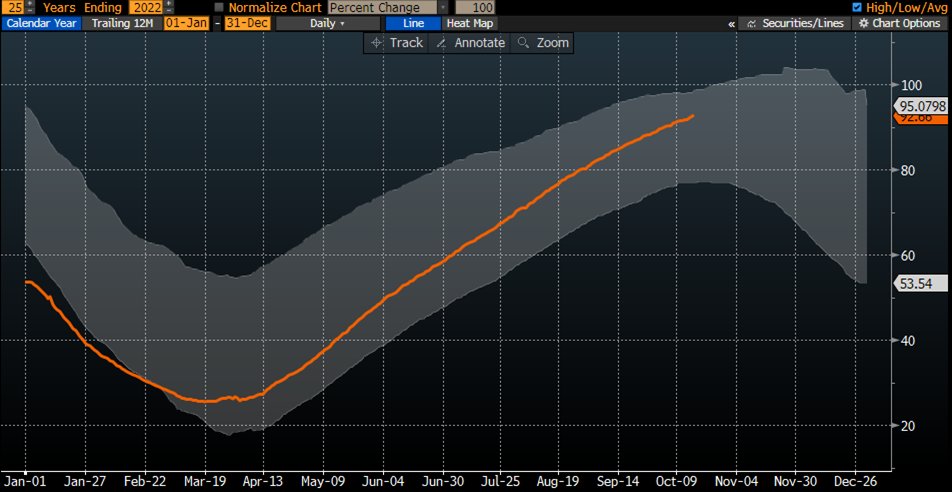

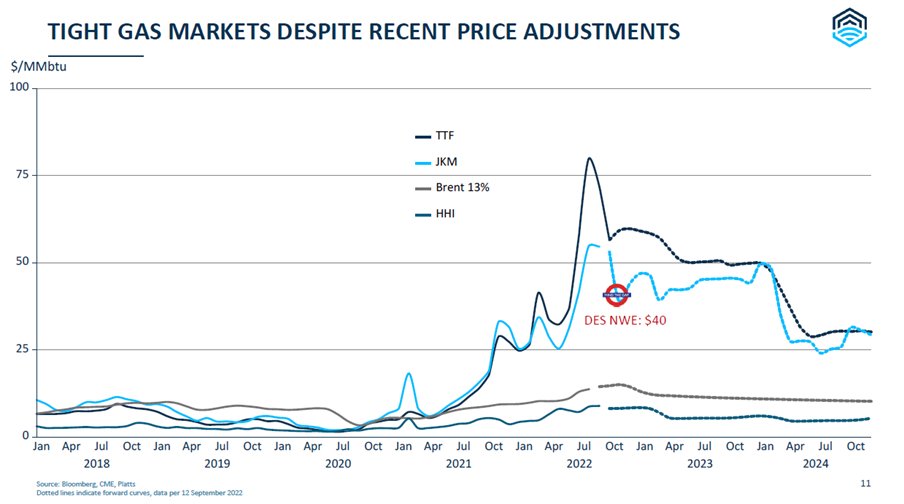

Medtem ko se “voditelji EU” pripravljajo na uvedbo cenovne “kapice” oziroma “ovratnice” za plin, so cene plina na referenčnih borzah (denimo nizozemska TTF) kolapsirale. V nekaj tednih so upadle za 80%, iz 338 €/MWh na vsega 63 €/MWh (kar je sicer 4-krat več kot pred dvema letoma). In še upadajo. Razloga sta manjše povpraševanje industrije zaradi prostovoljnega zmanjšanja proizvodnje vsled visokih cen plina (za 13%) ter zaradi drsenja v recesijo. Hkrati so evropske države že napolnile skladišča plina med 90 in 95%, kar zmanjšuje povpraševanje po plinu in zaradi česar se pred španskimi terminali za utekočinjen zemeljski plin (UZP) že delajo čakalne vrste tankerjev s plinom. Cene plina in nafte utegnejo v naslednjih dveh mesecih zaradi presežne ponudbe celo upasti na tako nizke ravni kot v času Covida. S tem postaja tudi dogovor glede cenovne kapice – ovratnice bolj ali manj irelevanten.

Spodaj je dobra nit Alexandra Stahela, ki pojasnjuje, zakaj je prišlo do kolapsa cen in ali bomo naslednje leto lahko nadomestili manjkajočih 60 mm3 plina. Letos smo lahko hvaležni prostovoljnemu zmanjšanju porabe plina zaradi visokih cen, Kitajski, ki se je odrekla delu LNG ter toplemu vremenu, toda naslednje leto mora Evropa zagotoviti dodatnih 60 mm3 plina, ki ga le letos še dobila iz Rusije.

1/n

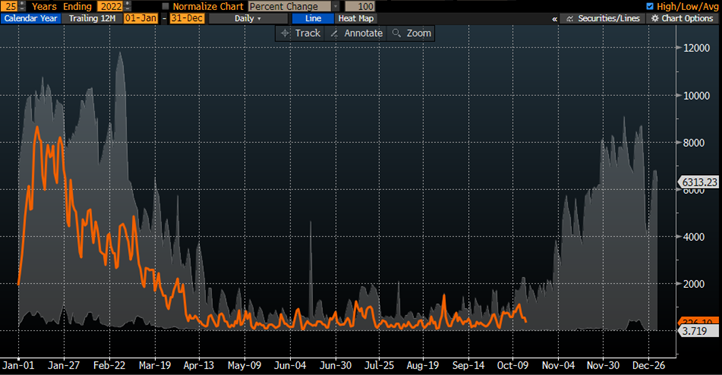

Mind you though, TTF was €13/MWh 2 years prior – up still 370%.

2/n

Because natgas can only be consumed or stored. If storage is (95%) full & not consumed (mild weather), prices have to do the work to keep system balanced as comdties trade in present (d-s), unlike equities/bonds which discount future.

3/n EU storage in %

4/n EU gas withdrawal in (GWh/day)

Europe needs to replace even more LNG in 2023 which will get much harder.

One way to verify that is by looking at the futures curve. It prices TTF at €140/MWh come Nov 2022 and into April 2024.

5/n

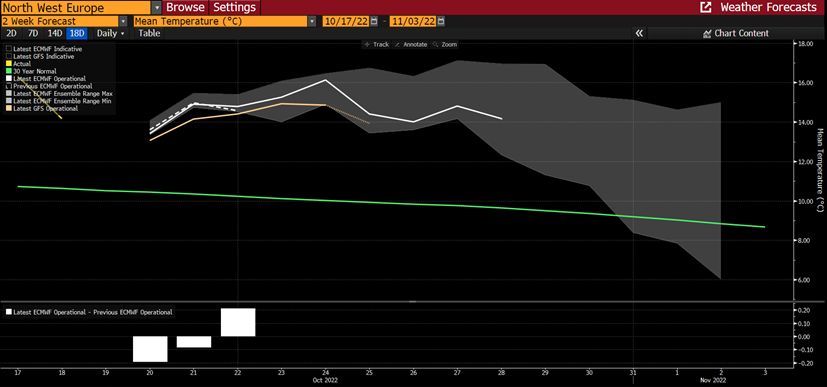

6/n 14 day weather forecast vs 30y normal

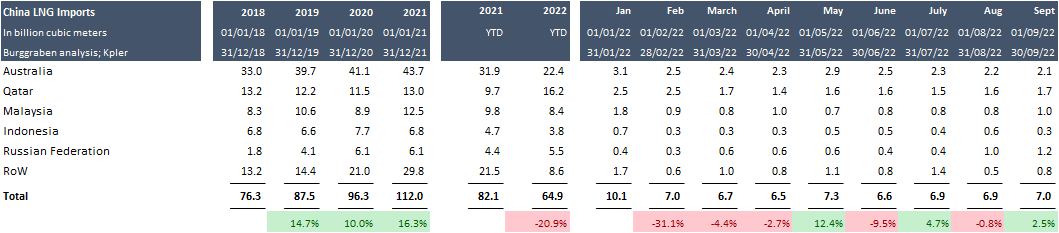

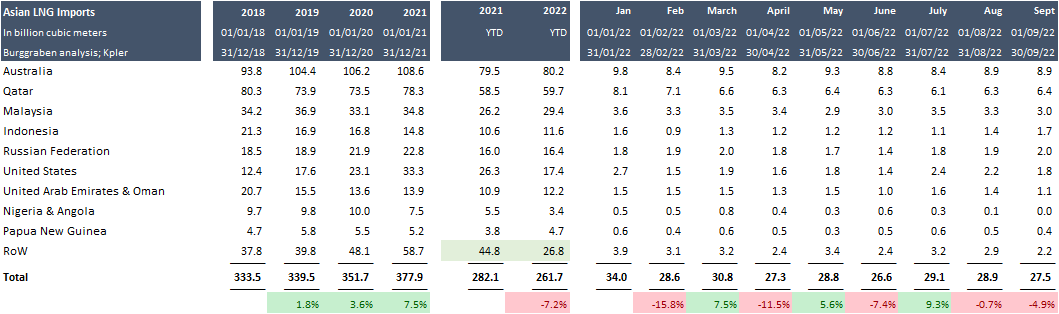

20% lower Chinese LNG purchasing yoy matters a lot too as it dragged Asian JKM prices lower into winter months as Asia obviously competes for those same LNG spot barrels with Europe (ex Australia; ex l-t Qatar contracts).

7/n

In general: US, Qatar & Australia are the big 3 exporters while EU, China, Japan & South Korea are the big importers of the global LNG market.

Of course, Middle East (UAE; Oman) & Nigeria or Angola matter too.

7/n

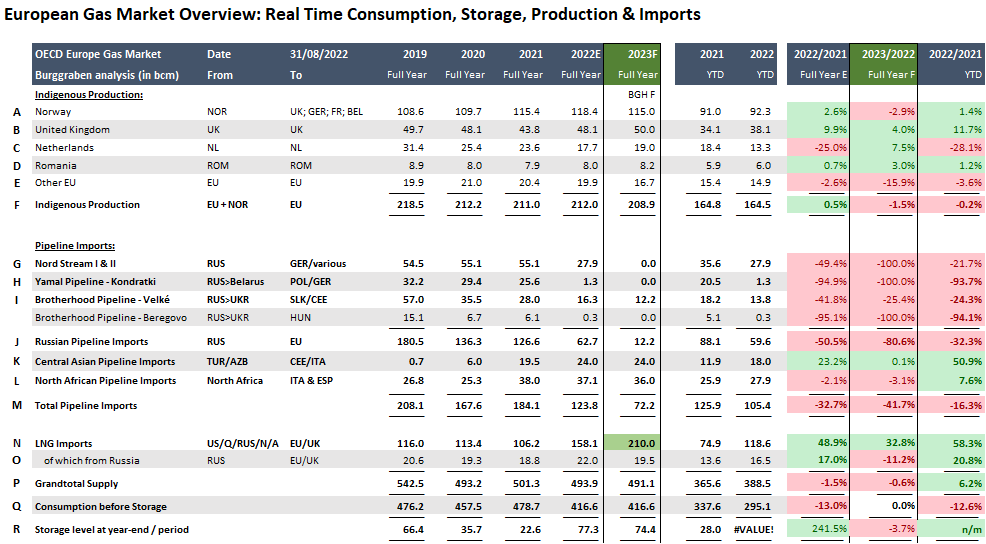

It will have to source approx 210bcm LNG, ceteris paribus.

That is 60bcm > than 2022 (which was 60bcm > than 2021).

Weather + Groningen field spare cap of 20bcm are only factors that can change this forecast meaningfully.

8/n

If they will re-engage (which we suspect) & continue LNG growth path to replace some coal use, prices (not politicans god forbid!) will have to do the work – like now – to clear market!

9/n

That is because US contracts have destination flexibility = means cargos owner were able to sell on the way to its original destination (say Japan) into Europe to make instant profit – nice!

10/

US operators have incentive (lower HH prices; arbitrage) to increase such capacities. But infra expansion takes time. 2025/26 is the time for more exports.

It adds 6bcm incremental supply for Europe in 2023. We are looking for 60bcm!

12/n

They usually purchased LNG pre-2020 on a long-term contract paid $6-10/MMBtu. Such LNG could be sold for >$30 all year, at times at $75 in spot market.

13/n

Re-directing Qatar cargos requires (Asian) buyers to return it to Qataries at par (<$10/MMBtu). Why would they?

Real challenge however will be to pull enough LNG into Europe come 2023.

For that prices must do THE WORK.

15/n Thx

Vir: Alexander Stahel, twitter