…so precej boljše od pričakovanj. In v primerjavi z ameriškimi tudi precej bolj vzdržne. Spodaj je dober vpogled Bena Arisa v ruske javne finance. Koristno je to poznati.

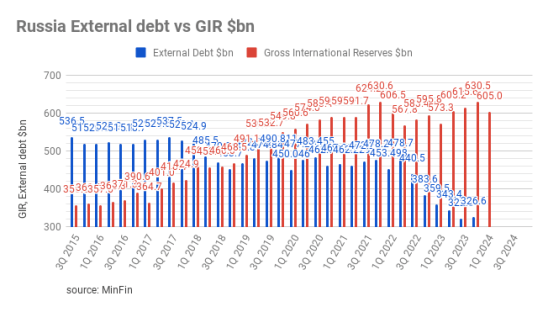

Russia external debt has been falling steadily and reached $326.6bn in December 2023, compared with $322.3bn in the previous quarter and $383.6bn at the end of 2022. It could pay the entire amount off tomorrow – in cash.

The Kremlin has been paying off its external debt. Low external debt means Russia doesn’t need to tap international capital markets so is not vulnerable to any sort of sanctions on bond issues, which are easy to apply and enforce.

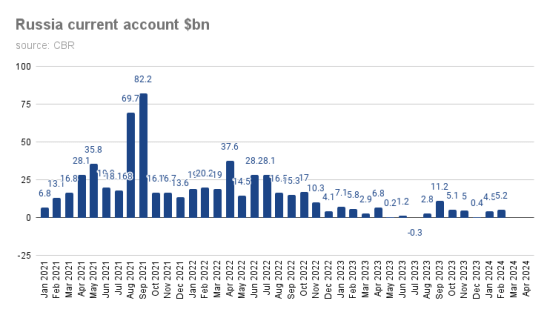

Coupled with Russia’s strong current account surplus, which was up to $5.2bn in February from $4.5bn in January, thanks to high oil prices, Russia can fund itself easily on this profit.

At the same time gross international reserves have been rising and are now hovering around $600bn at the end of the first quarter. Half of these reserves are frozen. About $150bn are in monetary gold (up from $135bn pre-war) and the rest in yuan.

Even counting out the frozen funds, Russia can cover its external debt dollar for dollar with cash, whereas everyone in the West is massively leveraged, including the Ukraine where the debt-to-GDP ratio is almost at 100%.

It is these rock-solid fundamentals – no one else in world has even remotely similar fundamentals – which is the essence of Putin’s Fiscal Fortress. It is a ridiculously strong basis, which means even if the West manages to reduce Russia income from oil and gas exports, it will still have a massive amount of wiggle room. And its ongoing commodity exports to the global south mean that it will continue to enjoy the raw materials subsidy for its economy. Because of their external debt (USA, Italy, much of G7, everyone in Africa and even China) everyone else is a lot more vulnerable to a global slow down. Russia is probably currently the least vulnerable on a macro fundamentals basis.

You must be logged in to post a comment.