Za nami je težko pričakovana tradicionalna elitna konferenca centralnih bankirjev v “najbolj čudnem mestu na svetu”. Jackson Hole je zanimiv z dveh vidikov: zaradi konference z zanimivo elitno zasedbo (centralni bankirji, elitni ekonomisti in skrbno izbrani novinarji) in zaradi kontrasta samega mesteca, ki ga “krasi” največja polarizacija glede dohodkov v ZDA (neenakost). Adam Tooze je naredil zanimiv vpogled v zgodovino te konference in samega mesteca (spodaj je nekaj odstavkov).

No, letošnja konferenca je bila tako močno pričakovana, ker so predvsem igralci na finančnih trgih želeli slišati, ali bo Fed v luči recesije v ZDA prenehal s politiko zviševanja obrestne mere. Toda šef Feda Jerome Powell je na tokratno konferenci “igral Paula Volckerja”, ki je pred natanko 40 leti branil svojo politiko dvigovanja obrestne mere, da bi znižal inflacijo. Powell je naredil enako in povedal, da je zniževanje inflacije prioriteta Feda in da bodo gospodarstvo in prebivalstvo pač deležni bolečine, ko bo dvig obrestnih mer pobil investicije in gospodarstvo poslal v recesijo ter povečal brezposelnost.

Toda tokrat je bila razprava precej bolj civilizirana kot pred 40 leti. Takrat je skupina ekonomistov ostro napadla Volckerjevo politiko, nobelovec James Tobin je bil na sami konferenci zelo jasen, da bo ta politika povzročila recesijo in dolgotrajno povečano brezposelnost in da bi morali Fedu zmanjšati pristojnosti, saj glede njegovih ukrepov ni nobene demokratične kontrole. Teden dni kasneje je Tobin v Washington Postu objavil zelo decidirano kritko Volckerjeve dezinflacijske politike “Stop Volcker from Killing the Economy”. Volckerja se kritika ni prijela in je nadaljeval z ostro dezinflacijsko politiko, inflacijo je sicer znižal iz 10% na 5% (na tej ravni je vztrajala celo desetletje), toda stopnja brezposelnosti se je šele po osmih letih vrnila na raven iz leta 1979, ko je začel z dezinflacijsko politiko. Tudi tokrat bo žrtev najbrž dokaj podobna.

Medtem ko so bili na letošnji konferenci udeleženci bistveno manj kritični in predvsem uglajeni, pa sta Powell in Fed požela precej več kritike s strani strokovne javnosti v medijih. Kritike se nanašajo predvsem na napake Feda pri napovedovanju inflacije lani, pri zamujanju z ukrepi in na izgubljeno kredibilnost (slednje je ključna lastnost v monetarni makroekonomiji, saj naj bi bilo od kredibilnsti centralne banke odvisno ali ji bodo subjekti verjeli in ustrezno spremenili obnašanje).

As is often the case, the smartest critical take on Powell’s dilemmas came from Mohamed El-Erian. Strikingly, El-Erian too framed his analysis in terms of temporality, in his case in terms of the past, present and the future. El-Erian was pleased with Powell’s message that rates will continue to rise and will do so for some time to come. But he regretted Powell’s failure to come to terms with the past and to more clearly map the future.

In El-Erian’s view, Powell has a fivefold problem.

(1) Powell’s 2021 speech premised on low inflation gave hostages to fortune and, with hindsight, was in El-Erian’s view a refletion of a fourfold failure of “bad forecasts, poor communication and belated policy responses”.

(2) In 2021, the Fed missed the chance for a soft-landing (by acting earlier) and now needs to show a determination to act since otherwise it will become a “mistake that builds on itself, aggravating problems of low growth, high inflation, worsening inequality and future financial instability”.

(3) The Fed’s forecasts and guidance have lost credibility. “Its quarterly (inflation) forecasts have been repeatedly dismissed as fantasy and its communication is seen as lacking the consistency needed for effective policy guidance.” This matters, according to El-Erian because it means the Fed will have a harder time persuading markets to believe its tougher stance.

(4) The Fed needs to address the fact that the “new policy framework” it first began developing in 2020 to deal with a world of low inflation, looks out of step with reality.

(5) Powell needs to “take responsibility for the last 18 months of Fed errors, including the mis-characterisation of economic and policy issues in last year’s speech”.

In El-Erian’s judgement, Powell’s unusually short 2022 speech: “dealt well with the present, but left out important past and future issues. I suspect that we will look back on this year’s Jackson Hole speech as a missed opportunity for the Fed to regain control over its policy narrative, as well as to outline what is needed to overcome the considerable policy challenge facing the world’s most powerful and systemically important central bank.”

This is perhaps the most substantive and extensive articulation of the critical position. It will be interesting to see how the Fed moves forward from this moment.

Not everyone agrees with El-Erian’s scathing critique. As Karl W. Smith notes at Bloomberg, the Fed has in fact pivoted to a far tougher line since March. Part of the problem is that after an initial selloff, markets have been slow to get the message. Over the summer the rebound helped to ease credit conditions at least somewhat.

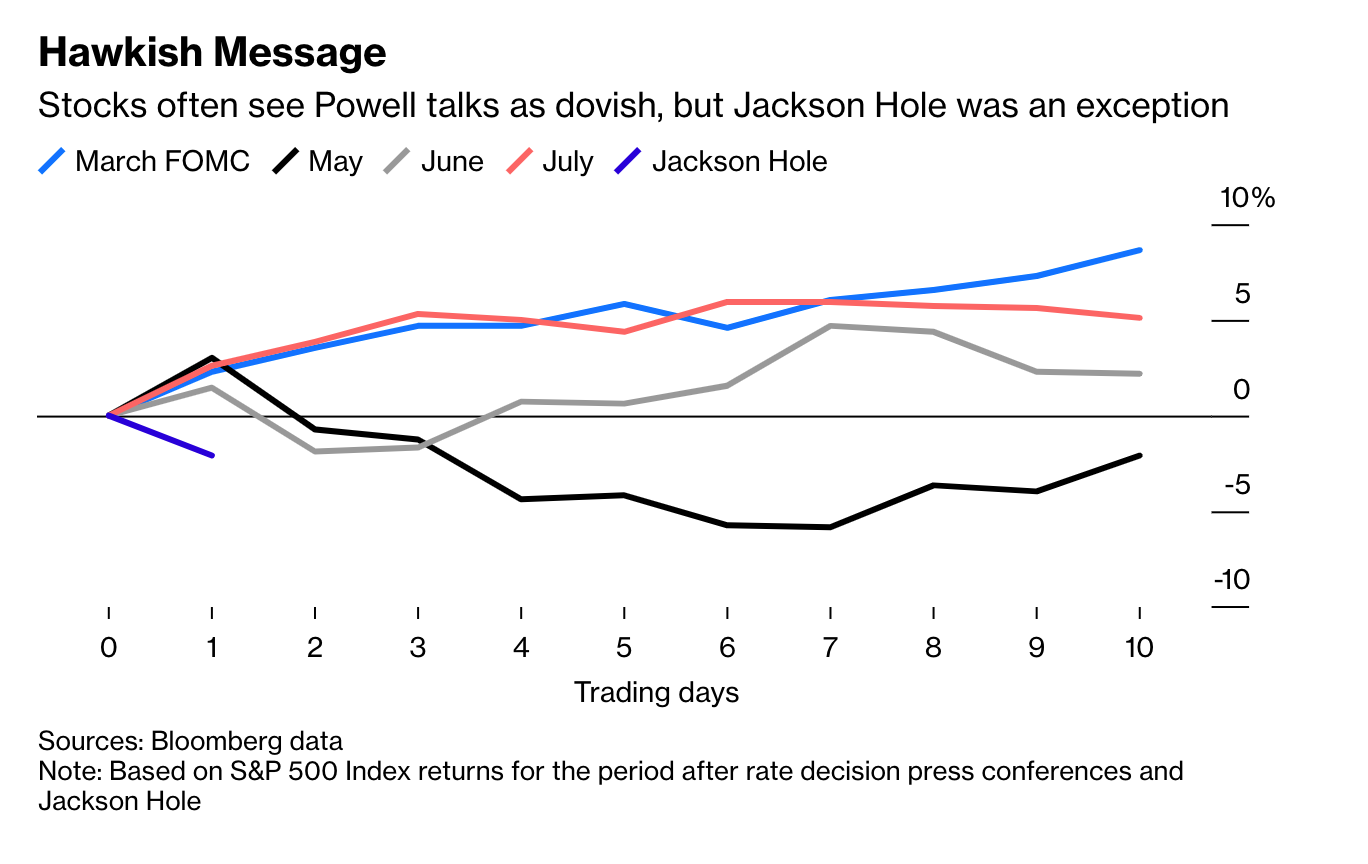

On this occasion the markets seem to have taken the point.. Rather than rallying as they have done after Powell’s more upbeat press conferences, the reaction to his toughly worded speech at Jackson Hole was a significant sell off.

Meanwhile, Raghuram Rajan, formerly the governor of India’s central bank, is kinder to Powell.

Clearly the Fed’s shift in August 2021 to a more accommodating framework of average inflation targeting was ill-timed.

This was the right framework for an era of structurally low demand and weak inflation, but exactly the wrong one to espouse just as inflation was about to take off and every price increase fuelled another. But who knew the times were a-changing? Even with perfect foresight — and in reality they are no better informed than capable market players — central bankers may still have been behind the curve. This is understandable. A central bank cools inflation by slowing economic growth. No matter how independent it is, its policies have to be seen as reasonable, or else it loses its independence. With governments having spent trillions to support their economies, employment just recovered from terrible lows and inflation barely noticeable for over a decade, only a foolhardy central banker would have raised rates to disrupt growth if the public did not yet see inflation as a danger. Put differently, pre-emptive rate rises that slowed growth would have lacked public legitimacy — especially if they were successful and inflation did not rise subsequently. Central banks needed the public to see higher inflation to be able to take strong measures against it.

The real question is what happens next.

This is not a time for postmortems to assess central bank functioning.

Instead central banks in Rajan’s view should concentrate on inflation fighting and they should do so without fear of deflation.

Of course, when central banks succeed in bringing inflation down, we will probably return to a low-growth world. It is hard to see what would offset the headwinds of ageing populations, a slowing China and a suspicious, militarising, deglobalising world. … What if inflation is too low? Perhaps like the virus, we should learn to live with it.

Rajan’s worry is that if they go beyond this limited but cruciual mandate, they risk a larger cycle of exaggerated expectations, disillusionment and delegitimization.

As central bankers meet in Jackson Hole, they must wonder how far they have fallen in the public’s eyes. A short while ago, they were heroes, supporting feeble growth with unconventional monetary policies, promoting the hiring of minorities by allowing the labour market to run a little hot, and even trying to hold back climate change, all the while berating paralysed legislatures to do more. Now they stand accused of flubbing their most important task, keeping inflation low and stable. Politicians, sniffing blood and mistrustful of the power of unelected officials, want to re-examine central bank mandates.

It is a dramatic scenario, of which Rajan has some experience in the Indian context. And no one should underestimate the threats to the institutional fabric in America today. But here too one must surely ask, when the talk turns to “sniffing blood”, are we talking about reality, or are we enacting a pantomime political economy?

Vir: Adam Tooze

Zakaj je FED ravnal kot je ravna?l:

“Talk is cheap”

Problem s tem je, da na dolgi rok pada kredibilnost. Je pa tudi res, kar je rekel že Keynes:

“Na dolgi rok smo vsi mrtvi”

In nikar ne pozabiti na Draghi-ja (parafraziram);

“Če ne gre drugače, se pač zlažež”

Raja ima itak omejen spomin.

Všeč mi jeVšeč mi je