out of reserves. And the loan is not created out of deposits: Loans create deposits, not the other way around. Then the deposits need a certain amount of reserves to be held against them, and the central bank supplies them …”(str. 7)

…

“This goes against the grain of the usual way of describing bank lending, which suggests that banks “collect” deposits and then “lend them out.” That is not the way it happens at all. In a closed economy (or the world as a whole), fundamentally, deposits come from only two places: new bank lending and government deficits. Banks create deposits when they create loans, as explained above. Governments also create deposits when they run budget deficits because they are putting more money into the public’s bank accounts than they are taking out. This net flow creates new deposits in the banking system, which has its counterpart on the bank’s balance sheet as an increase in reserves” (str. 8)

…

“Central banks don’t constrain the amount of bank reserves they supply. Rather they supply whatever amount of reserves that the banking system demands given the reserve requirements and the amount of deposits that have been created. Why is this? Because modern central banks, in normal times (such as before the crisis and the forays into QE) target a short-term (usually overnight) interest rate in the interbank money market (the market in which banks lend and borrow central bank reserves). They do this by adjusting the amount of reserves on their balance sheet (in the banking system) to ensure that the interest rate is in line with their announced policy rate (the federal funds rate in the case of the Federal Reserve).” (str. 8)

…

“If bank lending increases and the associated increase in bank deposits leads, as it will, to a higher level of minimum required reserves, the central bank will naturally supply those reserves. Otherwise there will be a central bank-induced shortage of reserves, and the overnight interest rate will go up, meaning that the central bank will not be hitting its interest-rate target. Central banks, in normal times, cannot target an interest rate and independently restrict the amount of reserves they supply.” (str. 9)

Učbeniška razlaga, da banke potrebujejo depozite oz. rezerve preden lahko posojajo in da posojajo v skladu z multiplikacijo zaradi rezervne zahteve torej ne drži.

Pravilno razumevanje ‘monetarne mehanike’ in pomena bank ima seveda daljnoročne posledice. Prvič, v veliki krizi kot je sedanja zmanjšuje nerealna pričakovanje glede učinkov monetarne politike (ki naj bi spodbudila posojanje in gospodarsko aktivnost). Drugič, miri iracionalne strahove glede hiperinflacije zaradi QE. Tretjič, kaže, da je bolj učinkovit odziv v krizi fiskalna politika. Četrtič, spodbuja regulatorje k večjemu nadzoru bančnega sektorja. Petič, kaže na to, da je potrebno ustvarjanje kredita (‘credit creation’) na računovodskih knjigah vstaviti v makroekonomske modele.

Michael Kumhof, ekonomist z Mednarodnega denarnega sklada, ki skupaj z Jaromirjem Benesem sam razvija monetarni DSGE model, o monetarni mehaniki pravi:

“Intermediation of course exists … but it is incidental and secondary and it comes after the actual money creation. Banks do not need to attract deposits before they lend money. Rather they create deposits out of nowhere in the act of lending. I’m a former bank manager. I worked for Barclays bank for 5 years. I’ve created those book entries. That is how it works … What happens is … when somebody comes into your bank, as a bank manager … you approve that loan because you think it is a good credit risk, then you enter on the asset side of your balance sheet the loan, which is a claim against this guy and on the liabilities side – at the same time, at exact same time – you create a new deposit. You have created new money because this gives this guy purchasing power to go out and buy something with it. Banks have created money at that point. No intermediation.” (3:04 – 4:15)

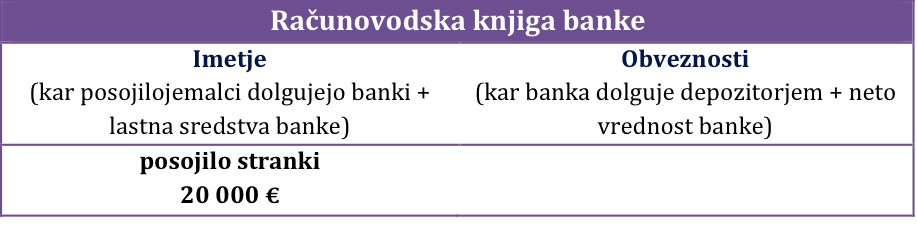

Če proces dejanskega ustvarjanja denarja pokažemo še shematično s preprosto računovodsko knjigo banke, zgleda takole:

Slika 1: Preprost prikaz bančne računovodske knjige in prvega koraka – vpisa zneska posojila na stran imetja

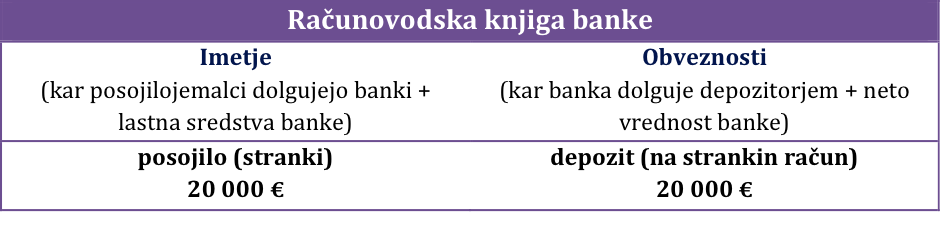

Slika 2: Drugi korak – vpis enakega zneska na stran obveznosti

Slika 2: Drugi korak – vpis enakega zneska na stran obveznosti

Za bolj natančno razlago celotnega procesa (vključno s centralno banko in plačili med bankami) priporočam preprosto in poljudno razlago, ki jo najdete na strani Positive Money.

You must be logged in to post a comment.