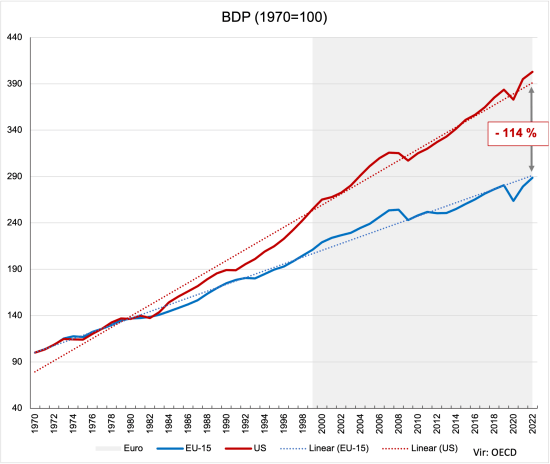

S prvim januarjem je evro praznoval 25 let obstoja. O tem, ali je bil to uspešen projekt, ali ne, pišem danes v kolumni v Dnevniku. V nadaljevanju je analiza, ki je podlaga za kolumno in kjer primerjam relativno “uspešnost” držav z evrom glede na ZDA. Pred in po začetku evropske monetarne unije. Vzel sem serijo podatkov o rasti BDP, ki je na voljo v OECD statistični bazi (na žalost je popolna serija šele od leta 1971 naprej). Prva slika kaže trend rasti BDP med jedrno skupino EU držav (stare članice EU in kasneje prve članice evro območja). Kot je razvidno, so jedrne EU države do sredine 1980. let rasle po enakih stopnjah kot ZDA, nato še nekako držale korak z ZDA do začetka 1990. let, nakar so ZDA pospešile rast. Med 2000 in 2008 so EU države spet rasle po podobnih stopnjah kot ZDA, prava divergenca pa se začne po letu 2008, kjer se ZDA nadaljevale rast v skladu z dolgoročnim trendom, medtem ko se je trend rasti EU držav močno upočasnil.

Trendi so bolje razvidni, če časovno serijo razdelimo na dva dela – na obdobje pred evrom (do 1998) in po evru (od 1990 naprej). V obeh slikah spodaj sem kot bazno leto izbral leto 1998 (zadnje leto pred uvedbo evra). Prva slika kaže, da so v obdobju pred evrom EU države glede trendne rasti zaostajale v povprečju le za nekaj več od 0.2 odstotne točke letno (povprečna rast EU-15 1.8%, ZDA 2%).

Druga slika pa kaže, da se je trendna rast jedrnih EU držav po letu 1999 (uvedba evra) upočasnila v povprečju na 1.4% letno in začela močno zaostajati za ZDA, ki so trendno rast celo pospešile iz 2% na skoraj 2.5% letno.

Ključna razlika, kot lahko vidite, se je zgodila po letu 2008, po veliki finančni krizi. ZDA so si hitro opomogle in se vrnile k prejšnji trendni rasti (oziroma celo hitrejši rasti kot v povprečju let 1971-1998), medtem ko so jedrne EU države povsem zablokirale v okrevanju zaradi institucionalnih težav in se k rasti vrnile šele po letu 2014.

Seveda ne moremo trditi, da je evro kriv za nižjo gospodarsko rast in za prelom v rasti po letu 1999, kajti na delu so bili številni dejavniki, kot so manjša inovativnost, nižji tehnološki napredek ter nižja rast produktivnosti v EU državah, slabša demografija v EU državah zaradi manjšega pritoka migracij in podobno. Vendar pa je imel evro ključen učinek glede dveh stvari. Prvič, zaradi skupne valute je izpadel nekdanji avtomatski mehanizem izravnavanja zunanjetrgovinskih neravnotežij prek sprememb tečajev nacionalnih valut, zaradi česar je prišlo do povečanjih zunanjetrgovinskih neravnotežij v prvih osmih letih po uvedbi evra. Nemčija je na eni strani močno povečala zunanjetrgovinski presežek, periferne evrske države pa so ustvarjale velike primanjkljaje (v primeru nacionalnih valut do tega ne bi prišlo v takšnem obsegu zaradi avtomatskega sankcioniranja deviznih tečajev). To pa je prek kapitalskih tokov privedlo do velikih makroekonomskih neravnotežij in nastanka kapitalskih in nepremičninskih balonov pred krizo leta 2008. Za finančno krizo iz leta 2008 je glavni krivec evro zaradi dizajna skupne monetarne unije, ko ni bilo več avtomatskih mehanizmov za odpravo trgovinskih neravnotežij in ko imamo popolno mobilnost kapitalskih tokov med državami.

Drugi negativni učinek evra pa prav tako sledi iz dizajna monetarne unije oziroma institucionalne ureditve ekonomskih politik, ki so zavirale hitrejše okrevanje EU držav. Prva je skupna monetarna unija, kjer ECB (vse do marca 2015) ni sledila vzoru ameriškega Feda, britanske BoE in Japonske BoJ glede politike kvantitativnega sproščanja, ki je omogočila refinanciranje finančnega sektorja z odkupom obveznic in znižanje obrestnih mer državnih obveznic, kar je dalo fiskalni prostor vladam za povečanje fiskalnega stimulusa. Druga pa skupni fiskalni okvir EU držav (najprej Pakt o stabilnosti in rasti in nato od leta 2010 Fiskalni pakt), ki je bil od leta 2010 v EU zastavljen zelo restriktivno in je kljub veliki krizi od članic EU zahteval fiskalno konsolidacijo namesto, da bi omogočil ekspanzivno fiskalno politiko. Oboje skupaj je države EU držalo v globoki stagnaciji dolgih šest let, medtem ko so ZDA galopirale naprej.

Torej evro ni kriv za celotno zaostajanje v trendni rasti držav z evrom glede na ZDA, njegova krivda pa je v dizajnu monetarne unije, ker po eni strani generira makroekonomska neravnotežja (ki jih brez njega ne bi bilo oziroma bi bila manjša), na drugi strani pa z institucionalnim ustrojem omejuje države glede spodbujanja rasti (skupna monetarna politika in skupni fiskalni okvir). Zaradi tega bodo države z evrom pogosteje padale v krize in se težje iz njih izvijale in zaradi tega bo trendna rast držav z evrom nižja kot bi bila, če bi imele države lastno valuto in avtonomne ekonomske politike.

Del teh težav bi se dalo odpraviti z opustitvijo ali relaksacijo skupnega fiskalnega okvirja in z uvedbo transferne unije (denimo s skupnim skladom za zavarovanje glede brezposelnosti in skupnimi evro obveznicami). Toda to so zaenkrat bolj pobožne želje ekonomistov kot bližnja politična prihodnost.

Ključno pa je, da evro ni prispeval k večji stabilnosti, hitrejši rasti in h konvergenci (zbliževanju) med državami z evrom, kot so si obetali in obljubljali kreatorji evra, pač pa je nasprotno prispeval k večji nestabilnosti, k zaviranju rasti držav z evrom in k divergenci med njimi. Slednje se lepo vidi v spodnji sliki za štiri največje države z evrom. Do prevzema evra leta 1999 so te države rasle po podobnih trendnih stopnjah, po prevzemu evra pa so njihove rasti postale izjemno volatilne in disperzija njihovih stopenj rasti se je močno povečala (t.i. sigma divergenca se je povečala).

To povečano divergenco zaradi ustroja evrske monetarne unije potrjuje tudi študija IMF, ki prav tako identificira povečano nestabilnost v obliki povečanih amplitud nihanj različnih ekonomskih kazalcev med državami. Na luzerski strani se je znašla predvsem Italija, ki je po prevzemu evra komajda kaj zrasla, medtem je Španiji uspevalo zadržati višje stopnje rasti zaradi primarnega učinka konvergence manj razvitih držav.

O tem, da evro ni bistveno povečal medsebojne trgovine med evrskimi državami, kar je bila tudi ena izmed tez kreatorjev evra pred njegovo uvedbo, pa je bilo narejeno ogromno analiz. Napovedi so bile, da bo zaradi eliminacije valutnega rizika evro povečal trgovino za dvakrat, dejanski učinki pa so bili mizerni (dodatno povečanje trgovine med članicami za 4 do 10%). In pokazalo se je nasprotno, trgovina z nečlanicami se povečuje hitreje, kar govori o tem, da eliminacija valutnih tveganj z evrom po predhodnih dveh desetletjih že fiksiranih tečajev ni bila pomembna. Ob 20. obletnici evra, leta 2019, je nekdanji visoki uradnik IMF Ashoka Mody napisal uničujočo kritiko evra. Kratek povzetek ključnih točk:

- Evro je nujen za skupni trg: Ne drži.

- Evro spodbuja trgovino med članicami: Ne drži, velja kvečjemu nasprotno – trgovina z nečlanicami se povečuje hitreje.

- Evro spodbuja konvergenco med članicami: Nasprotno, po uvedbi evra se konvergenca med članicami zmanjšuje – države brez evra rastejo hitreje.

- Evro je nujen za makroekonomsko stabilnost: Ne velja, evro je zaradi fiksacije valutnih tečajev in fiskalnih pravil zmanjšal sposobnost držav za blaženje šokov in povečal makro nestabilnost.

Thomas Fazi ima torej v spodnjem članku prav, ko pravi, da je bil evro sicer uspeh evrokratov in finančnih elit, za gospodarstva držav z evrom in za EU kot celoto pa je bil polom.

_______________

On January 1, as the European Union ushered in another year of economic chaos and not-so-distant wars, no one was in the mood to celebrate the euro’s 25th birthday. No one, that is, but the Eurocrats.

…

Since 2008, the euro area has essentially been stagnating — and its overall long-term growth trend has been negative. This has led to a dramatic divergence between its economic fortunes and those of the US: adjusted for differences in the cost of living, the latter’s economy was only 15% larger than the euro area’s economy in 2008; it is now 31% larger. Today, the euro’s share of global currency reserves is significantly lower than its predecessors — the Deutsche Mark, French franc and ECU — in the Eighties.

But this is far from the only result of the euro’s failure. When it was introduced, it was hoped that the single currency’s “culture of stability” would narrow the difference in terms of its members’ economic performance. In effect, as the IMF has noted, the opposite has happened: “the envisaged adjustment mechanisms under monetary union have been insufficient to support convergence, and have in some cases contributed to divergence”. Added to this, exports between euro nations as a percentage of total eurozone exports have been on a downward trend since the mid-2000s.

It seems clear, then, that the introduction of the euro was a mistake — but only if we take its proponents’ stated intentions at face value. For it is important to understand that the euro was always as much a political project as an economic one. And, from that standpoint, it has been an extraordinary success.

There’s a reason the foundations of the monetary union were only laid in the early Nineties, even though the idea had been around since 1970. That year, the first report examining the feasibility of monetary union was published. Known as the Werner Report, it stressed that, in addition to the creation of a European central bank as the issuer of the new single currency, “transfers of responsibility from the national to the Community plane will be essential” for the conduct of economic policy.

Seven years later, the MacDougall Report reinforced the need for a sizeable EU budget — of 5% or more of EU GDP — to underpin any European monetary union, with responsibility for it handed to a European Parliament. Given the reluctance of member states to move towards a fully-fledged monetary and fiscal union, which would have involved significant transfers between countries, the plans for monetary union floundered for another decade. However, new life was then breathed into the euro project in the late Eighties and early Nineties — not because the economics of the project had improved, but because the politics around the idea of monetary union had changed, especially at the level of Franco-German relations.

The official story is that the French, who had always been particularly reluctant to agree to any supranational authority, came round to the idea of a monetary union in the wake of German reunification, as a way of “shackling” German power. Germany, meanwhile, relinquished its much-loved national currency, the symbol of its post-war economic achievement, in order to quell concerns about its growing hegemony.

The reality, in fact, was more complicated. It is true that France hoped that monetary integration would constrain Germany. But France was also influenced by domestic developments — in particular the French Socialists’ neoliberal turn in the early Eighties, under Mitterrand. This led it to embrace the idea that “national sovereignty no longer means very much” and that “a high degree of supranationality is essential”, as Mitterrand’s finance minister, Jacques Delors, put it — an idea that Delors would then export to the rest of Europe during in his role as President of the European Commission from 1985 to 1995.

As for Germany, the notion that the country reluctantly accepted to have the euro foisted upon itself, in exchange for its European partners’ acceptance of reunification, is largely a myth. German elites were perfectly aware that the eurozone would give an immense boost to Germany’s export-led mercantilist strategy, by ensuring a significantly lower exchange rate with the euro than it would have had with the Deutsche Mark, even in the face of persistent trade surpluses. In other words, the German elites viewed the euro as a way of reasserting their hegemony over Europe — the exact opposite of what the French were hoping to achieve.

For a while at least, history would prove the Germans right. They seized the opportunity to ensure that the future monetary union would be functional to German interests, partly by getting other member states to agree to the creation of a fully independent central bank — that is, fully insulated from a democratically elected polity — with the sole mandate of ensuring price stability. No wonder Helmut Kohl, Germany’s Chancellor, admitted to pushing through the euro “like a dictator” in face of a reluctant public, while Theo Waigel, his finance minister, boasted about “bringing the Mark in Europe”.

Why did other countries agree to join a monetary union destined to boost the German economy at the expense of other less export-dependent economies, such as Italy? There were certainly ideological elements at play, such as the rise of monetarism, but, as with France, the reasons were mostly political rather than economic. By the early Nineties, national elites in most European countries had come to view the euro as a “Trojan horse” with which to push through neoliberal policies for which there was little political support, by engaging in what Kevin Featherstone has called a “‘blameshift’ towards the ‘EU’”.

Moreover, by explicitly prohibiting the ECB from acting as lender of last resort and forcing states to rely solely on loans from the financial markets for their financing needs, the idea was that representative democratic institutions would be subject to the supposed “discipline” of the markets. Angela Merkel coined a rather ominous term for such a system: “market-conforming democracy”.

In short, the euro saw the light of day because national elites came to embrace the idea for different but convergent reasons: in some cases (such as Germany), it was a matter of gaining an economic advantage at the expense of other countries; in others (Italy, for example), it was a matter of gaining an advantage at the expense of domestic actors, even if that cost economic growth.

The result was an extremely dysfunctional monetary union. And when the financial crisis hit, and a series of credit-led economic booms — fuelled by massive capital flows from Europe’s core to the periphery — went bust, the implications of its structure hit home. Those members in a slump could not devalue. Since they could not print their own money, and because the central bank was unwilling to act as lender of last resort, they risked sovereign default, or national insolvency, as they came under attack from financial markets. Essentially, the euro was their downfall.

Yet, by late 2010, European elites — the Germans, in particular — had rewritten history. The financial crisis was not the fault of an out-of-control system exacerbated by the dysfunctional nature of the monetary union; it was, they claimed, the fault of excessive government debt inflated by countries that had “lived well beyond their means”. The fact that most euro countries had registered primary fiscal surpluses in years leading up to the financial crisis, and that public debts had exploded only in the latter’s aftermath as a result of the massive bank bail-outs, was conveniently brushed aside. There was only one possible “cure”, Europe’s leaders proclaimed: austerity. The leading proponent of this theory was Germany’s ultra-hawkish finance minister, Wolfgang Schäuble, who died last week.

The imposition of such harsh fiscal austerity measures across the eurozone didn’t just raise unemployment, erode social welfare, push populations to the brink of poverty and create a genuine humanitarian emergency — it also completely failed to achieve the stated aims of kickstarting growth and reducing debt-to-GDP ratios. Instead, it drove economies into recession and increased debt-to-GDP ratios. Meanwhile, democratic norms were dramatically upended, as entire countries were essentially put into “controlled administration”. The result was a “lost decade” of stagnation and permacrisis that led to a profound divide between the eurozone’s north and south, and brought the monetary union to the brink.

This wasn’t simply the “automatic” outcome of the defective architecture of the monetary union. Rather, the European “sovereign debt crisis” of 2009-2012 was largely “engineered” by the ECB (and Germany) to impose a new order on the continent. Indeed, former ECB president Jean-Claude Trichet made no secret of the fact that its refusal to support public bond markets in the first phase of the financial crisis was aimed at pressuring eurozone governments into consolidating their budgets and implementing “structural reforms”. But the ECB then went further, resorting to various forms of financial and monetary blackmail — most notably in Ireland, Greece and Italy — with the aim of coercing governments to comply with the overall political-economic agenda of the EU.

In this sense, we could say that the euro crisis was both an economic disaster and a political success for Europe’s financial-political elites. After all, it allowed them to radically restructure and re-engineer European societies and economies along lines more favourable to capital, while creating one of the single biggest upward transfers of wealth in history — all in the name of the allegedly inescapable realities of the euro.

Since then, not much has changed in terms of the inner workings of the monetary union. Even the temporary suspension of the EU’s fiscal rules during the pandemic is in the process of being curtailed; a rehashed but fundamentally unchanged version of the EU’s fiscal framework is set to come back into force this year, spelling the return of austerity to the continent. That Germany has fallen from grace in the process, going from unchallenged European hegemon to American vassal-in-chief, is one of the great ironies of the past decade.

Nonetheless, when European elites say that the euro has been a success, they are unwittingly revealing a truth. From their perspective, it undoubtedly has; and their greatest success has arguably been to convince everyone that there is no alternative. To paraphrase Mark Fisher, it’s easier to imagine the end of the world than the end of the euro.

Vir: Thomas Fazi; Unherd

You must be logged in to post a comment.