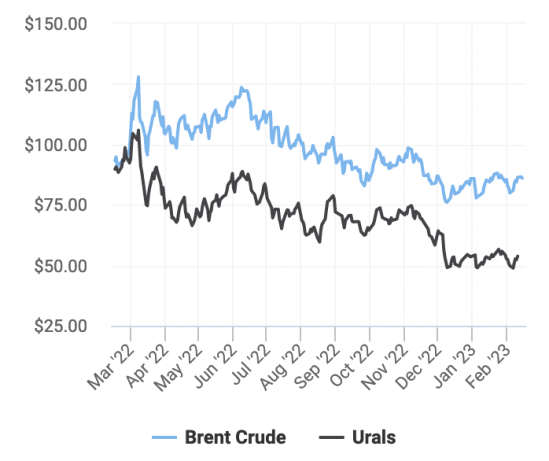

Mnogi novinarski komentatorji, pa tudi kvalificiran, vendar zelo rusofobni Robin Broks, navdušeno poročajo, kako je cenovna kapica na rusko nafto uspešna, ker naj bi tej kapici uspelo povečati diskont na rusko nafto na raven med 30 in 35 $/sodček. Pri tem izhajajo iz javno objavljenih borznih cen ruske premijske nafte Urals ter to primerjajo s cenami severnomorske premijske nafte Brent ali premijske teksaške nafte WTI. Gledajo sliko, kot je tale:

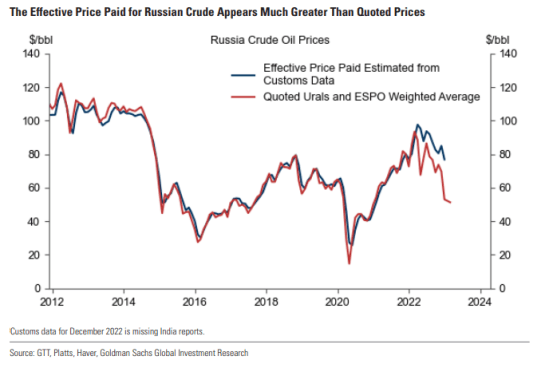

Vendar je resnica precej drugačna, saj se praktično nič ruske nafte ne proda po ceni za Urals nafto. Slednja je namreč zgolj statistična ocena, pridobljena na podlagi posrednih ocen različnih agencij, ki pa so irelevantne v tem primeru, ker se po tej ceni ne sklepa nobenih pogodb. O tem je 10 dni nazaj pisal tudi The Economist, poznavalci energetskega trga pa o tem govorijo že nekaj mesecev (več spodaj). Problem je, ker ni neposrednih podatkov o pogodbenih cenah. Nazadnje so analitiki Goldman Sachs objavili spodnjo sliko, ki na podlagi preračuna iz “leaked” ruskih carinskih podatkov kaže, da naj bi bila efektivna cena ruske nafte danes na ravni med 75 in 80 $/sodček. Torej za 20 $/sodček višja od cenovne kapice.

Vir: Goldman Sachs

Vendar je slika glede prodajnih cen ruske nafte bistveno bolj niansirana. Odvisna je od prodajnega kanala (kot sledi iz “leaked” ruskih carinskih podatkov). Zaradi cenovne kapice naj bi se zmanjšale cene nafte, ki jih Rusija prodaja prek štirih evropskih pristanišč (glejte spodaj cene Baltic, Druzhba in Black Sea), medtem ko so prodajne cene nafte za azijske države (Pacific, China, Arctic) na ravni okrog 80 $/sodček. Hkrati pa je treba vedeti, da tudi cene ruske nafte prek “evropskih kanalov” ne odražajo dejanskega stanja, saj se je dejanska uradna prodaja po teh kanalih zahodnim kupcem precej zmnajšala, povečala pa se je “siva” prodaja ruske nafte – prek ruske “skrite flote” ter prek transshipinga (dostava iz ladje na ladjo). O slednjih dveh, ki že predstavljata levji delež prodaje ruske nafte prek evropskih kanalov, pa ni podatkov.

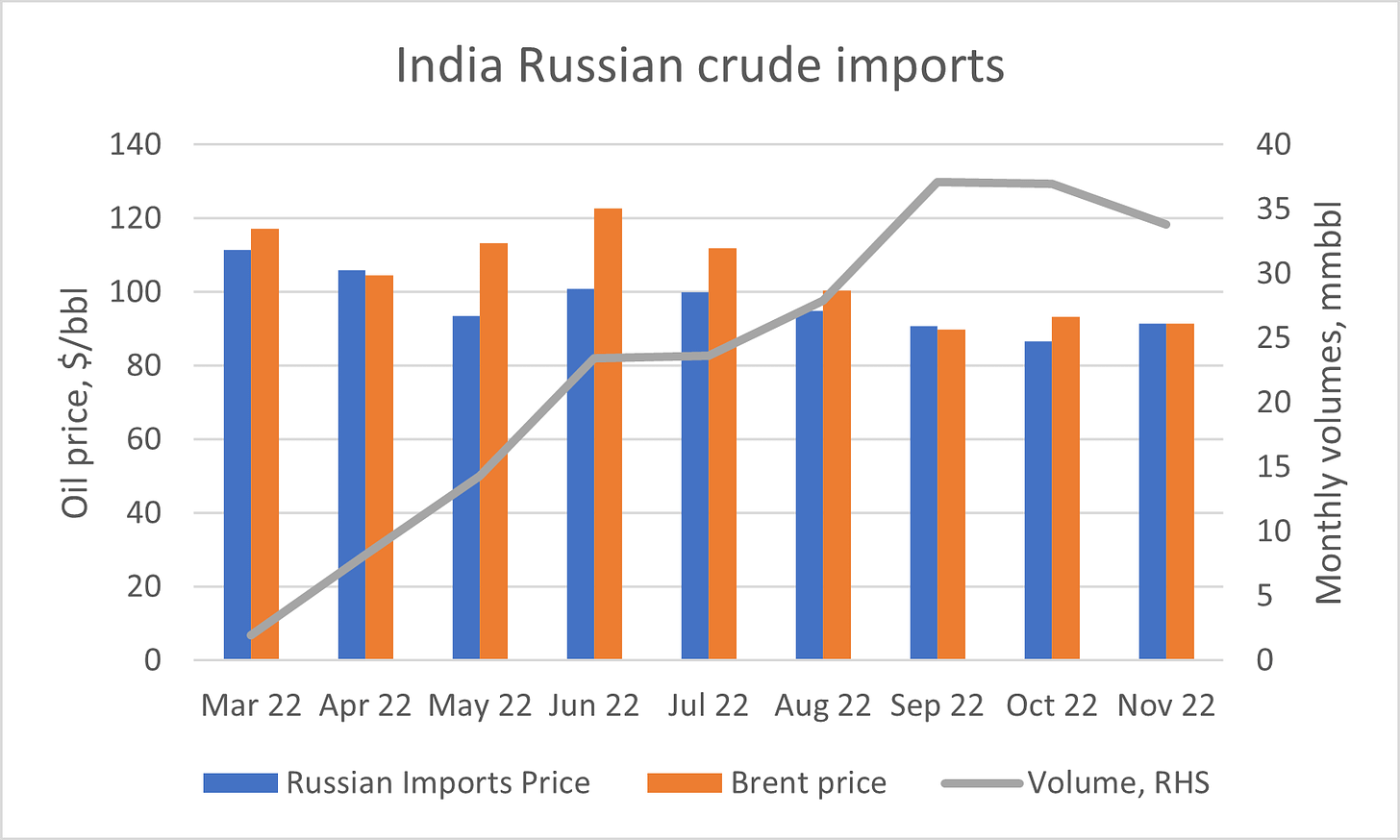

Spodaj je zapis Sergeya Vakulenka, energetskega strokovnjaka, ki je ocenil, kakšne naj bi bile dejanske cene ruske nafte. Če povzamem, je pomembno več dejavnikov. Prvič, dejanske prodajne cene ruske nafte naj bi imele malenkostni diskont glede na Brent cene. Anekdotski podatki trgovcev kažejo na diskont 6-10 $/sodček. Eden izmed pomembnejših prodajnih trgov za rusko nafto je Indija, kjer indijske rafinerije kupujejo rusko nafto po cenah po benchmark cenah za dubajsko in omansko nafto, in po teh podatkih je bil diskont ruske nafte glede na Brent zelo majhen in naj bi se po zadnjih dosegljivih podatkih zmanjšal na blizu ničle. Drugič, pomembno je vedeti, da eno največjih indijskih rafinerij (Nayara Energy) obvladuje ruska Rosneft. Tretjič, borzne cene glede prevoza ruske nafte so irelevantne, če ima Rusija svojo “skrito floto” tankerjev in če najema tankerje, saj je tukaj pomemben zgolj strošek prevoza. Četrtič, Rusija dnevno nepossredno proda za 1.6 do 1.8 milijona sodčkov nafte prek kitajskega plinovoda in pristanišča Kozmino (85 km južno od Vladivostoka in blizu kitajske in severnokorejske meje), kjer so transportni stroški nizki, prodajne cene pa neznane.

Iz vidika učinkovanja sankcij je pomembno predvsem troje. Prvič, vsem v naftni verigi je v interesu, da poročajo čim nižje nakupne cene nafte in čim višje cene prevoza, da pokažejo, da se držijo sankcij. In če ruska naftna podjetja kontrolirajo večji del naftne verige (vključno s tankerji in rafinerijami), se elegantno izognejo sankcijam. Pri čemer še posebej profitirajo indijske rafinerije, ki predelana goriva iz ruske nafte nato prodajajo naprej v Evropo in ZDA. Drugič, tudi ruskim naftnim podjetjem je v interesu, da poročajo ruskim oblastem čim nižje prodajne cene, da si s tem zmanjšajo osnovo za izvozne carine. In tretjič, tudi Putinu in oligarhom je v interesu, da poročajo čim nižje uradne prodajne cene, dejanske razlike v zaslužkih pa transferirajo na svoje skrite račune za “slabe čase”.

Toda iz vidika osnovnega namena sankcij je pomembno predvsem, ali se bo zaradi cenovnih kapic na surovo nafto in goriva res presušil ruski proračun, s čimer bi Rusijo prisilili, da ne bi mogla več financirati vojne v Ukrajino. Pričakovati kaj takšnega v situaciji, ko ruska oblast kontrolira vse trgovce s plinom in nafto in jim lahko kadarkoli poviša izvozne carinske stopnje in dajatve za iskoriščanje virov ali jim nabije dodatne enkratne dajatve (kot je že naredila pri Gazpromu) in ko ima ruska vlada oblikovan poseben naftni premoženjski sklad, je eluzivno. Ni verjetno na kratek in srednji rok iz vidika, da bi to lahko vplivalo na dogajanje v ukrajinski vojni. Cenovna kapica je zgolj dimna zavesa, zaradi katere se nekateri politiki počutijo bolje.

At the first glance, the price cap for Russian oil works like a charm. The market is well-supplied, on one hand, Russia did not curtail its production in an attempt to force higher prices, and on the other Russian crude is reportedly sold at a deep discount to the general market levels. According to the official Russian statistics, published by the Central Bank and the Ministry of Finance, the average price for the benchmark Urals crude for the period between 16.12.2022 and 15.01.2023 was $46.82/bbl, which is well below the $60/bbl price cap, imposed by the G7 and EU. At the very least, these numbers mean trouble for the Russian state budget, as they form the basis for the customs duties and oil extraction taxes levied on the oil companies, and these two taxes comprised more than 45% of the Russian state income in the first half of 2022.

On the other hand, this picture suggests, that Russia as a whole has lost a substantial part of its revenues, which may be misleading, and in reality, the situation is much more nuanced.

The Urals price, quoted by the Russian official statistics and reiterated in the press is a notional value. Extremely little oil, if any is sold at this price. This is an average of FOB Primorsk and FOB Novorossiysk price assessments, calculated according to methodology, which is irrelevant to the current market environment

The actual sales price of the Urals in its main market is circa $70-75/bbl

The non-transparent shipping market creates a mechanism for evading the price cap and channeling a large portion of Russian oil revenues to shadow accounts.

A large amount of seaborne Russian crude (up to 800 000 bbl/day, 20% of the total seaborne volumes) is sold at $70/bbl or more on FOB basis, thus openly defying the cap.

Let me go into more detail on each of these points.

Where do the mid-40s prices come from in the 80-plus market?

Commodity markets operate with a plethora of prices. There are various grades of the same product, (Brent, Urals, WTI, Dubai, Oman, etc.), spot and futures prices, and different delivery basis and terms (CIF Rotterdam and FOB Primorsk for example). Let’s dissect the difference between the last two. Rotterdam is where many buyers actually needed Russian crude before the war. At times they might be willing to pay more for it than for Brent, at times less, depending on the market conditions between diesel fuel and gasoline (In a refinery Urals yields more diesel than Brent). To get it there from Primorsk, a Russian port in the Gulf of Finland, one has to pay for shipping and associated expenses. A buyer may pick up cargo in Primorsk (this would be FOB basis) and take care of the shipping costs, or in Rotterdam (on CIF basis) with shipping costs paid by the seller.

Until 2022 this was a transparent and vibrant trade. Baltic Exchange, a London shipping industry clearinghouse, was quoting two standardized indicators, TD6 and TD17, serving as benchmarks for shipping costs between the Novorossiysk and Augusta, an oil trading hub in Sicily, and Primorsk and Rotterdam. These indicators were calculated based on information provided by the Baltic Exchange members – shipping brokers, handling most of the vessel chartering trade.

The Urals-Brent differential was influenced by the market conditions, and not political considerations, boycotts, or embargoes.

It is important to remember, that Urals FOB Primorsk or Novorossiysk, quoted by Argus and Platts, have never been the proper market prices, derived from the actual deals. They always were assessments, estimates by the agencies, calculated from the three elements – Brent Dated price, Brent-Urals spread estimate and shipping costs estimates. The agencies used to run the numbers by the market participants to check if they make sense and might get access to price information from some actual FOB sales, but the sense check stopped at that. It is also important to keep in mind, that Brent was a reasonable benchmark for Urals, as these two crudes were sold in the same market to the same refiners.

In late 2022 everything changed. Russian crude is no longer sold in Rotterdam and Augusta. London-based shipping brokers handle a much lower share of activities in Russian ports. Baltic Exchange has killed the TD17 instrument and modified the TD6, so it is not necessarily applicable to Russian cargoes.

However, the Argus methodology, last updated in January 2023, does not seem to recognize these changes. Argus analysts are smart and professional people, and most likely they see the deficiencies of the old approach and try their best to provide a sensible estimate, but this might be difficult with the toolbox they are used to.

What is the actual Urals sale price?

Since the European embargo, most of the Russian crude, loaded in the Baltics and the Black Sea, goes to India, predominantly to west coast refineries in Gujarat and Kerala states (the number of tankers with non-declared final destinations surged as well, but many of them end up in India too). Coincidentally, one of the largest refineries there, Nayara Energy with 400 kbd capacity, is controlled by Rosneft. Anecdotal evidence from traders is that Urals sells to other Indian refineries at a 6-10 USD discount to Brent, dependent mostly on the prices of Dubai and Oman crudes, which are the benchmark sorts in that part of the world.

European refineries and their parent companies trading desks often exchange data with price agencies on daily basis, but this is probably not the case for the Indian refineries, so the agencies are unlikely to get a glimpse of the prices. Indian customs statistics might be of some help. Unfortunately, official December data is not in yet, and even December arrival volumes would have left Russia a month earlier, so even that number would not be a perfect indicator of what’s going on now, but it still gives some idea. Official data for March 2022 – November 2022 shows relatively small Urals – Brent discounts, coming to zero in November. This data gives more confidence to the anecdotal evidence from the traders and suggests that the actual discounts might be even lower.

What does it cost to bring a barrel of oil from the Baltic Sea to India?

Hellenic Shipping News has quoted $11-$19/bbl shipping costs from the Russian ports to India, and these rates are higher than rates for comparable distances, such as a voyage from the Persian Gulf to Rotterdam. However, these are open-market quotes. If the rumors of the 100+ tankers recently acquired by Russian actors for the shadow fleet are true, then most of the Russian trade would be carried on these tankers, and shipping rates and costs would be almost irrelevant except for the bunkering fuel and insurance elements. It is also likely that additional tankers are booked on a time-charter basis, which also makes the cost of a single voyage non-transparent. Needless to say, these tankers would not be booked through Baltic Exchange shipping brokers, so there is a dearth of information on the actual conditions.

Where does it bring us on the Urals FOB price after all?

The two elements, Urals-Brent price differential for Gujarat deliveries and shipping quotation give us a range of 17 to 29 USD/bbl discount. The upper range of it brings us close to the widely publicized figure of circa $50/bbl for the Russian crude (have to reiterate, netback to Russian ports, not the actual sale price), but I believe the actual discounts are lower.

This situation also allows for an elegant way to circumvent the price cap. As long as the oil companies directly or indirectly control the shipping element of the value chain and are able to refer to some high benchmark number for the cost of shipping, they could pretend they are selling the crude below the price cap, gain access to insurance services from the Western markets, and collect additional revenues on the shipping leg, thus keeping then whole for the full transaction.

And we also have to remember, that up to 1.6 – 1.8 million barrels per day leave Russia via the Far Eastern route, partially via pipeline to China, and partially via the port of Kozmino. It had its capacity expanded from 600 to 800 thousand barrels per day, and the price there is going steadily above the $60/bbl price cap on the FOB basis. Russia is apparently able to handle at least these volumes without a need to resort to window-dressing so as to be able to employ Western market infrastructure, unavailable for sales over the price cap.

Qui Prodest?

As I have mentioned at the beginning of this note, there is an obvious loser – the Russian state budget. In theory, it would be the Indian refiners and international tanker owners, pocketing $30/bbl between them, but I believe that their cut is rather small.

Indian refiners would still be extremely interested to portray the situation as if they do manage to extract deep discounts from desperate Russian sellers. This optics would strengthen their negotiating position vis-à-vis Iran, UAE, and other regional sellers. The same logic applies to the shipowners.

Russian oil companies in the past might want to tell the world that they were successful to sell their crude at the top of the market to impress their international shareholders and keep debtholders happy and content. Now they have nobody to impress, but apparently low realized international price for their crude slashes their tax bill, so the companies would be happy to support the picture as well.

The Russian Ministry of Finance takes notice though and there are discussions of switching to Dubai crude price as the base for the Russian oil industry taxes calculations.

The sudden murkiness and non-transparency provide a lot of space for creativity for the managers and middlemen involved in the oil trade and create fertile grounds for side deals and kickbacks not seen since the 1990s when billion-size fortunes have been made by people in charge of the commodities trade in the former USSR.

Shipping and trading companies serving this trade also provide a convenient conduit to siphon some funds away from the watchful eye of the US and EU economic warfare bodies in charge of embargoes and sanctions. Part of the crude value may end up in the accounts of these companies and used for purchases of controlled goods, from oilfield equipment, if used by the oil companies themselves, to electronic chips and other parts and materials for the arms making, if the government is aware of the actual goings and has some say over the use of proceeds, which is quite likely. This is not unprecedented – back in 2016 Putin admitted that a 50% share of the dividends, paid on the state stakes in Gazprom and Rosneft, is spent by Rosneftegaz on “special projects that require close attention”. Going a step further, some of the funds may be used to support and finance pro-Kremlin or extremist groups in the West, the same way as Moscow has been supporting them in the 1970s.

And at last (and sorry for indulging in a bit of conspiracy theories), these circumstances create an ideal mechanism for the creation of an emergency fund for Mr. Putin and his coterie if he falls from power and has to leave Russia and hide somewhere. After all, Gaddafi, Mobutu, Abacha, and other dictators of resource-rich countries employed very similar mechanisms.

“The West’s cumulative bid to choke the Russian economy has not had the desired effect so far, as latest figures show. Russia’s budget revenues from the oil and gas industry grew 28% last year, amounting to $36.5 billion. Oil production in Russia rose 2% last year to 535 million tonnes, while exports of the fuel increased by 7.5%.”

36 milijard je pribžno toliko kot je ruski izvoz žit in orožja skupaj. Cene žit so se v 2022 močno povečale in bodo na visokem nivoju tudi ostale zaradi izpada ukrajinskega izvoza in zaradi podražitve ključnih imputov tj. umetnih gnojil in nafte. Gnojila bosta Belorusija in Rusija kontrolirali še v večji meri kot doslej (ne samo zaradi izpada ukrajinske, temveč predvsem evropske proizvodnje) kar pomeni, da bosta dodatno profitirali od višjih cen. Podobno bo z določenimi minerali (titan, antracit…) ali metalurškimi proizvodi.

Rusija je sistemsko svetovno pomemben dobavitelj ključnih surovin, poljščin in določenih proizvodov. Take države se ne da izolirati. To bi moralo biti jasno od začetka.

Če se bo to nadaljevalo v bodoče, bo prva pokleknila Evropa.

RT: Redirecting supplies

“The West’s cumulative bid to choke the Russian economy has not had the desired effect so far, as latest figures show. Russia’s budget revenues from the oil and gas industry grew 28% last year, amounting to $36.5 billion. Oil production in Russia rose 2% last year to 535 million tonnes, while exports of the fuel increased by 7.5%.”

36 milijard je pribžno toliko kot je ruski izvoz žit in orožja skupaj. Cene žit so se v 2022 močno povečale in bodo na visokem nivoju tudi ostale zaradi izpada ukrajinskega izvoza in zaradi podražitve ključnih imputov tj. umetnih gnojil in nafte. Gnojila bosta Belorusija in Rusija kontrolirali še v večji meri kot doslej (ne samo zaradi izpada ukrajinske, temveč predvsem evropske proizvodnje) kar pomeni, da bosta dodatno profitirali od višjih cen. Podobno bo z določenimi minerali (titan, antracit…) ali metalurškimi proizvodi.

Rusija je sistemsko svetovno pomemben dobavitelj ključnih surovin, poljščin in določenih proizvodov. Take države se ne da izolirati. To bi moralo biti jasno od začetka.

Če se bo to nadaljevalo v bodoče, bo prva pokleknila Evropa.

Všeč mi jeVšeč mi je