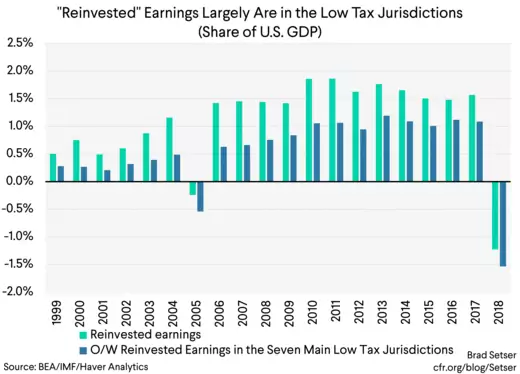

Mnoge mednarodne inštitucije, na čelu z UNCTAD in njegovim proklamiranim World Investment Reportom, vsako leto objavljajo statistike o rasti svetovnih neposrednih tujih investicij in njihovo visoko dinamiko razglašajo kot dinamiko globalnih investicij. Kot razkrivajo zadnje študije, od Gabriela Zucmana do IMF, pa podrobnejši pregled kaže, da je polovica teh investicij fantomskih. So zgolj navidezne investicije. Pravih investicij v obliki investiranega kapitala je malo. Večina investicij je v obliki reinvestiranih dobičkov podružnic ameriških korporacij v davčnih oazah oziroma med eno podružnico matične družbe in drugo, ki je locirana v davčni oazi (glejte spodnjo sliko). Da se matično podjetje razbremeni plačila davka na dobiček.

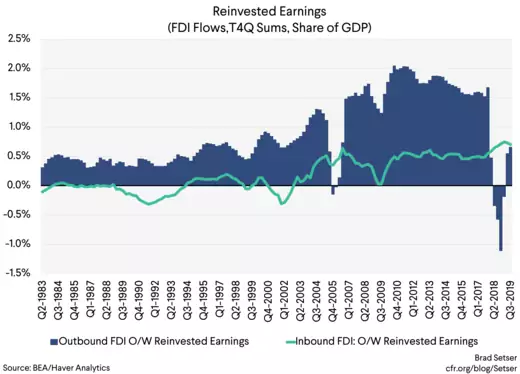

Nato pa je prišla Trumpova davčna reforma z znižanjem davka na dobiček podjetij, kar je vzelo motiv ameriškim korporacijam, da prelagajo dobičke med podružnicami v tujini (v obliki navideznih investicij reinvestiranih dobičkov). In prej ogromne ameriške neposredne investicije v tujino so zdrknile pod ničlo.

Spodaj je nekaj odlomkov iz odlične analize Brada Setserja.

Foreign direct investment is generally thought to be real investment in plant and equipment abroad—GE building gas turbines in France, GM building cars in China, Siemens buildingturbines in North Carolina, and BMW and Toyota building cars in South Carolina and Kentucky.

Statistically, though, FDI is often investment by one special purpose entity (generally located in a tax center) in another special purpose entity…so called phantom FDI.

That is why it is time to start viewing the direct investment data with a more jaundiced eye.

That same critical eye also needs to applied to the data on direct investment into and out of the United States, as it too is heavily influenced by transactions that are likely motivated primarily by tax considerations.

Consider the data on outward U.S. direct investment abroad.

That data historically has been dominatedby “reinvested” earnings—the profits American firms earn abroad that they legally kept in their offshore subsidiaries.

This was the source of thesupposedly offshore cash stashof U.S. firms (the funds were only legally offshore, as they legally were assets of say Apple Ireland or Microsoft Bermuda; in practice they were invested in U.S. financial assets—and firms that wanted to access their offshore cash to say buyback their shares could do so by borrowing against their offshore cash). The bulk of those reinvested earnings—if you looked closely in the data—weren’t being reinvested in physical assets, but rather were piling up in the offshore subsidiaries U.S. firms had established in low tax jurisdictions. From 2010 to 2018, 65 percent of all reinvested earnings were “reinvested” in jurisdictions like Ireland and Bermuda (which works out to about $200b a year of investment in those jurisdictions, or about half of all US FDI in the “pre-tax reform” data).

That clearly was a function of firms’ ability to defer paying U.S. tax on otherwise un-taxed global profits under the old tax law. Profits earned in high tax jurisdictions didn’t have any U.S. tax liability under the old law, as firms could deduct taxes actually paid abroad. Indefinite deferral effectively distorted the global data—raising the amount of U.S. direct investment abroad (the cash Apple held in Ireland was an asset of Apple USA, so reinvestment raised the stock of U.S. equity assets abroad even if technically the equity investment abroad was the accumulation of offshore cash) and the amount of foreign claims on the United States (U.S. treasuries purchases by Apple Ireland were counted as foreign holdings of U.S. government debt, that’s why Ireland was at one time the world’sthird largest holder of U.S. Treasuries).

In other words, financial globalization wasn’t all benign—rising “globalization” could simply mean more tax arbitrage, not more real integration. Reinvested earnings by U.S. firms abroad rose from about half a point of U.S. GDP in the 1990s to between 1.5 to 2 percent of GDP…a number out of line with the sum foreign firms “reinvested” in the United States.

It was basically just a big tax game, which inflated the FDI data until it (partially) reversed after the tax reform.

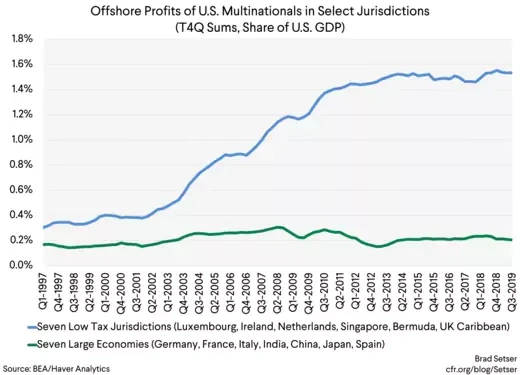

Under the new tax law, U.S. firms still earn large profits in low tax jurisdictions (seeMartin Wolf, theIRS country by country dataorKim Clausing’s latest)* but they no longer have a federal corporate income tax incentive to “reinvest” those funds abroad and accumulate financial assets inside their very profitable subsidiaries in low tax jurisdictions. Profits booked in a low tax jurisdiction can now be returned to the United States with no tax penalty—and they equally can be held abroad with no tax limits on how they can be used.