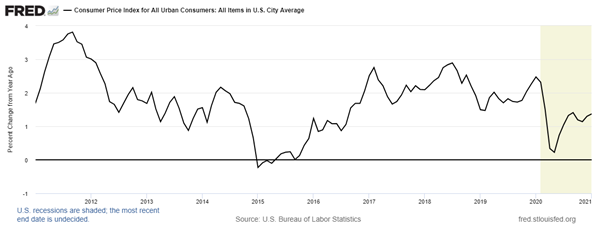

During the year of the COVID, global consumer and producer prices inflation dropped. In some manufacturing-based economies, there was even a fall in price levels (deflation) eg the Euro area, Japan and China).

US inflation rate (annual %)

“Effective demand” as Keynesians like to call it, plummeted, with business investment and household consumption dropping sharply. Savings rates rose to high levels (both corporate savings relative to investment and household savings).

Household savings rates (% of income) – OECD

| Country | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 |

| United Kingdom | 3.1 | 3.6 | 4.9 | 2.2 | 0.0 | 6.1 | 6.5 | 19.4 |

| United States | 6.6 | 7.6 | 7.9 | 7.0 | 7.2 | 7.8 | 7.5 | 16.1 |

| Euro area (16 countries) | 5.6 | 5.7 | 5.7 | 5.7 | 5.6 | 6.4 | 6.7 | 14.3 |

Many companies went bust and many lower income households either lost their jobs or faced reductions in wages. Higher income households maintained their wage levels, but they were unable to travel…

View original post 2,458 more words