Lani sem večkrat pisal o tem, da ko pride do porasta inflacije, centralni bančniki takoj zaženejo paniko pred potencialno plačno-inflacijsko spiralo. Češ, rast plač kot najpomembnejšega inputa bi lahko povišala proizvodne stroške, kar bi nato “prisililo” podjetja, da “morajo” dvigovati cene proizvodov in storitev, kar pa bi povzročalo perpetualni pritisk na dvig plač zaradi dviga življenjskih stroškov. V tem komentarju sem opisal mehanizem te logike prek Blanchardovega WS-PS modela. Napisal sem tudi, da gre pri tej narativi centralnih bančnikov za ekskluzivno ideološkost: centralni bančniki se namreč v tem WS-PS modelu fokusirajo zgolj na WS (wage setting) stran, medtem kot na PS (price-setting) strani ignorirajo tržno in pogajalsko moč podjetij in predpostavljajo konstantne marže (stopnje dobička) podjetij. Drugače rečeno, centralni bančniki zamolčijo, da lahko podjetja z izkoriščanjem pogajalske moči dvigujejo svoje marže in s tem poganjajo cene proizvodov in storitev navzgor. Še več, zamolčijo, da podjetja to dejansko počnejo, kot kažejo študije za ZDA in Evropo. Namesto tega centralni bančniki žugajo sindikatom naj ob višji inflaciji ne zahtevajo dviga plač. Torej namesto, da bi opozorili korporacije, da se omejijo glede marž, vztrajno zahtevajo, naj zaposleni nosijo stroške povišane inflacije prek znižanja realnih plač.

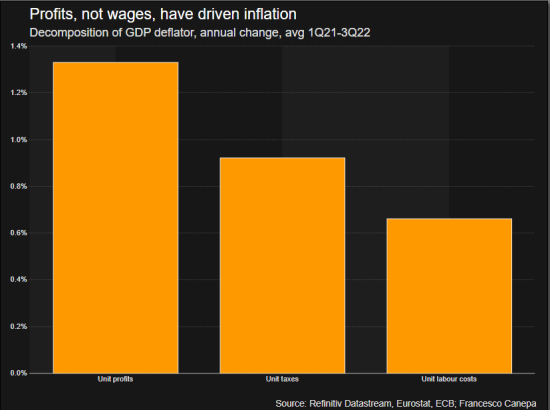

No, prejšnji teden so se člani izvršilnega odbora ECB umaknili v oddaljeno arktično vasico v Finski, kjer so diskutirali o ekonomski situaciji v evrskem območju in med drugim tudi pogledali prezentacijo glede “distribucijskih učinkov” inflacije. Sama prezentacija je sicer nedostopna, toda med drugim naj bi bil v njej podoben graf, kot tale spodaj, ki ga je povzel Reuters. Spodnji graf kaže dekompozicijo deflatorja BDP (t.j. inflacije BDP, kar je različen indeks od običajnega CPI) na rast cen treh faktorjev BDP po dohodkovni metodi: dobičkov, plač in davkov. In kot lahko vidite, naj bi v evrskem območju v obdobju Q1 2021 – Q3 2022 rast dobičkov imela dvakrat večji prispevek k porastu BDP deflatorja kot rast plač (1.33% vs. 0.67%), rast davkov pa 0.92%. Drugače rečeno, porast dobičkov in davkov je prispevala k inflaciji BDP več kot tri četrtine (77%), rast plač pa manj kot četrtino (23%).

.

Zakaj torej centralni bančniki žugajo sindikatom, naj se držijo nazaj, namesto da bi žugali korporacijam in državi naj omilijo svoje apetite? Pri čemer pa so delavci tisti, ki so utrpeli upad kupne moči njihovih plač (za približno 5% v 2022).

Zakaj naj bi zaposleni nosili bolečino zniževanja inflacije, če pa:

- pregledni študiji ekonomistov iz IMF in BIS iz lanskega leta kažeta, da plače še nikoli v zgodovini 20. stoletja niso bile dejavnik povišane inflacije (niti v zloglasnih 1970-ih letih)?

- podatki kažejo, da se je od 1970-ih let delež plač v razdelitvi BDP zmanjšal iz 70% na 56%, delež dobičkov pa iz ene petine na eno tretjino?

Zakaj so bile plače na zadnji tiskovni konferenci predsednice ECB Christine Lagarde omenjene 14-krat, medtem ko marže podjetij niso bile omenjene niti enkrat, ko je bilo govora o politiki ECB glede zniževanja inflacije?

Zgodba je povsem ideološka in je tako globoko vsidrana v makroekonomsko teorijo in glavne teoretske modele, da tega večina “izšolanih” ekonomistov niti ne opazi. To narativo o “dobički so dobri, plače pa so strošek za podjetja” ter o škodljivosti dvigovanja plač smo dobili intervenozno med študijem ekonomije. Skoraj nihče sploh ne razmišlja več, da sta v podjetjih (ob poslovnem okolju) dva ključna proizvodna dejavnika – delo in kapital in da bi morala oba pravično participirati na rasti prihodkov oziroma donosa podjetij. Namesto tega je prevladala dogma, da se menedžement podjetij upravičeno trudi za dvig dobičkov in s tem za povečevanje vrednosti in kapitalskega donosa lastnikov, medtem ko so zaposleni zgolj nujna in nebodigatreba “navlaka”, pač strošek.

Toda ta narativa se bo morala spremeniti. Tudi zaradi učinkovitosti politik za zniževanje inflacije.

Indeed, wages have been growing far more slowly than inflation, implying a 5% drop in the standard of living for the average employee in the euro zone compared with 2021, according to ECB’s calculations.

That’s pretty much the opposite of the wage-led inflation that characterised the 1970s, an era which has become the most widely used point of comparison in the public debate about appropriate central bank policy responses, economists say.

“The public discourse to some extent is detached from what’s actually happening out there,” said Philipp Heimberger, an economist at the Vienna Institute for International Economic Studies. “The main story of the risks going forward is still that there’s a looming wage-price spiral which should make the central bank even more aggressive in hiking interest rates.”

For example, wages were mentioned 14 times in ECB President Christine Lagarde’s latest news conference while margins didn’t get a single mention. Her deputy, Luis de Guindos, also warned that the ECB needed to be careful because labour unions might demand excessive pay rises.

“You see a very clear reluctance to discuss profit,” Daniela Gabor, a professor of economics and macro-finance at the University of West England in Bristol. “That illustrates that the distributional politics of inflation targeting is: You don’t go for profits; you don’t go for capital.”

In the United States, the issue of runaway margins has been raised by former Federal Reserve Bank vice-chair Lael Brainard, who is now President Joe Biden’s top economic adviser, and Democratic senators Elizabeth Warren and Bernie Sanders.

Even inside the ECB, labour representatives demanding higher pay for central bank staff have distanced themselves from what they described as the institution’s “anti-worker bias”.

They cited, among others, a paper by researchers at the International Monetary Fund showing that accelerating wages have not historically led to a wage-price spiral.

PROFIT VS WAGES

ECB policymakers gathered in Finland went through similar data sets showing that profits had outpaced wages thanks to savings built up during lockdowns being spent, but also because of companies’ power to set prices, the sources said.

With those savings now being depleted and competition returning, things may be changing for ECB policymakers who have been calling for a redrafting of the inflation narrative.

In January, Portuguese central bank governor Mario Centeno was among the first to warn about the risk of a very clear increase in profit margins, saying it should be brought up the European policy agenda.

ECB board member Fabio Panetta later said workers had borne the brunt of the surge in prices while, on balance, company mark-ups had remained stable, or even increased in some sectors.

Wages are accelerating, with the ECB’s forward-looking wage tracker anticipating a rise of nearly 5% in 2023 for contracts signed in the last quarter of 2022. But that won’t offset the massive drop in real wages over the past year, analysts said.

“A key missing ingredient is the bargaining strength of the labour movement, which is structurally weakened by the disinflation policies of the 1980s and the ensuing liberalisation of labour markets,” said Mattias Vermeiren, a professor of international political economy at the Ghent Institute for International and European Studies.

During the last inflation crisis in the 1970s, nearly 70% of economic output went to employees, with just over 20% going to profits, according to Eurostat data. Now, labour’s share stands at 56% with a third going to profits.

The ECB policymakers went over those differences at their Finnish retreat, though their tentative conclusions were dotted with caveats, the sources who attended the meeting said.

Some argued that furlough schemes during the pandemic may buttress incomes, the sources said, and that a sustained period of high inflation may raise salary demands in a way that models developed during periods of stable prices fail to predict.

And the interest rate doves might have their work cut out after data showed inflation in France, Spain and Germany exceeded expectations last month.

Vir: Reuters

You must be logged in to post a comment.