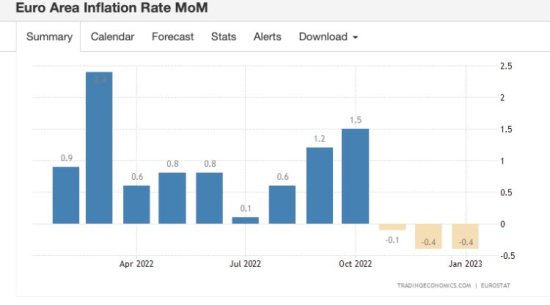

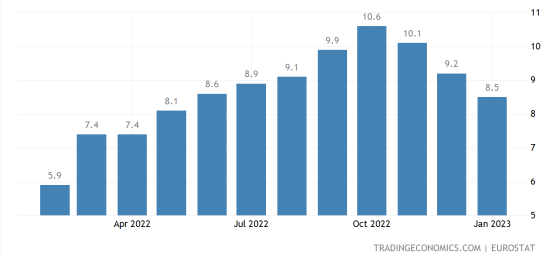

Trend upadajoče inflacije, ki ga opažamo v ZDA od julija lani naprej, se dogaja tudi v evro območju – mesečna inflacija upada že 3 mesece zapored. Glejte spodnji sliki, prva kaže mesečni prirastek, druga pa prirastek glede na isti mesec preteklega leta (letno stopnjo inflacije). Inflacijski pritiski so se močno izpeli. Še večji upad bo zabeležen v mesecih februar in marec, ko se bodo primerjale cene glede na lanska ista dva meseca, ko so cene energentov ponorele.

Slika 1: CPI inflacija v evro območju, mesečni prirastek

Slika 2: CPI inflacija v evro območju, glede na isti mesec preteklega leta

Seveda še ne moremo govoriti o zmagi nad inflacijo, saj bi kakšen nov šok spet pognal navzgor cene emergentov, ki so bile ključna postavka za lanski dvig splošne ravni cen. Ne glede na to pa se med ekonomisti in centralnimi bančniki že delajo “obračuni” glede zaslug. Torej, komu pripisati zasluge za zniževanje inflacije? Centralni bančniki in “team stagflacionistov” (oznaka Paula Krugmana) pripisuje zasluge sebi, saj naj bi “odločna akcija” Fed glede zviševanja obrestne mere poslala kredibilne signale gospodarstvu in potrošnikom, da centralna banka misli smrtno resno glede zniževanja inflacije. Tudi za ceno recesije oziroma stagflacije.

Toda če pogledamo podatke, je očitno, da inflacija ni padla zaradi bistvenega ohlajanja gospodarstva (kar je mehanizem centralnih bank prek dvigovanja obrestnih mer), pač pa predvsem zaradi padca cen energentov. Seveda je v ozadju lahko deloval posreden učinek, in sicer da so cene energentov upadale zaradi zmanjšanja povpraševanja gospodarstva po energentih (zaradi kitajske zero-Covid politik, recesijskih pričakovanj v razvitih državah in visokih cen). Kar pa delno gre na roku “teamu staflacionistov”.

Druga skupina ekonomistov, ki ji Krugman pravi “team transition”, Stiglitz pa “team transitory”, pa trdi, da je bila inflacija prehodne (tranzitorne) narave zaradi ponudbenih šokov (odpiranja gospodarstva po Covidu in nato dodatno še zaradi ukrajinske vojne). Ti ekonomisti pravijo, da je bilo drastično zviševanje obrestnih mer (glejte spodnjo sliko) nepotrebno. Da je premočno podražilo kredite (predvsem za nepremičnine), da negativno vpliva na ceno zadolževanja držav v razvoju in da bodo zaradi visoke depozitne obrestne mere pri centralni banki od tega “profitirale” samo banke (dodatnih 100 do 200 milijard dolarjev v ZDA in enako v evrih za banke v evro območju).

Jospeh Stiglitz je tipičen predstavnik te “tranzitorne” skupine, medtem ko se je Krugman iz te skupine – glede vzrokov za inflacijo, ne pa glede zdravljenja inflacije – preselil nekako do pol poti do skupine stagflacionistov. Nekaj odlomkov najprej iz Krugamanovega komentarja, ki pravi, da stagflacionisti niso imeli prav, ko so govorili, da bo za znižanje inflacije potrebno “ustvariti bolečino” (beri: recesijo in povečanje brezposelnosti):

To get meta for a bit here, one disturbing aspect of recent economic debate has been the consistency of many economists’ positions despite rapid changes in the economic situation: Optimists are always optimists, pessimists always pessimists. And I have to admit that I personally am part of this pattern.

Given the tendency to choose data that reinforces one’s prejudices, I’ve become nervous about using “artisanal” inflation measures that try to exclude data that may well be misleading. Can we trust people, myself included, not to pick the measures they like?

For a while I thought I could avoid this issue by focusing on growth in wages, a broad measure of how hot the economy is running. But this approach has problems, too. For one thing, the craziness of the post-pandemic economy has reshuffled the mix of high- and low-wage jobs, distorting the averages.

Beyond that (although possibly related), recently the Bureau of Labor Statistics has been making big revisions to past estimates — big enough to cause large changes in the narrative. Here’s the three-month change in average hourly earnings, as reported in three successive data releases:

The past is not quite what it used to be, at least when it comes to B.L.S. data.

The November release (the blue line) seemed to show a clear pattern of slowing inflation. Yay! Then, in December, the B.L.S. not only released a higher wage number but revised older numbers up so that the new trajectory (the orange line) seemed to show inflation getting worse. Aarrgh! And then, in January, it revised the numbers again — the gray line — and the inflation trajectory looked better again. Um …

So I spent this morning trying not to drink too much coffee, waiting for the release of the Employment Cost Index, which tries to correct for changes in the job mix and is probably the best measure we have of wage pressures. And it was good.

It shows overall wages and salaries rising at a 4 percent rate, only a bit higher than they were prepandemic. Diving into the details, things look a bit better, if anything. As Mike Konczal, a leading member of Team Soft Landing, put it: “The Fed has lost its excuse for a recession.”

No doubt this debate will continue, as economic debates tend to. But I think we’re approaching the point at which Team Stagflation will have to do what Team Transitory did a while back: admit that they got it wrong, and try to figure out why.

In še nekaj odlomkov iz komentarja Josepha Stiglitza, ki svari predvsem pred negativnimi učinki napačnega “zdravljenja! prehodne inflacije prek dvigovanja obrestnih mer:

irst, economists’ standard models – especially the dominant one that assumes the economy always to be in equilibrium – were effectively useless. And, second, those who confidently asserted that it would take five years of pain to wring inflation out of the system have already been refuted. Inflation has fallen dramatically, with the December 2022 seasonally adjusted consumer price index coming in just 1% above that for June.

There is overwhelming evidence that the main source of inflation was pandemic-related supply shocks and shifts in the pattern of demand, not excess aggregate demand, and certainly not any additional demand created by pandemic spending. Anyone with any faith in the market economy knew that the supply issues would be resolved eventually; but no one could possibly know when.

…

Policymakers continue to balance the risk of doing too little versus doing too much. The risks of increasing interest rates are clear: a fragile global economy could be pushed into recession, precipitating more debt crises as many heavily indebted emerging and developing economies face the triple whammy of a strong dollar, lower export revenues, and higher interest rates. This would be a travesty. After already letting people die unnecessarily by refusing to share the intellectual property for COVID-19 vaccines, the United States has knowingly adopted a policy that will likely sink the world’s most vulnerable economies. This is hardly a winning strategy for a country that has launched a new cold war with China.

Worse, it is not even clear that there is any upside to this approach. In fact, raising interest rates could do more harm than good, by making it more expensive for firms to invest in solutions to the current supply constraints. The US Federal Reserve’s monetary-policy tightening has already curtailed housing construction, even though more supply is precisely what is needed to bring down one of the biggest sources of inflation: housing costs.

…

To be sure, a deep recession would tame inflation. But why would we invite that? Fed Chair Jerome Powell and his colleagues seem to relish cheering against the economy. Meanwhile, their friends in commercial banking are making out like bandits now that the Fed is paying 4.4% interest on more than $3 trillion of bank reserve balances – yielding a tidy return of more than $130 billion per year.

To justify all this, the Fed points to the usual bogeymen: runaway inflation, a wage-price spiral, and unanchored inflation expectations. But where are these bogeymen? Not only is inflation falling, but wages are increasing more slowly than prices (meaning no spiral), and expectations remain in check. The five-year, five-year forward expectation rate is hovering just above 2% – hardly unanchored.

Some also fear that we will not return quickly enough to the 2% target inflation rate. But remember, that number was pulled out of thin air. It has no economic significance, nor is there any evidence to suggest that it would be costly to the economy if inflation were to vary between, say, 2% and 4%. On the contrary, given the need for structural changes in the economy and downward rigidities in prices, a slightly higher inflation target has much to recommend it.

Some also will say that inflation has remained tame precisely because central banks have signaled such resolve in fighting it. My dog Woofie might have drawn the same conclusion whenever he barked at planes flying over our house. He might have believed that he had scared them off, and that not barking would have increased the risk of the plane falling on him.

One would hope that modern economic analysis would dig deeper than Woofie ever did. A careful look at what is going on, and at where prices have come down, supports the structuralist view that inflation was driven mainly by supply-side disruptions and shifts in the pattern of demand. As these issues are resolved, inflation is likely to continue to come down.

Yes, it is too soon to tell precisely when inflation will be fully tamed. And no one knows what new shocks await us. But I am still putting my money on “Team Temporary.” Those arguing that inflation will be largely cured on its own (and that the process could be hastened by policies to alleviate supply constraints) still have a much stronger case than those advocating measures with obviously high and persistent costs but only dubious

You must be logged in to post a comment.