Močno povečani nakupi zlata v zadnjih mesecih ter trgovanje z zlatom na Shanghajski borzi nekatere napeljujejo k špekulacijam, da uradni kitajski kupci kopičijo zlato. Špekulacije gredo v smeri, da se Kitajska pripravlja na morebitne sankcije s strani ZDA v primeru eskalacije dogajanja glede Tajvana. Kitajska bi se na podlagi izkušenj letos z zasegom ruskih deviznih rezerv utegnila umikati iz dolarskih imetij in kopičiti zlato.

Druga špekulacija gre v smeri, da se države izvoznice nafte umikajo iz trgovanja v dolarjih in da naj bi petrodolarje počasi izrinilo petrozlato. Bolje rečeno – petrojuan (kot je napovedal kitajski voditelj Xi Ping), saj je zlata mnogo premalo, lahko pa služi kot rezerva pri trgovanju z energenti v drugih valutah. Seveda gre zgolj za špekulacije, na katere pa je treba biti pozoren.

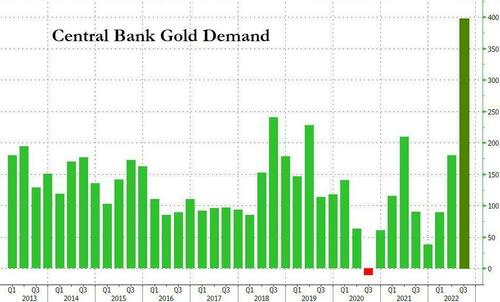

A month ago, we confirmed the identity of the “mystery” gold-buyer who had been suddenly hording the precious metal in recent months.

Specifically, we identified China as the hidden whale buying the barbarous relic when all around them are decrying it’s inflation-hedging help, remarking at the time that for China, the need to find an alternative to dollars, which dominate its reserves, has rarely been greater.

Tensions with the US have been high since measures taken against its semiconductor firms, while Russia’s invasion of Ukraine has demonstrated Washington’s willingness to sanction central bank reserves. In other words, now that the US has shown it is ready to weaponize the dollar, any USD reserves held by the Fed, Western banks or any other counterparty, could and will be promptly confiscated if China does something unpalatable… like invading Taiwan. Which is why China is desperately seeking money without counterparty risk. Here it has just two choices: crypto or gold. For now, it has picked the latter.

…

The TD Securities’ strategist has a few ideas:

- Reserve Currency Ambitions: A contingent of market participants has suggested that gold is gaining market share as a reserve asset. After all, USD valuations have moved to extremes following the build-up in USD cash and associated stagflation hedges. European data surprises are surging with growth expectations on the rise as extremely mild weather helped the region fare with the ongoing energy shock, at the same time as a fast-paced Chinese reopening bolsters rest-of-world growth — factors which are all in support of a cyclical peak in USD value. Most importantly, however, is the rise in perceived sanctions risks associated with USD reserves held in the East, following the introduction of Western sanctions on Russia this year; these have likely bolstered official purchases. This is consistent with official purchases announced by Turkey, Qatar and other nations. Market participants have pointed to the rapprochement between China and Gulf nations to support the thesis that demand for USD reserves is indeed declining. President Xi attended the very first China-Arab States Summit in history, seen as an echo to FDR’s meeting with King Abdul Aziz Ibn Saud in 1945 which cemented a new paradigm amounting to US security guarantees exchanged for oil sold in US dollars. Today, US incentives to provide security are likely to decline over the coming decade along with Western oil demand, whereas China’s growing demand for energy is likely to solidify trade with GCC nations over this timeframe. President Xi also spoke of a new paradigm — one of all-dimensional energy cooperation, which will entirely rely on RMB settlement for oil and gas trade over the next five years. While the long-term resilience of this thesis is difficult to rank in the present, this narrative is certainly consistent with price action associated with a steep accumulation of gold in support of the renminbi.

- Hedging Sanctions: We previously discussed the rise in perceived sanctions risks associated with USD reserves held in the East, following the introduction of Western sanctions on Russia this year. A less likely scenario worth considering is whether a steep increase in gold reserves could be associated with the building of a sanction-evasion war chest tied to China’s geopolitical ambitions. Tensions between China and Taiwan have come to a boil over the past year with a heightened sense of fear of a military confrontation since the war in Ukraine. In turn, some market participants could plausibly fear that the steep accumulation of gold is preceding a military confrontation, but there is little concrete evidence to support this. Further, one could argue that this is inconsistent with an apparent détente with the West, highlighted by the recent lifting of China’s embargo on Australian coal and a notable shift in China’s foreign policy communications.

…

Finally, as Zoltan Pozsar wrote most recently here (and in a must-read note last month), the role of gold may be changing as first Russia, then other countries (China) seek to force out the petrodollar and replace it with petrogold, a move which would finally lead to substantial price upside for the yellow metal which has gone nowhere in the past 2 years.

Remember Zoltan’s portfolio advice: Commodities should include three types of gold: yellow, black, and white. Yellow gold is gold bars. Black gold is oil. White gold is lithium for EVs.

Vir: Zerohedge