Glavna skupna lastnost vseh ekonomskih napovedi je, da … se vedno zmotijo. Jaz na različnih javnih predstavitvah rad povem slab vic o ekonomistih, in sicer:

Kako vemo, da imajo ekonomisti smisel za humor?

Ker svoje napovedi oblikujejo na decimalko natančno.

V realnem življenju namreč znaša (pri našem najbolj uveljavljenem inštitutu in pri drugih mednarodnih inštitucijah je zelo podobno) povprečna absolutna napaka glede napovedi rasti BDP 2 odstotni točki. To pomeni, da če napoved rasti znaša 2% za naslednje leto, bo gospodarska rast najbolj verjetno znotraj razpona med 0% in 4%. Seveda je pa pogosto tudi izven v primeru nenadnih šokov.

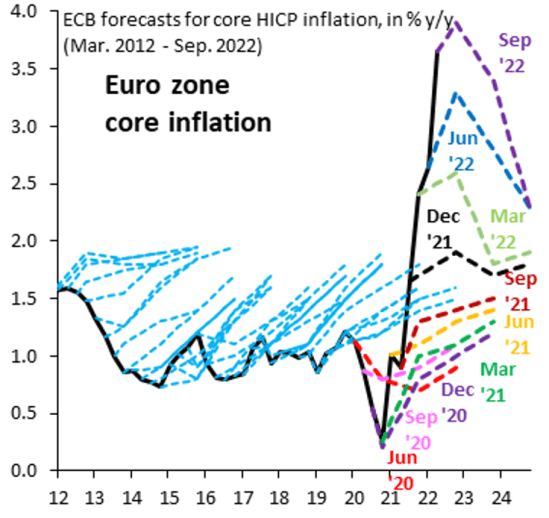

Najhujši napovedovalec je najbrž res ECB glede inflacije. ECB ima tendenco, da se glede napovedi inflacije sistematično moti v nasprotno smer. V času inflacije, nižje od ciljne (2%), napoved inflacije za 3 leta vnaprej vedno kaže zvišanje inflacije in da se bo približala ciljni 2-odstotni inflaciji. In obratno pri višji inflaciji od 2%, kjer napoved ECB za 3 leta vnaprej vedno kaže, da se bo infflacija znižala in približala 2%. Poglejte spodnjo sliko glede napovedi (polna temna črta je dejanska stopnja temeljne inflacije, črtkane črte so napovedi za 3 leta vnaprej). Kolikokrat je v zadnjih 10 letih ECB zadela smer, kaj šele stopnjo inflacije? Sami si odgovorite na to vprašanje.

V čem je problem teh napovedi ECB (ter napovedi ostalih inštitucij)? Problem je v sistematski pristranosti napovedi. Na eni strani, kadar gre za uporabo ekonomskih modelov, je njihov problem v tem, da vsi temeljijo na predpostavki steady-stata, torej da se po šoku gospodarstvi vrne v ravnotežno stanje . v stanje polne zaposlenosti (upoštevajoč naravno stopnjo brezposelnosti) in stabilne ravni cen. Ergo, vse simulacije morajo pripeljati do napovedi, kot so inherentno vgrajene v modelsko strukturo. Na drugi strani pa je problem pristranosti, predvsem monetarnih oblasti, v tem, da pričakujejo, da se bo na podlagi njihovega ukrepanja bodoča dinamika res razvila v smeri, kot jo napovedujejo. Če je cilj centralne banke 2-odstotna inflacija, potem računa, da bo z monetarno politiko gospodarstvo v zastavljenem roku res pripeljala v željeno stanje in dosegla željeno stopnjo inflacije. Kar pa seveda nikakor ne pomeni, da se bo to res zgodilo in se običajno nikoli ne zgodi. Razen slučajno.

No, problem pristranosti napovedovalcev in njihovih modelov je glavni razlog, zakaj so ekonomske napovedi tako slabe. Zadevo lepo prikazuje spodnji zapis s tekmovanja ekonomskih napovedovalcev. Letos je zmagal mlad doktorski študent ekonomije iz Češke, katerega napovedni model nima vgrajenih nobenih pričakovanj in temelji na preteklih vzorcih, pač pa se model sproti uči na podlagi novih podatkov. Čista stohastika. To je seveda velik udarec za strukturne modele, ki imaj vgrajeno strukturo “obnašanja” agentov, pa tudi za modele, ki temeljijo na statistični analizi preteklih dogodkov.

To seveda tudi pomeni, da lahko velike mednarodne institucije, centralne banke, ekonomski inštituti, velike banke itd. zaprejo svoje oddelke za napovedovanje in namesto tega prevzamejo modele, ki temeljijo na nevronskih mrežah in učenju. Ampak hudič je, da to pomeni, da lahko teorije, na katerih utemeljujemo razumevanje delovanja gospodarstva in kar učimo študente in s čimer centralne banke poskušajo vplivati na gospodarstvo, vržemo na smetišče. Ups! To je velik udarec za tiste, ki so verjeli, da je ekonomija zgolj podveda fizike.

__________

The Makridakis Open Forecasting Centre at the University of Cyprus has been running a fascinating forecasting competition between old and new world models for some years now. The interesting thing about these competitions is not really who wins, but what type of modelling approaches work best. The trend seems to favour modern neural networks. The latest competition was on stock market forecasting. The new world won hands down, with a couple of notable exceptions. We wrote about this before, but today we would like to emphasise an important aspect. It is all about bias.

Kudos to everybody who took and who allowed themselves to be counted out in the full light of public scrutiny. We noted one entry from the financial forecasting team at Oracle, which used highly sophisticated statistical methods, and which did very well at one point but ended in some middle position in the end. Their method is very much premised on the idea that anything that happens today had been matched by previous episodes. Their method was to find those episodes that match our current situation the closest. In fairness, their approach is much more sophisticated than what we outlined, but it is ultimately an approach based on historic patterns.

The winning entry, by a young economics student from the Czech Republic, used an approach called meta learning: learning how to learn. This type of model does not know what it wants from the outset. It chooses its own models as more data come in. This is an important trend in forecasting because it addresses the single most important problem of all forecasting including some modern machine learning methods, that of forecasting bias. The belief in technical historic patterns constitutes a bias. So does the pre-determined choice of any specific modern machine learning method like specific types of neural networks. So does the assumption inherent in central bank forecasting models that the central bank can guide expectations through inflation targets and communications. This is why inflation forecasts always predict a return to the target. Central bank forecasting models are the ultimate bias-machines. They constitute an attempt to objectivise prejudices. New Keynesians do not only disagree with monetarists. They also produce different forecasts.

The reason why meta learning outperforms both of them is the lack of bias. We noted before that the ECB’s forecasting is so terrible that it is outperformed by a pure random process, the proverbial monkey with a dart board. We would love to see an economic forecasting competition, but doubt very much that economic forecasters would want to enter a competition with non-economists. We also note a generalised absence of a critical review of economic forecasting performances. Years ago, we remember one independent review of the European Commission’s economic forecast, commenting that it achieved the rare success, if you want to call it, of a correlation coefficient of exactly zero when measured against the future outcomes. The researcher noted it is quite rare for a model to be so bad that it hits zero precisely.

A policy lesson from this is that you would do better if you closed down your forecasting department, and replaced it with one of the modern methods. What makes them superior is the lack of bias.

It also has been our observation that the successful investors we met did not have a better theory or better models, let alone access to exclusive information. Different methods yield different results for sure. What they had in common was an ability to take bias out of their own thinking, which is a rare skill.

Vir: Eurointelligence

You must be logged in to post a comment.