Najbrž spremljate kolaps Silicon Valley Bank (SVB), banke, katere poslanstvo je financiranje tehnoloških start-upov (zagonskih podjetij). Najbolj fascinantno pri tej zgodbi je paradoks, da je propadla banka, ki se je “kopala” v presežni likvidnosti in ki je to svojo likvidnost zaradi varnosti naložila v najbolj varne možne naložbe – večinoma v ameriške državne obveznice (treasuries). Za razliko od denimo Lehman Brothers iz leta 2008, ni propadla investicijska banka, ki je zbrana sredstva investirala v rizične obveznice, ki so temeljile na “poolih” slabih kreditov za nakupe nepremičnin, pač pa banka, ki je svoje obveznosti (depozite tehnoloških podjetij) zavarovala z investiranjem v najbolj varne možne naložbe. Kako je to mogoče?

Vendar je zgodba absolutno logična in je posledica restriktivne monetarne politike ameriškega FED. Bilo je samo vprašanje časa, kdaj bo dvigovanje obrestnih mer s strani FED privedlo do zloma. Tako kot je leta 2008, takrat zaradi posledičnega dviga obrestnih mer za stanovanjske kredite. Za razumevanje kolapsa SVB je treba razumeti dvoje. Prvič, poslanstvo SVB je bilo financiranje zagonskih podjetij, ta podjetja pa so pri SVB v obliki večinoma odprtih (nezavarovanih) depozitov držala svoja sredstva za tekoča plačila svojih obveznosti. Marca letos se je v bilanci SVB nabralo za več kot 170 milijard dolarjev depozitov, od tega 150 milijard dolarjev nezavarovanih. Na drugi strani bilance so bili ti depoziti zavarovani z naložbami v pretežno državne obveznice v nominalni vrednosti več kot 210 milijard dolarjev (slika spodaj). Absolutno dovolj za mirno morje in absolutno dovolj za stabilno monetarno politiko. Toda morje se je močno razburkalo, ko je Fed lani spomladi začel drastično dvigovati obrestno mero.

In, drugič, glede nadaljevanja je treba razumeti inverzno relacijo med obrestno mero na obveznico in vrednostjo obveznice (kar je osnova poslovnih financ): če se obrestna mera dvigne, se ustrezno zmanjša vrednost obveznice. Torej vsakič, ko je FED dvignil obrestno mero za 50 ali 75 bazičnih točk, se je zmanjšala vrednost “varnega” zavarovanja, ki ga je imela SVB v obliki državnih obveznic. Za vsak dvig obrestne mere za 25 bazičnih točk (0.25%) je SVB izgubila za okrog 1 milijardo dolarjev varnega kritja. FED pa je obrestne mere dvignil za 450 bazičnih točk. Problem je nastal, ko so tehnološka podjetja začela dvigovati depozite, SVB banka pa je za njihovo poplačilo morala prodajati vse manj vredne državne obveznice in v neki točki se je zgodba sprevrgla v tipični bank run (stampedo na dvigovanje depozitov), ki ga nobena banka ne more preživeti.

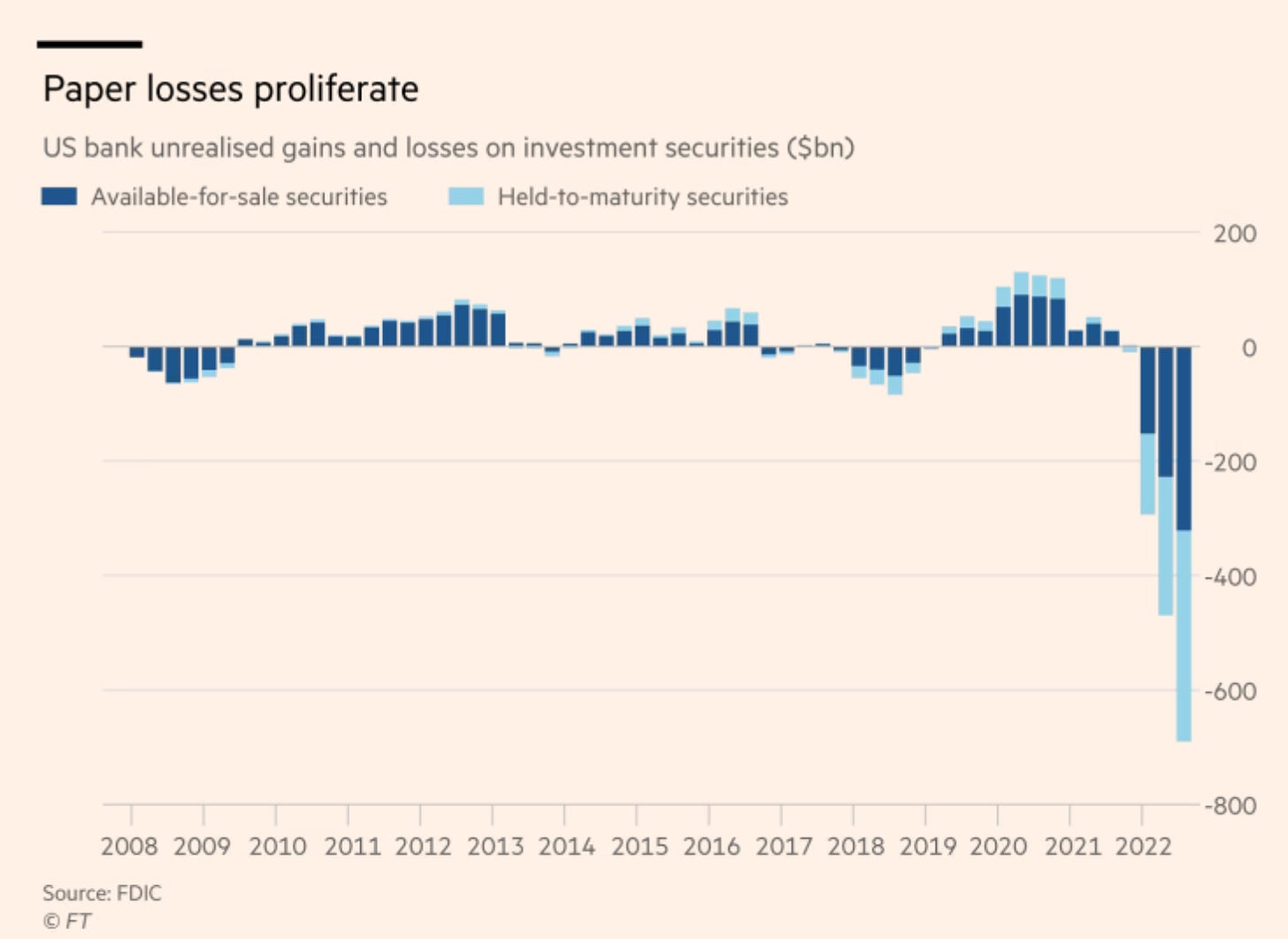

Kolaps SVB banke je torej produkt izjemno restriktivne monetarne politike FED. Vprašanje je, kaj se bo zgodilo z drugimi bankami. Tudi ostale banke imajo podoben problem. Konec tretjega četrtletja lani je obseg (še) nerealiziranih izgub zaradi padca vrednosti državnih obveznic v ameriškem bančnem sistemu znašal že 689 milijard dolarjev, od tega 321.5 milijard dolarjev nerealiziranih izgub pri obveznicah, ki so naprodaj. Druge banke so se za razliko od SVB sicer hedgale z investicijami tudi v druge naložbe, vendar lahko šok povzroči panično dvigovanje depozitov in bank run, če ne bodo ameriške finančne oblasti ustrezno in hitro odreagirale.

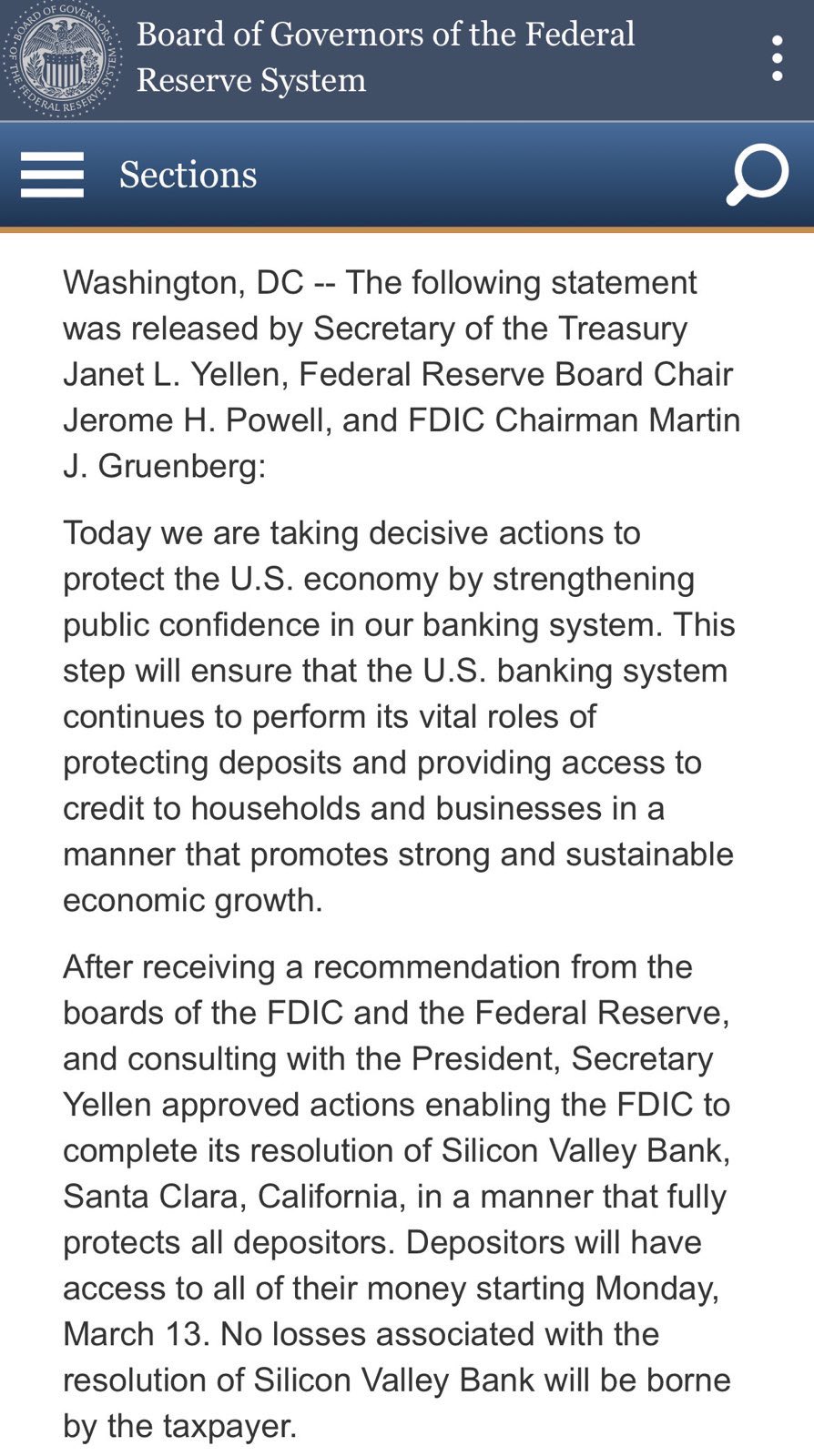

Preko vikenda so se pojavljale različne špekulacije, da ameriška vlada naj ne bi želela sanirati SVB oziroma prevzeti bremena depozitov (katerih varstvo pa je pri FDIC zajamčeno samo do višine 250,000 dolarjev). No, zadnje novice kažejo, da bo (namesto FDIC) FED (prek posebne družbe, i.e. SPV) poskrbel za varstvo depozitov, saj se boji podobnega učinka kot leta 2008, ko se oblasti niso odločile za reševanje Lehman Brother in kar je nato sprožilo verižno reakcijo prek zamrznitve medbančnega trga in privedlo do množičnih nesolventnosti finančnih institucij ter privedlo do največje finančne krize v razvitih državah po letu 1929. Zato Yellenova govori o “jačanju zaupanja javnosti v ameriški bančni sistem“:

Zanimivo pri vsej zgodbi je dvoje. Prvič, tudi najbolj varne naložbe ne omogočajo varnosti, kadar morje postane močno razburkano. In drugič, centralne banke delajo stres teste za vse mogoče negativne scenarije (od padca BDP do povečanja inflacije), pozabile pa so na scenarij tveganjam, ki ga same lahko povzročijo – drastično povečanje obrestnih mer. V naslednjih dneh bomo videli reakcijo FED glede politike nadaljnjega zaostrovanja monetarne politike, torej ali se bo ustrašil realizacije negativnih posledic svoje politike ali pa se na to ne bo oziral.

Za bolj radovedne je spodaj (kot vedno) dobro dokumentiran komentar Adam Toozeja o tej zadevi. Kasneje pa objavim še en ali dva druga pogleda.

_________

For a while we have been asking, as the Fed drives a global interest rate hike, what will bend and will break? The stress has been felt around the world. With Silicon Valley Bank’s collapse we now have a significant bank failure at the heart of a vital part of the US economy directly linked to the interest rate hike.

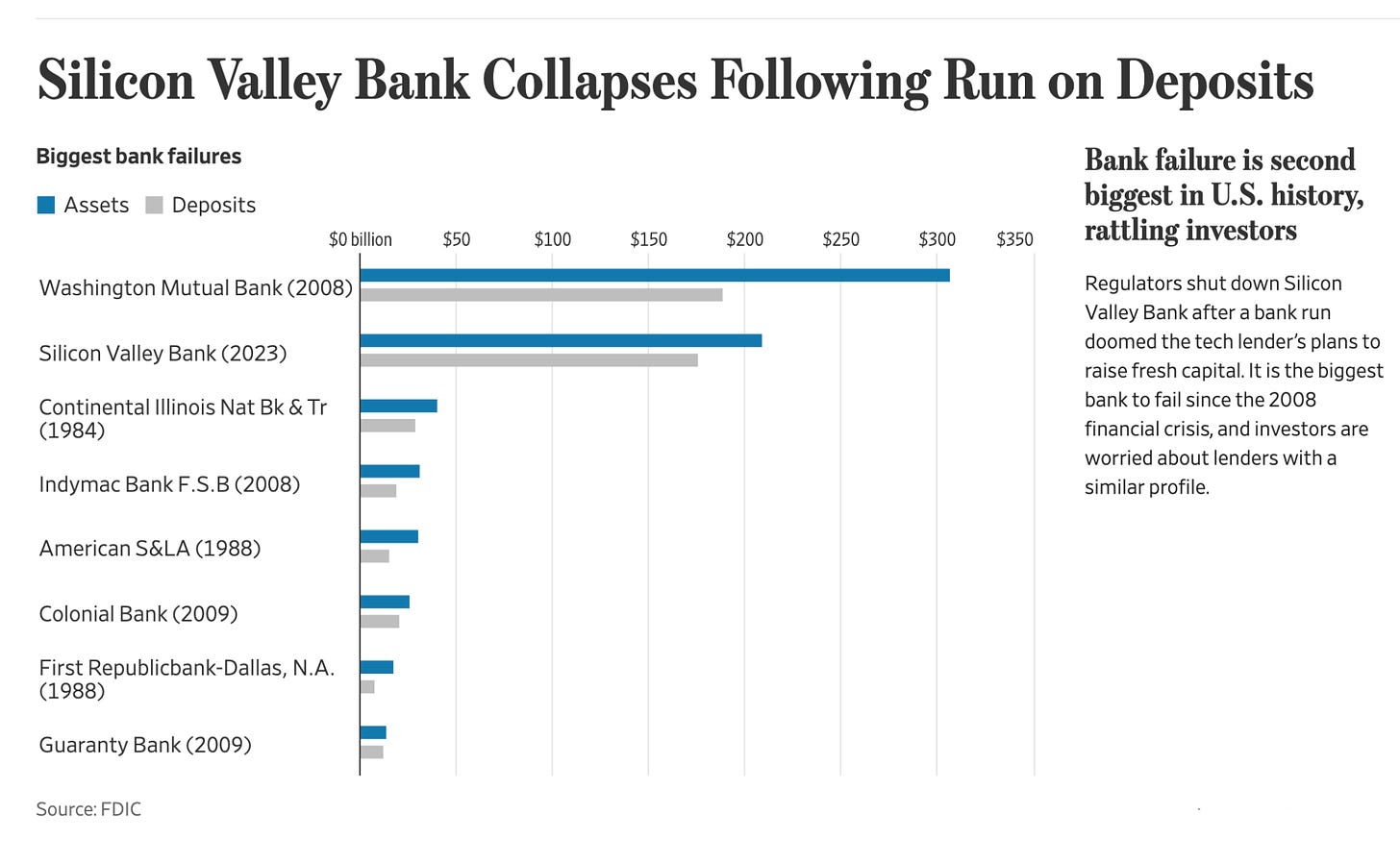

Silicon Valley Bank was not a small bank. It was the 16th largest in US financial system (and there are a LOT of banks in the US). Its collapse is the largest failure, by far, since 2008.

Source: WSJ

How did it happen? This by Noah Smith is really helpful, especially on the Silicon Valley side of the story, Peter Thiel etc

Noahpinion

Why was there a run on Silicon Valley Bank?

The big news in both the tech and financial worlds right now is the run on Silicon Valley Bank. SVB, as it’s known, was a bank that lent a lot of money to startups (or “startups”, i.e. bigger tech companies that are still private), and provided a lot of financial services to both startups and other tech companies. Here’s…

Read more

7 hours ago · 139 likes · 52 comments · Noah Smith

The immediate cause of bank failures is almost always a run. No bank however solvent can withstand a full-scale run. SVB was a VERY VERY runnable bank.

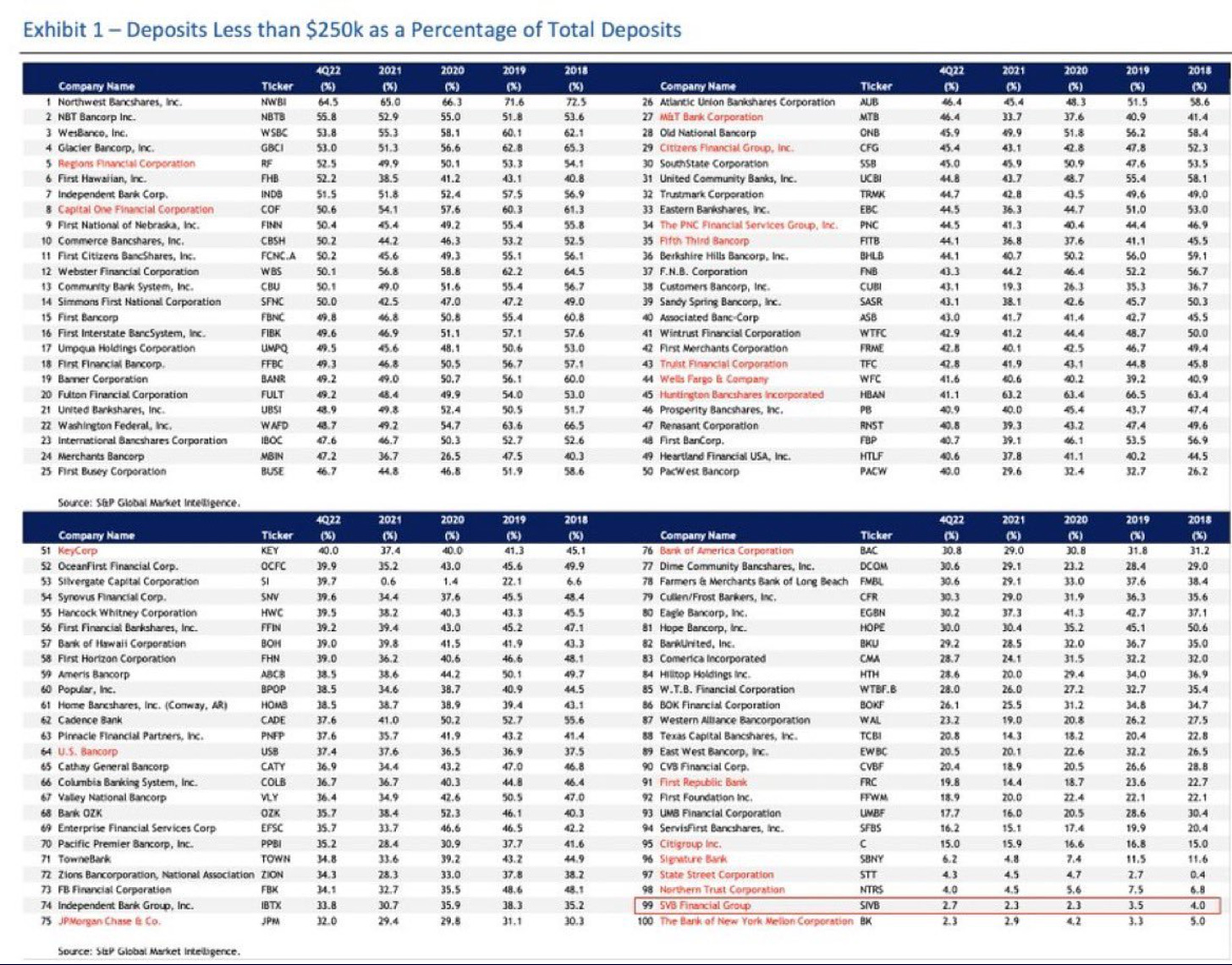

To prevent bank runs, the US, like most countries, offers guarantees, by way of the FDIC, to depositors who have deposits of less than $250,000. They will be made whole whatever happens and so have no incentive to run, whatever the state of the bank. The average bank in the US has about 50 percent of its deposits insured in this way. JP Morgan and Bank of America have c. 30 percent covered.

h/t Gian Luca

At SVB at the end of 2022 only 2.7 percent of deposits were covered by FDIC insurance! As Noah Smith explains:

Why did SVB have so many uninsured deposits? Because most of its deposits were from startups. Startups don’t typically have a lot of revenue — they pay their employees and pay other bills out of the cash they raise by selling equity to VCs. And in the meantime, while they’re waiting to use that cash, they have to stick it somewhere. And many of them stuck it in accounts at Silicon Valley Bank. If you’re a startup founder, why would you stash your cash in a small, weird bank like SVB instead of a big safe bank like JP Morgan Chase, or in T-bills? This is actually the biggest mystery of this whole situation. Some companies put their money in SVB because they also borrowed money from SVB, and keeping their money in SVB was a condition of their loan! For others, it was a matter of convenience, since SVB also provided various financial services to the founders themselves.

So SVB was a big accident waiting to happen. What pushed it over the edge?

Did SVB make speculative loans? Yes, some. But not enough by itself to blow it up. Did it engage in adventurous financial engineering? No! A large part of its depositors’ money was invested in what is supposed to be the safest part of the financial system, Treasuries and government-backed bonds like agency-backed Mortgage Backed Securities.

SVB adopted this strategy precisely in the hope of always having the cash on hand it needed to meet any cash withdrawals from its large depositors. As the FT reported already in late February.

At the peak of the tech investing boom in 2021, customer deposits surged from $102bn to $189bn, leaving the bank awash in “excess liquidity”. At the time, the bank piled much of its customer deposits into long-dated mortgage-backed securities issued by US government agencies, effectively locking away half of its assets for the next decade in safe investments that earn, by today’s standards, little income. Becker said the “conservative” investments were part of a plan to shore up the bank’s balance sheet in case venture funding of start-ups went into freefall. “In 2021 we sat back and said valuations and the amount of money being raised is clearly at epic levels . . . so we looked at that and were more cautious.” That decision also created a “stone anchor” on SVB’s profitability, said Oppenheimer research analyst Christopher Kotowski, and it had left the bank vulnerable to changing interest rates.

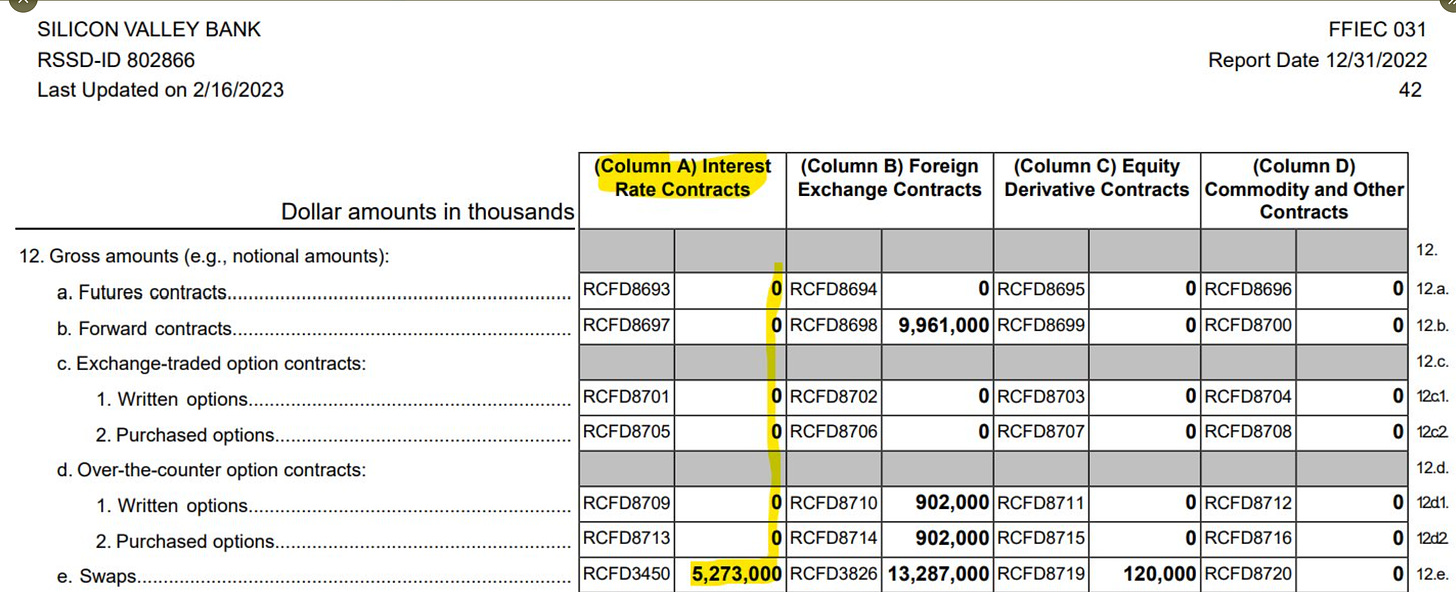

A portfolio of government backed bonds will be something you can sell. The question is what price do you sell it at and will you suffer a loss? In 2021 interest rates were still low and bond prices were high. SVB’s bonds looked like a safe piggybank. Then came the great inflation scare of 2022. The Fed hiked rates, bonds suffered their worst year in history. Why? Because bond prices go down as prevailing interest rates go up. At a rough guess SVB suffered at least a $1bn loss on its books every time interest rates went up by 25 basis points and the Fed has hiked by 450. So if they had to sell their “safe” portfolio of bonds they would actually suffer a huge loss.

Of course, SVB were not the only ones in this position. And for that reason there is a big market in interest rate hedges. Did SVB have interest rate hedges? No it didn’t.

h/t Joseph Wang

It was not holding a safe piggybank. It was, in effect, taking a huge $100-billion-plus, one-way bet on interest rates.

As Matt Levine summarized it in a single brilliant paragraph, tech fed off low interest rates:

And so if you were the Bank of Startups, just like if you were the Bank of Crypto, it turned out that you had made a huge concentrated bet on interest rates. Your customers were flush with cash, so they gave you all that cash, but they didn’t need loans so you invested all that cash in longer-dated fixed-income securities, which lost value when rates went up. But also, when rates went up, your customers all got smoked, because it turned out that they were creatures of low interest rates, and in a higher-interest-rate environment they didn’t have money anymore. So they withdrew their deposits, so you had to sell those securities at a loss to pay them back. Now you have lost money and look financially shaky, so customers get spooked and withdraw more money, so you sell more securities, so you book more losses, oops oops oops.

Tech-finance is, no doubt, “special”. But is SVB the only financial institution sitting on large losses on its bond holdings? NO it isn’t. Chartbook noted this back in December:

The big bank bond losses

For years big US banks have been piling excess cash into bonds. Following the pandemic there was a 44 per cent surge in their bond holdings, to $5.5 trillion.

In 2022 the Fed began a tightening cycle and those bonds took a serious beating, inflicting HUGE paper losses on the bank holdings.

Unrealized Losses on Securities Increased: Unrealized losses on securities totaled $689.9 billion in the third quarter, up from $469.7 billion in the second quarter. Unrealized losses on held-to-maturity securities totaled $368.5 billion in the third quarter, up from $241.8 billion in the second quarter. Unrealized losses on available-for-sale securities totaled $321.5 billion in the third quarter, up from $227.9 billion in the second quarter.

The distinction between HTM and AFS is all-important because as FT’s Lex explains

Banks can classify their security holdings as “held-to-maturity” (HTM) or “available-for-sale” (AFS). Those that are labelled HTM cannot be sold. But that means any changes in market value will not count in the formulas regulators use for calculating capital requirements. By contrast, any losses in the AFS basket have to be marked to market and deducted from the bank’s capital base.

The upshot. Even allowing for accounting help, there is a huge paper loss sitting on the balance sheet of America’s banks. Were there to be a liquidity squeeze, then a large part of the banks’ portfolios – the HTM part – could not easily be sold.

Lex finishes the year by warning:

For now, US banks remains awash in liquidity and are suffering no obvious financial stress. But rising deposit outflows and the increase in unrealised losses could become problematic if they need to sell investments to meet unexpected liquidity needs. Bond holdings could emerge as a serious pressure point for banks in volatile markets. Investors should watch out for this in 2023.

OK! … that was on December 27 2022. Two months later on 28 February the chair of the FDIC warned: “the combination of a high level of longer–term asset maturities and a moderate decline in total deposits underscores the risk that these unrealized losses could become actual losses should banks need to sell securities to meet liquidity needs.”

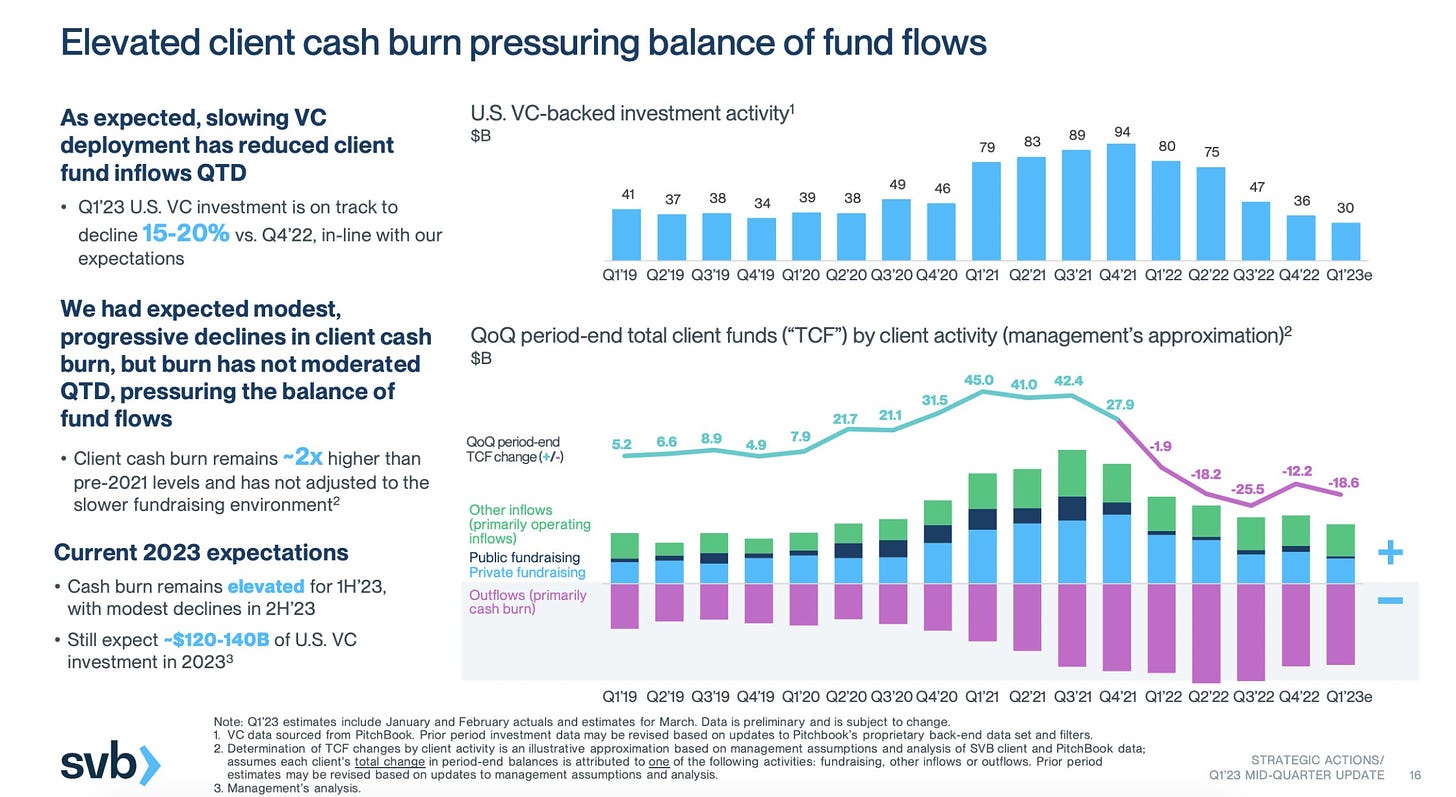

Guess where the outflows started in early 2023? The stressed tech sector! Since Q4 2021 VC activity has been declining in Silicon Valley and that was showing up in SVB’s balance sheet:

h/t Jack Farley

The panic began when SVB tried to raise capital to cover its losses. As Lulu Cheng explains this went terribly wrong.

Lulu Cheng Meservey @lulumeservey

SVB made the responsible decision to strengthen its financial position with a cap raise. It made sense. Where things went terribly wrong was the communication, specifically: (1) WHAT they said, (2) WHO the audience was, (3) WHEN they did it, and (4) HOW they framed it.

Standing back, how could SVB have ended up in this exposed position? Why was it not stress-tested? Because in 2018 the regulations were changed and SVB was leading the charge pushing for the onerous regulations to be lifted.

The bank executive lobbying in this instance, is the same Greg Becker who “sold $3.6 million of company stock under a trading plan less than two weeks before the firm disclosed extensive losses that led to its failure. The sale of 12,451 shares on Feb. 27 was the first time in more than a year that Becker had sold shares in parent company SVB Financial Group, according to regulatory filings. He filed the plan that allowed him to sell the shares on Jan. 26.” As reported by Business Standard

What happens next? The FDIC will move quickly to wind the bank up. The politics will start around the 97.5% of the deposits that are not FDIC covered. Larry Summers and Andrew Yang are out there arguing for the FDIC to cover all the banks depositors. The impact on the Silicon Valley and Start Up Scene could be ugly. The damage may easily spread to the “private markets” which generate the billions in cash that sloshed into SVB’s accounts.

What is the risk of the damage spreading? A lot will be written about the rest of the. US banking system in coming days, so let me pivot instead to the rest of the world, where Brad Setser offers a typically superb overview:

Brad Setser @Brad_Setser

The collapse of Silicon Valley Bank highlighted the risks posed by “underwater” long duration bonds — particularly when those bonds funded with short-term liabilities. Who else in the global economy holds a lot of underwater bonds? Asian insurers and policy banks … 1/

Edino vprašanje, ki se meni poraja, je: koga bi za takšen oz. te vrste zlom okrivili v SLO? Katero čarovnico bi pospravila na hladno tožilec Kozina in sodnica Lundrova?

Lp

Matjaž

Edino vprašanje, ki se meni poraja, je: koga bi za takšen oz. te vrste zlom okrivili v SLO? Katero čarovnico bi pospravila na hladno tožilec Kozina in sodnica Lundrova?

Lp

Matjaž

Všeč mi jeVšeč mi je