V ZDA je inflacija v preteklih dveh mesecih po sprejemu Bidenovega stimulus programa pospešila. To je seveda dalo vetra v jadra inflacijskim jastrebom, ki napovedujejo hiperinflacijo že zadnjih 11 let, odkar je FED začel s prvim paketom kvantitativnega sproščanja. Tudi sicer zmerni Larry Summers, ki je od začetka trdil, da je Bidenov stimulus preobsežen in da bo povzročil pregrevanje gospodarstva, je dva dni nazaj razlagal, da je inflacijski pospešek celo večji od njegovih pričakovanj. Zdi se, da so finančni trgi višjo prihodnjo inflacijo vzeli v zakup. Vendar, je ta inflacijska nevarnost res realna?

Poglejmo nekaj argumentov. Prva stvar, ki jo glede inflacije moramo razumeti, je, da pri “tiskanju denarja” s strani centralne banke ne gre za dejansko povečevanje denarja v obtoku (denimo za dodatne količine bankovcev ali elektronskega denarja). Pri centralnobančnem “tiskanju denarja” gre dejansko zgolj za zagotavljanje dodatne likvidnosti poslovnim bankam s t.i. primarnim denarjem. Slednji služi poslovnim bankam za uravnavanje medsebojne likvidnosti. Količina denarja v obtoku se poveča šele, ko poslovne banke odobrijo nove kredite potrošnikom ali podjetjem (pri tem pa v ta namen kot depozite ali za izravnavanje pozicij uporabijo primarni denar centralnih bank). Če ni novih kreditov s strani poslovnih bank, ni dodatnega denarja v obtoku in ne more priti do inflacije. Denar ustvarja povpraševanje po njem. Problem v Evropi oziroma v evrskem obdobju v zadnjem desetletju je bil, da se vsa ta povečana likvidnost, ki jo je ECB napumpala v evrski bančni sistem, ni prelila v povečane kredite potrošnikom in podjetjem, pač pa je ostala v obliki depozitov poslovnih bank pri ECB.

Druga ključna stvar pa je, da se povečanje denarja v obtoku, ki ga denimo merimo z agregatom M2 (gotovina in depoziti), ne prelije avtomatično tudi v povečano inflacijo, kot si to predstavlja večina laične javnosti ter velik del ekonomistov. Na čelu z Miltonom Friedmanom, ki je propagiral kvantitativno teorijo denarja (PxQ=TxV). Paul Krugman to napačno predstavo ironično imenuje “teorija brezmadežne inflacije“. Vendar je inflacija, kadar do nje ne pride zaradi eksogenega šoka, posledica gospodarske rasti. Torej posledica povečanega števila transakcij zaradi večje gospodarske aktivnosti in povečanega povpraševanja po delovni sili, ki zaradi njenega pomanjkanja (trk ob naravno stopnjo brezposelnosti) privede do pospešene rasti plač. Spodaj je zelo nazorna razlaga Paula Krugmana, ki bi morala biti vsem razumljiva.

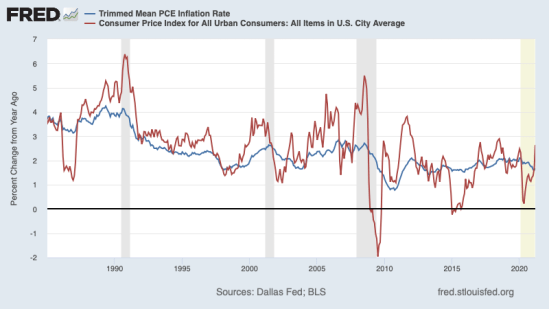

No, ali smo glede na povedano danes v situaciji, ko lahko pričakujemo povišano inflacijo v ZDA? Pogoji zanjo so sicer izpolnjeni: (1) banke so polne likvidnosti, ki jo je FED dodatno napumpal v gospodarstvo po začetku epidemije, in (2) Bidenov stimulus paket (1,900 milijard dolarjev) in njegov infrastrukturni paket (2,300 milijard dolarjev) sta tako velika, da lahko spodbudita visoko gospodarsko rast in pospešita rast plač zaradi omejenosti ponudbe delovne sile. Toda ali se bo to res zgodilo? Trenutno gledamo sicer pospešek v indeksu cen življenjskih dobrin, ne pa tudi v temeljni inflaciji (brez cen energetov, hrane, alkohola in tobaka), ki se v ZDA v zadnjem desetletju giblje med 1.7 in 2% na letni ravni. V letošnjem letu je temeljna inflacija celo upadla glede na zadnji dve leti.

In to navkljub povečani količini denarja (M2). Ne pozabite, da so v slednjem agregatu zajeti kratkoročni depoziti gospodinjstev in podjetij, ki v času povečane negotovosti kopičijo likvidnost v obliki depozitov na bankah.

Težko je biti prerok, toda v dani situaciji je najbolj verjetno, da bo letos v ZDA res prišlo do višje ravni indeksa cen življenjskih potrebščin, temu pa ne bo nujno sledila temeljna inflacija. Pri tem pa velja upoštevati novo doktrino FED, ki je bila razvita v mandatu sedanjega predsednika Jeroma Powella, in sicer, da bo FED dopuščal srednjeročno višjo raven inflacije (nad inflacijskim ciljem 2%), da bi tako trajno stimuliral višja inflacijska pričakovanja. S čimer bi se izognil zadregam iz zadnjega desetletja, ko FEDu nikakor ni uspevalo trajneje dosegati inflacijskega cilja. Torej kratkotročno lahko sledi obdobje nekoliko povišane inflacije (indeksa cen življenjskih potrebščin) zaradi pregrevanja ameriškega gospodarstva v času Bidenovega stimulusa, pri čemer FED ne bo nujno reagiral z dvigovanjem obrestne mere, medtem ko je trajnejši dvig temeljne inflacije manj verjeten.

Spodaj je še Krugmanova razlaga inflacije, velja si jo prebrati.

For one thing, we are seeing some actual inflation as a recovering economy runs into bottlenecks — shortages of lumber, shipping containers, used cars, etc. I believe, and the Fed believes, that these shortages are temporary, that this is only a blip and that inflation will subside; but we could be wrong, and at least there’s some substance to this concern.

But a lot of the money-printing panic is, I believe, coming from the crypto crowd. I’ve been in a number of extended (and determinedly civil) discussions with boosters of Bitcoin etc., doing my best to keep an open mind. What happens in these discussions is that skeptics like me keep pressing for an answer to the question, “What problem is cryptocurrency supposed to solve, exactly?” And at some point the answer always devolves to some version of “Fiat money is doomed because the Fed won’t stop running the printing press.”

So it seems to me that it would be useful to talk about why that’s a really bad take, and has been a bad take over and over again for the past 40 years.

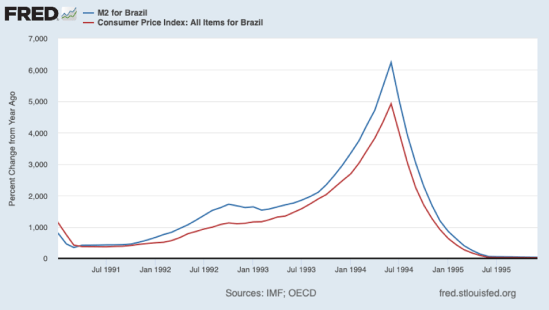

To be fair, printing huge amounts of money to pay the government’s bills does in fact lead to high inflation. Take the example of Brazil in the early 1990s:

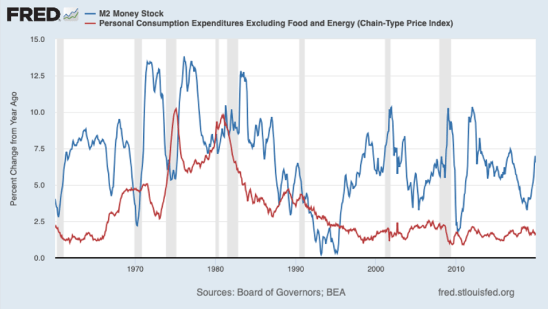

But nothing like that has happened in the U.S., even during periods when monetary aggregates like M2 have increased dramatically. Anyone claiming that big increases in M2 presage surging inflation was wrong again and again since the 1980s. I mean really, really wrong:

Why?

There are actually two big fallacies in the “printing press goes brrr -> inflation” story.

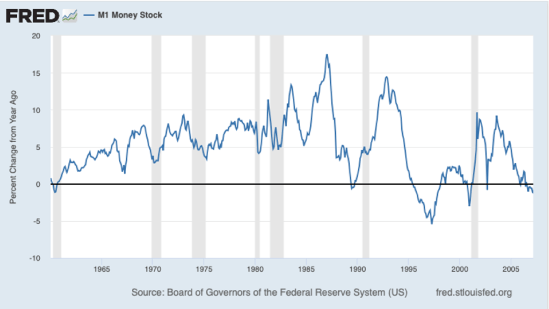

One of them is what I think of as the doctrine of immaculate inflation: the notion that an increase in the money supply somehow translates directly into inflation without causing economic overheating along the way. Many people have fallen for that fallacy over the years. Among them was no less a figure than Milton Friedman. He looked at rapid growth in M1 during the early 1980s:

And from 1982 to 1985 he repeatedly predicted a resurgence of inflation: 8 percent for 1983, double-digit for 1984, 8 to 10 percent for 1985.

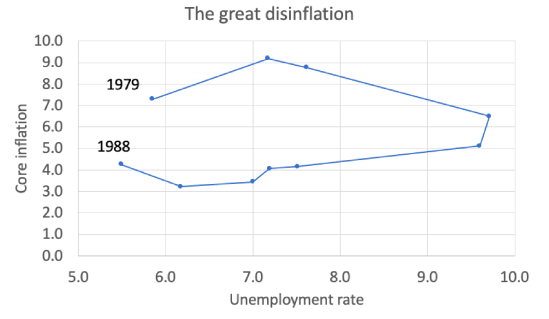

Obviously none of that happened. Instead, a slack economy with high unemployment led to declining inflation over the whole period:

Today’s inflationistas, however, don’t know anything about that history.

The other fallacy of the modern inflationistas is that they don’t understand how the role of money changes in a world of very low interest rates, even though we’ve been living in that kind of world for a very long time.

Before 2007 it was expensive for people to hold money, because cash yielded no interest while bank deposits paid less than other assets like Treasury bills. So people held money only because of its liquidity — the fact that it could readily be spent. When the Fed increased the money supply, this left the public with more liquidity than it wanted, so that the money would be used to buy other assets, driving interest rates down and leading to higher overall spending.

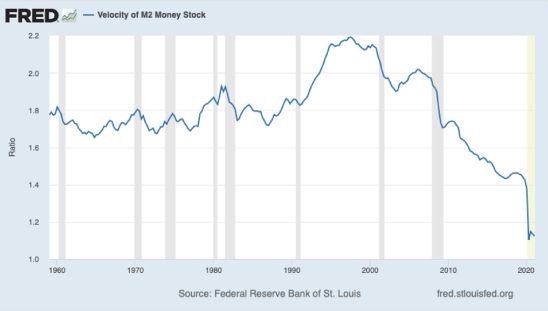

But when interest rates are very low — which they have been for years, basically because there’s a glut of savings relative to perceived investment opportunities — money is, at the margin, just another asset. When the Fed increases the money supply, people don’t feel any urgent need to put that cash to more lucrative uses, they just sit on it. The money supply goes up, but G.D.P. doesn’t, so the “velocity” of money — the ratio of G.D.P. to the money supply — plunges:

These aren’t new insights. I wrote about all of this in the context of Japan back in the 1990s, and even that was mainly a formalization of insights many economists had held for decades. And while it took a while, my sense is that by 2014 or so the great majority of economic commentators had accepted that looking at the money supply in the U.S. context offered basically no information about future inflation.

But now we have a new crop of financial types, especially, as I said, people associated with crypto, who don’t know about any of that and, as so often happens with money people, assume that they already know everything. So we’re having a fresh infestation of monetary cockroaches, and everything has to be explained again.

Vir: Paul Krugman, New York Times

You must be logged in to post a comment.