Hm, dobrih deset let nazaj, ko so me obtoževali neoliberalizma, nisem imel pojma, česa me obtožujejo. Ne meni ne kolegom se sanjalo ni, kaj je neoliberalizem. V ekonomski teoriji tega pojma namreč nismo poznali. Če že, je s tem, vsaj na mojem področju, morda mišljen val liberalizacije trgovine po drugi svetovni vojni. Ampak to, kot sem se poučil kasneje, ni tisto, kar so imeli v mislih sociologi, ki so se tega spomnili. Simon Wren-Lewis ima tukaj dobro razlago evolucije korenin neoliberalizma. Poenostavljeno rečeno, neoliberalizem je levičarska psovka za desničarje (beri: ekonomiste), pri čemer so levičarji imeli v mislih predvsem Miltona Friedmana in Montpelerinovo združbo zelo heterogenih bodisi friedmanovskih sledilcev in zagovornikov idej prostega tržnega gospodarstva bodisi konkurečnih “prodajalcev idej” libertarizma. Vsem pa je skupno to, da sovražijo “veliko državo”. Saj veste, država zganja nasilje nad ljudmi, s tem ko jim predpisuje obvezne javne storitve in pobira davke ter s tem onemogoča njihovo prosto izbiro.

Cel štos je v tem, da prostotržni in libertarni ekonomisti svoje ideje prodajajo kot neideološke in prosti trg kot naravno stanje sveta, sociologi pa kričijo, da neoliberalizem ne pomeni odsotnosti ideologije. Prav imajo seveda drugi, kar je zelo lepo in enkrat za vselej pokazal Karl Polanyi v “The Great Transformations” (1944). Odločitev za favoriziranje prostega trga je sama po sebi ideološka (in to skrajno ideološka), prosti trg brez institucionalne vpetosti v družbo pa ne more delovati. Trga brez močne države ni. Brez močne regulatorne vloge države se trg sprevrže v to, kar ga inherentno poganja – v zmago močnejšega, ki si vzame vse. Torej v monopol ali najboljšem primeru omejen oligopol, ki zlorablja svojo moč na račun šibkejših (potrošnikov, konkurentov). In tisti, ki zagovarjajo neomejen trg, se na koncu vedno izkažejo kot plačani lobisti velikega kapitala.

Kakorkoli, med ekonomisti je danes konsenz, da je neoliberalizem morda najlažje poistovetiti z Washingtonskim konsenzom (WK), torej z 10 zapovedmi, ki so jih od sredine 1980. let naprej zagovarjale ključne washingtonske inštitucije: IMF, Svetovna banka in ameriški State department. Pravila pa je zapisal britanski ekonomist John Williamson (1989), ter jih kasneje (2003) modificiral in dodal malce bolj človeški obraz. Osnovne poante WK so liberalizacija (trgovinskih in kapitalskih tokov), deregulacija, znižanje mejnih davčnih stopenj in davčna vzdržnost, fleksibilni tečaji in privatizacija, torej zmanjšanje države in povečanje vpetosti v mednarodne tržne sile. Vse lepo in prav, tudi jaz bi se pod to podpisal pred dobrimi desetimi leti. Predvsem zato, ker nisem razumel, kaj takšna vseobsežna liberalizacija, deregulacija, privatizacija in izgon države v medsebojni interakciji prinesejo na dolgi rok. Prinesejo pa predvsem povečano nestabilnost in neenakost, saj ni več sider, ki so držale gospodarstva v ravnotežju in ni več sider, ki so vzdrževale družbeno ravnovesje.

To, da se je WK najprej razbil na čereh azijske, ruske in vzhodnoevropske finančne krize (1997-98), nato v Argentini (2001) in dokončno v globalni finančni krizi (2008), je logična posledica “odsidranja” držav. Je posledica pretirane liberalizacije in deregulacije, ki se sprevrže v močno volatilnost in na koncu v razpad sistema. Toda WK, kot je že pred desetletjem nekajkrat lepo popisal harvardski razvojni ekonomist Dani Rodrik, je dejansko nasedel na čereh že v Latinski Ameriki, desetletja pred tem, preden je bil sploh formalno zapisan. Latinskoameriške države, ki so desetletja verno sledile naukom WK, se niso mogle razvojno odlepiti, azijske države, ki so šle v kontrolirano liberalizacijo z močno regulatorno vlogo države, so postale razvojni tigri.

Kako šampionska je neoliberalna agenda, če jo pogledamo iz perspektive nekaj desetletij? Prejšnji teden so se tega vprašanja učinkovitosti neoliberalnega gospodarskega modela lotili tudi v samem izvoru te “pošasti”: v IMF. Trije ekonomisti IMF (Jonathan D. Ostry, Prakash Loungani, and Davide Furceri), ki jih dobro poznate, če prebirate ta blog (glejte tukaj in tukaj), po temah o neenakosti in rasti, redistribuciji in rasti, vlogi sindikatov, hitrosti fiskalne konsolidacije etc., so se lotili tudi seciranja uspešnosti politik, ki izhajajo iz tega neoliberalnega modela. V članku “Neoliberalism: Oversold?“, se sprašujejo, če neoliberalizem ni bil precenjen. Analizirajo dve področji neoliberalne agende, in sicer glede liberalizacije kapitalskih tokov in glede fiskalne vzdržnosti (austerity), ter seveda ugotovijo, da je bil, kljub mnogim pozitivnim učinkom za nerazvite države, neoliberalizem neučinkovit:

- liberalizacija kapitalskioh tokov poveča volatilnost in poveča tveganje makroenomske nestabilnosti. Če pride do finančnih kriz, pa se te vedno končajo v solzah in v povečanju neenakosti. Neenakost pa zmanjša vzdržnost rasti, torej liberalizacija kapitalskih tokov poruši to, čemur je bila prvotno namenjena;

- fiskalna konsolidacija ne more biti sama sebi namen, pomemben je njen timing glede na okoliščine. Prehitro zmanjšanje javnih izdatkov samo pozvroči (ali poglobi) krizo in ima nasproten učinek od željenega, saj pade gospodarska rast, delež dolga pa se avtomatično povečuje. Zmanjšanje dolga in ustvarjanje fiskalnega prostora se dela v dobrih časih, ne slabih.

Ostry, Loungani & Furceri na koncu ugotovijo, da ni enotnega recepta za razvoj, da je potrebno razvojne strategije prilagoditi okoliščinam. In povedo, zakaj in kako je IMF v zadnjih letih spremenil svoja stališča do teh vprašanj in tudi spremenil svoje nasvete. To priznanje pa kljub škodi, ki jo je IMF povzročal nekaj zadnjih desetletij državam v razvoju z napačnimi in škodljivimi nasveti, velja pohvaliti. Večje koristi od spremembe intelektualnega kurza na IMF sicer ne bo, vseeno pa gre za pomemben znak intelektualne poštenosti v “najbolj neoliberalni inštituciji“. Ne pozabite, da je Jonathan Ostry namestnik direktorice IMF.

There is much to cheer in the neoliberal agenda. The expansion of global trade has rescued millions from abject poverty. Foreign direct investment has often been a way to transfer technology and know-how to developing economies. Privatization of state-owned enterprises has in many instances led to more efficient provision of services and lowered the fiscal burden on governments.

However, there are aspects of the neoliberal agenda that have not delivered as expected. Our assessment of the agenda is confined to the effects of two policies: removing restrictions on the movement of capital across a country’s borders (so-called capital account liberalization); and fiscal consolidation, sometimes called “austerity,” which is shorthand for policies to reduce fiscal deficits and debt levels. An assessment of these specific policies (rather than the broad neoliberal agenda) reaches three disquieting conclusions:

- The benefits in terms of increased growth seem fairly difficult to establish when looking at a broad group of countries.

- The costs in terms of increased inequality are prominent. Such costs epitomize the trade-off between the growth and equity effects of some aspects of the neoliberal agenda.

- Increased inequality in turn hurts the level and sustainability of growth. Even if growth is the sole or main purpose of the neoliberal agenda, advocates of that agenda still need to pay attention to the distributional effects.

…

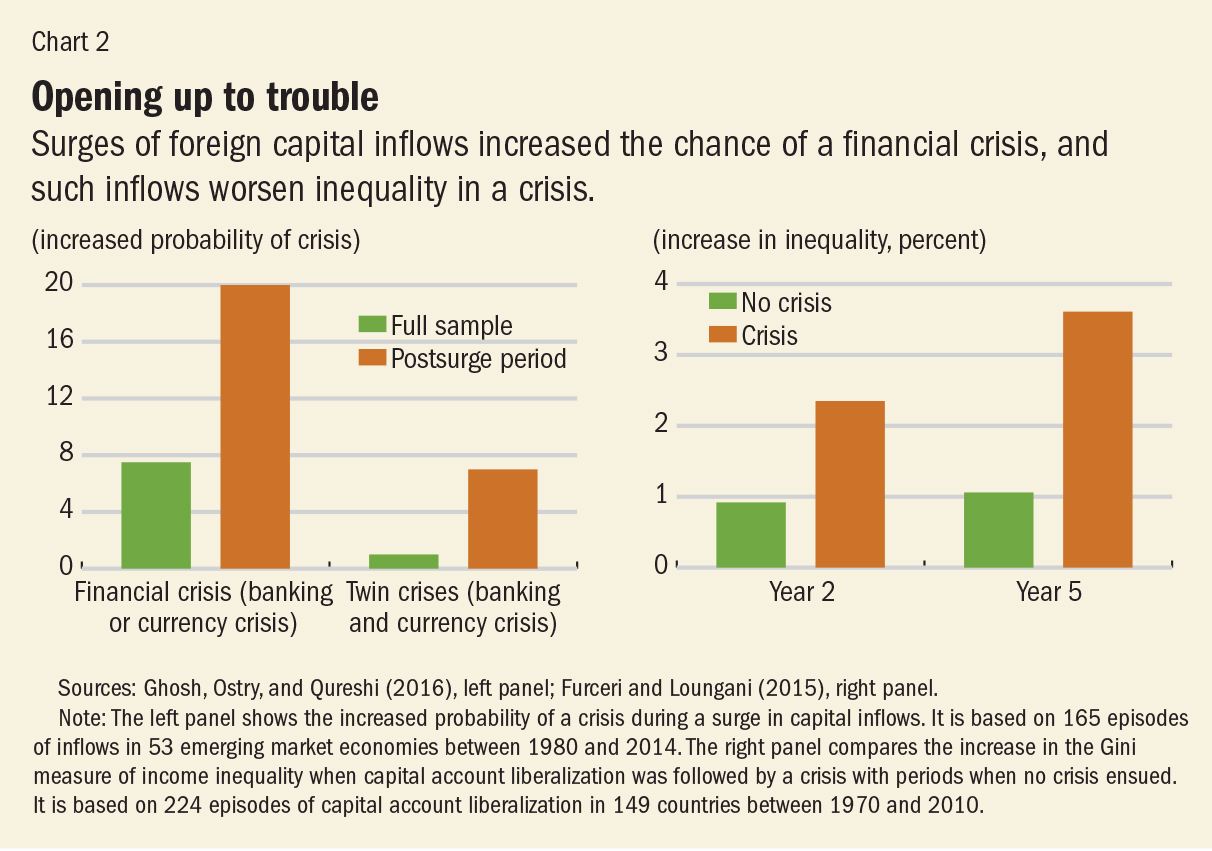

Although growth benefits are uncertain, costs in terms of increased economic volatility and crisis frequency seem more evident. Since 1980, there have been about 150 episodes of surges in capital inflows in more than 50 emerging market economies; as shown in the left panel of Chart 2, about 20 percent of the time, these episodes end in a financial crisis, and many of these crises are associated with large output declines (Ghosh, Ostry, and Qureshi, 2016).

The pervasiveness of booms and busts gives credence to the claim by Harvard economist Dani Rodrik that these “are hardly a sideshow or a minor blemish in international capital flows; they are the main story.” While there are many drivers, increased capital account openness consistently figures as a risk factor in these cycles. In addition to raising the odds of a crash, financial openness has distributional effects, appreciably raising inequality (see Furceri and Loungani, 2015, for a discussion of the channels through which this operates). Moreover, the effects of openness on inequality are much higher when a crash ensues (Chart 2, right panel).

The mounting evidence on the high cost-to-benefit ratio of capital account openness, particularly with respect to short-term flows, led the IMF’s former First Deputy Managing Director, Stanley Fischer, now the vice chair of the U.S. Federal Reserve Board, to exclaim recently: “What useful purpose is served by short-term international capital flows?” Among policymakers today, there is increased acceptance of controls to limit short-term debt flows that are viewed as likely to lead to—or compound—a financial crisis.

…

Curbing the size of the state is another aspect of the neoliberal agenda. Privatization of some government functions is one way to achieve this. Another is to constrain government spending through limits on the size of fiscal deficits and on the ability of governments to accumulate debt. […]

Markets generally attach very low probabilities of a debt crisis to countries that have a strong record of being fiscally responsible (Mendoza and Ostry, 2007). Such a track record gives them latitude to decide not to raise taxes or cut productive spending when the debt level is high (Ostry and others, 2010; Ghosh and others, 2013). And for countries with a strong track record, the benefit of debt reduction, in terms of insurance against a future fiscal crisis, turns out to be remarkably small, even at very high levels of debt to GDP. For example, moving from a debt ratio of 120 percent of GDP to 100 percent of GDP over a few years buys the country very little in terms of reduced crisis risk (Baldacci and others, 2011).

But even if the insurance benefit is small, it may still be worth incurring if the cost is sufficiently low. It turns out, however, that the cost could be large—much larger than the benefit. The reason is that, to get to a lower debt level, taxes that distort economic behavior need to be raised temporarily or productive spending needs to be cut—or both. The costs of the tax increases or expenditure cuts required to bring down the debt may be much larger than the reduced crisis risk engendered by the lower debt (Ostry, Ghosh, and Espinoza, 2015). This is not to deny that high debt is bad for growth and welfare. It is. But the key point is that the welfare cost from the higher debt (the so-called burden of the debt) is one that has already been incurred and cannot be recovered; it is a sunk cost. Faced with a choice between living with the higher debt—allowing the debt ratio to decline organically through growth—or deliberately running budgetary surpluses to reduce the debt, governments with ample fiscal space will do better by living with the debt.

Austerity policies not only generate substantial welfare costs due to supply-side channels, they also hurt demand—and thus worsen employment and unemployment. The notion that fiscal consolidations can be expansionary (that is, raise output and employment), in part by raising private sector confidence and investment, has been championed by, among others, Harvard economist Alberto Alesina in the academic world and by former European Central Bank President Jean-Claude Trichet in the policy arena. However, in practice, episodes of fiscal consolidation have been followed, on average, by drops rather than by expansions in output. On average, a consolidation of 1 percent of GDP increases the long-term unemployment rate by 0.6 percentage point and raises by 1.5 percent within five years the Gini measure of income inequality (Ball and others, 2013).

…

These findings suggest a need for a more nuanced view of what the neoliberal agenda is likely to be able to achieve. The IMF, which oversees the international monetary system, has been at the forefront of this reconsideration.

For example, its former chief economist, Olivier Blanchard, said in 2010 that “what is needed in many advanced economies is a credible medium-term fiscal consolidation, not a fiscal noose today.” Three years later, IMF Managing Director Christine Lagarde said the institution believed that the U.S. Congress was right to raise the country’s debt ceiling “because the point is not to contract the economy by slashing spending brutally now as recovery is picking up.” And in 2015 the IMF advised that countries in the euro area “with fiscal space should use it to support investment.”

On capital account liberalization, the IMF’s view has also changed—from one that considered capital controls as almost always counterproductive to greater acceptance of controls to deal with the volatility of capital flows. The IMF also recognizes that full capital flow liberalization is not always an appropriate end-goal, and that further liberalization is more beneficial and less risky if countries have reached certain thresholds of financial and institutional development.

Chile’s pioneering experience with neoliberalism received high praise from Nobel laureate Friedman, but many economists have now come around to the more nuanced view expressed by Columbia University professor Joseph Stiglitz (himself a Nobel laureate) that Chile “is an example of a success of combining markets with appropriate regulation” (2002). Stiglitz noted that in the early years of its move to neoliberalism, Chile imposed “controls on the inflows of capital, so they wouldn’t be inundated,” as, for example, the first Asian-crisis country, Thailand, was a decade and a half later. Chile’s experience (the country now eschews capital controls), and that of other countries, suggests that no fixed agenda delivers good outcomes for all countries for all times. Policymakers, and institutions like the IMF that advise them, must be guided not by faith, but by evidence of what has worked.

Vir: Ostry, Loungani & Furceri, 2016

Tomaž Mastnak je eden redkih domačih avtorjev, ki je o neoliberalizmu izdal tudi (zaenkrat svežo) knjigo. En daljši citat iz intervjuja z njim:

“O neoliberalizmu pišem kot o militantni družbeni teoriji in političnem gibanju, in ne kot o ekonomski doktrini, ker je militantno politično gibanje, ki brezkompromisno udejanja svoj specifični pogled na družbo, in ne ekonomski nauk. Da neoliberalizem nikdar ni bil ekonomska teorija, trdijo ugledni ekonomisti in ne zgolj kritični levičarski teoretiki. Zamisel, da je trg temeljni družbeni regulativni mehanizem, je ideja o delovanju družbe, ne pa ekonomski umislek. Pri predpostavki, da je treba državo zvesti na minimum, gre prav tako za socialno in politično idejo, ne pa za ekonomsko logiko. Neoliberalistični individualizem je filozofija – če še tako slaba – in enako velja za neoliberalistično teorijo vednosti, s katero razlagajo delovanje tržnih subjektov. Tovrstne teorije ne izhajajo iz študija ekonomije, temveč ga usmerjajo. Niso izpeljane iz razumevanja ekonomije, ampak narekujejo njeno specifično razumevanje.”

http://www.pogledi.si/ljudje/levico-je-lahko-dvakrat-sram

Sam menim, da neoliberalizem ni le militantno, elitistično politično gibanje, ampak strategija preživetja samega kapitalizma in zastopnikov kapitala. Na kratko, zakaj je šlo kapitalizmu po 2. svetovni vojni bolje kot kdajkoli? Ne le zaradi redistributivnih keynesijanskih ekonomskih politik, ampak predvsem zato, ker je se je med svetovno vojno uničilo toliko vrednosti, da je imel kapitalizem maneverski prostor širjenja in rasti.

Neoliberalizem dela točno to, kadar kapitalizem pade v škripce, uničuje dosežene standarde, znižuje plače, znižuje delavske pravice in z nadaljno “osvoboditvijo” kapitala otežuje možnost resnega upora. Neoliberalizem je nadvse učinkovit ideološki odgovor na to kako v miroljubnih časih uničiti vrednost in povečati profitabilnost kapitala, ki je resnična življenjska kri kapitalizma, konec koncev pa tudi edina prava motivacija, da je z vidika elit kapitalizem sploh videti smiseln. Ko kapitalizem ne bo več primerno profitabilen, z vidika elit ne bo več smiseln in si bodo želele drugačnega, morda še hujšega sistema.

Všeč mi jeVšeč mi je