Če je – kot je zatrjeval Milton Friedman – inflacija vedno in izključno monetarni fenomen (ker centralna banka “tiska” preveč ali premalo denarja, potem je monetarnim politikam enostavno zmanjkalo receptov, kako inflacijo ustvariti. V okviru ameriškega Feda so – v luči (pre)nizke inflacije in prenizkih inflacijskih pričakovanj – dve leti potekale diskusije glede potrebnega novega okvirja monetarne politike. Se pravi glede sprememb monetarnih politik, s katerimi bi bolj uspešno približali raven inflacije nazaj na željeno ciljno raven (2%). Na koncu so sprejeli nov okvir z dvema ključnima spremembama: (1) po potrebi dvig srednjeročne inflacije nad 2% za nedoločen čas in (2) da monetarna politika ne sledi več tesno trendu stopnje brezposelnosti.

Sedanji predsednik Jerome Powell je dobil težko nalogo, da javnosti pojasni, zakaj si bo Fed zavzemal inflacijo dvigniti nad 2% in jo tam tudi pustiti dlje časa in zakaj se Fed ne boji več, da bi zgodovinsko nizka brezposelnost spodbudila plačno in cenovno inflacijsko spiralo. V četrtek je na tradicionalnem srečanju centralnih bankirjev in monetarnih ekonomistov v Jackson Holeu, ki je vsako leto zadnji teden avgusta (tokrat prvič v online obliki) Powell v svojem govoru de facto razglasil dvoje:

prvič, Fed odstopa od neomonetaristične (čikaške) teorije inflacije, katere začetnik je Milton Friedman, in

drugič, da je tudi neomonetaristična – keynesianska razlaga inflacije, grafično predstavljena v obliki Phillipsove krivuje, mrtva. (za osvežitev: keynesianci so trdili da obstaja trade-off med stopnjo brezposelnosti in inflacijo, neomonetaristi pa, da obstaja morda zgolj kratkoročni trade-off med njima, medtem ko je dolgoročna Phillipsova krivulja navpična na ravni “naravne stopnje brezposelnosti“, in zato brezposelnosti z ukrepi monetarne politike ni mogoče zmanjšati pod njo, saj se dvignejo inflacijska pričakovanja)

V glavnem, de facto je povedal, da nobena izmed obstoječih teorij glede inflacije ne drži v sedanjem času in da bo Fed v času kritičnega trendnega zniževanja inflacije poskušal z novim okvirjem monetarnih politik dvigniti inflacijo in inflacijska pričakovanja na željeno raven.

Powellov govor je poslastica (spodaj sem dodatno označil nekaj odstavkov). Tudi zato, ker na dokaj preprost in tudi laični javnosti razumljiv način pove, zakaj Fed zapušča dosedanji monetarni okvir, ki je veljal dobrih 30 let in ker pove, da v bodoče Fed ne bo zasledoval več nobenih trdnih relacij, kaj šele formul. Pač pa bo z veliko dozo fleksibilnosti pri odločanju (s širokim prostorom diskrecijske pravice) presojal od situacije do situacije, kdaj je morda inflacijska stopnja postala previsoka in kdaj bi močno zmanjšana stopnja brezposlenosti morda lahko sprožila plačno spiralo navzgor. Se pravi:

Cenovni cilj: po daljšem obdobju permanentno nižje inflacije od ciljne (2%) bo Fed za daljše obdobje pustil inflacijo nad 2%, da bi ciljal na povprečno 2% inflacijo na daljši rok. Pri tem se ne bo posluževal nobenih časovnih omejitev glede dolžine obdobja višje inflacije ali se pustil diktirati od formul, pač pa zgolj zasledoval cilj 2% dolgoročne povprečne inflacije.

Cilj polne zaposlenosti: “naravna stopnja brezposlenosti” je mrtva, nihče ne ve, kakšna je prava raven polne zaposlenosti, zato bo Fed fleksibilen pri odločanju, v kateri situaciji na trgu dela bo začel zategovati monetarno politiko, da bi preprečil, da se rastoče plače prelijejo v inflacijsko spiralo (uvedel je subtilno razliko med “primanjkljajem zaposlenosti” (shortfall) in “odstopanjem” (deviation) od polne zaposlenosti).

Nov monetarni okvir bo torej: popolna nevezanost na katerikoli teoretski okvir, popolna relaksacija kratkoročnih benchmark ciljev, popolna fleksibilnost in popolna diskrecija glede odločanja.

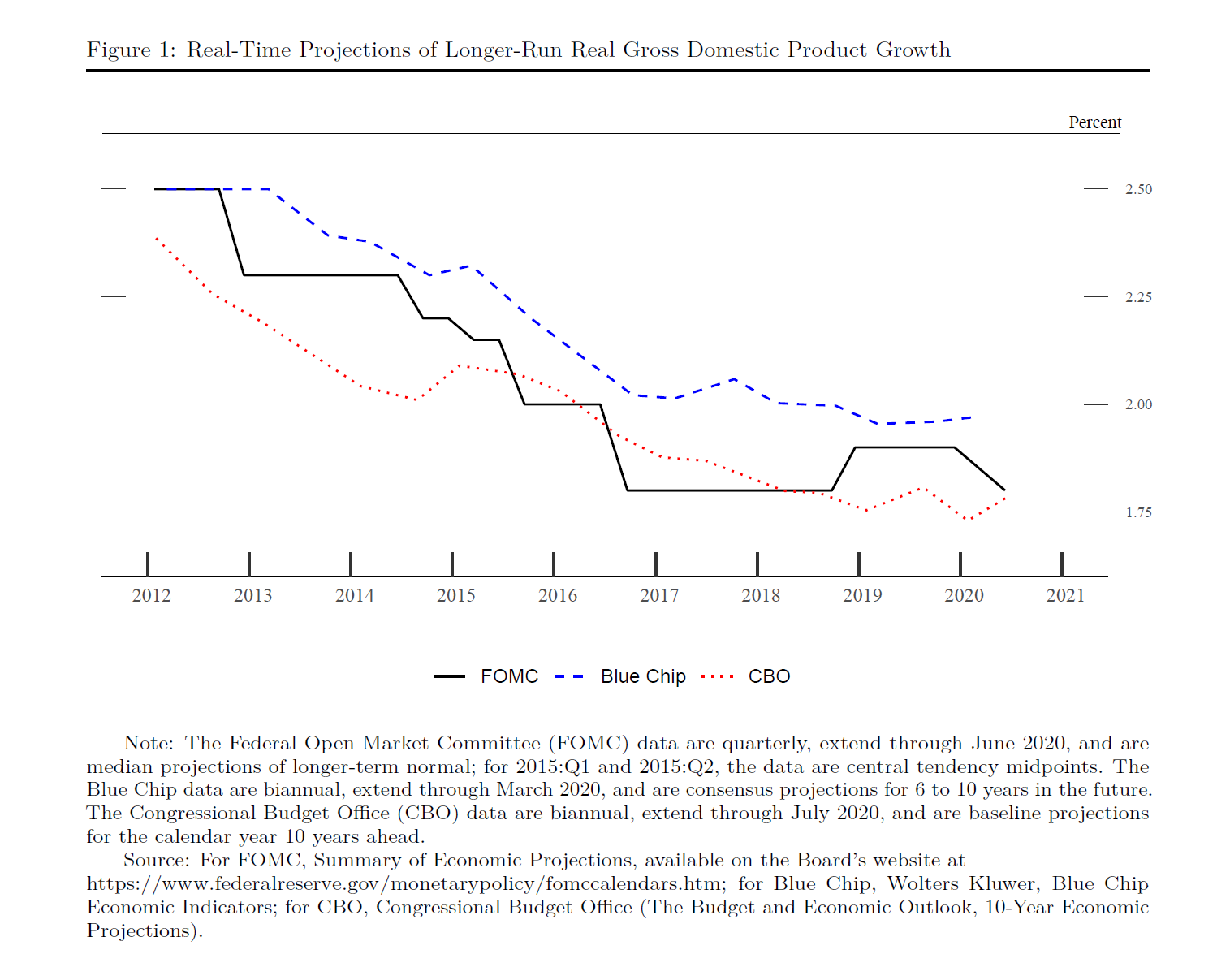

Our evolving understanding of four key economic developments motivated our review. First, assessments of the potential, or longer-run, growth rate of the economy have declined. For example, since January 2012, the median estimate of potential growth from FOMC participants has fallen from 2.5 percent to 1.8 percent (see figure 1). Some slowing in growth relative to earlier decades was to be expected, reflecting slowing population growth and the aging of the population. More troubling has been the decline in productivity growth, which is the primary driver of improving living standards over time.10

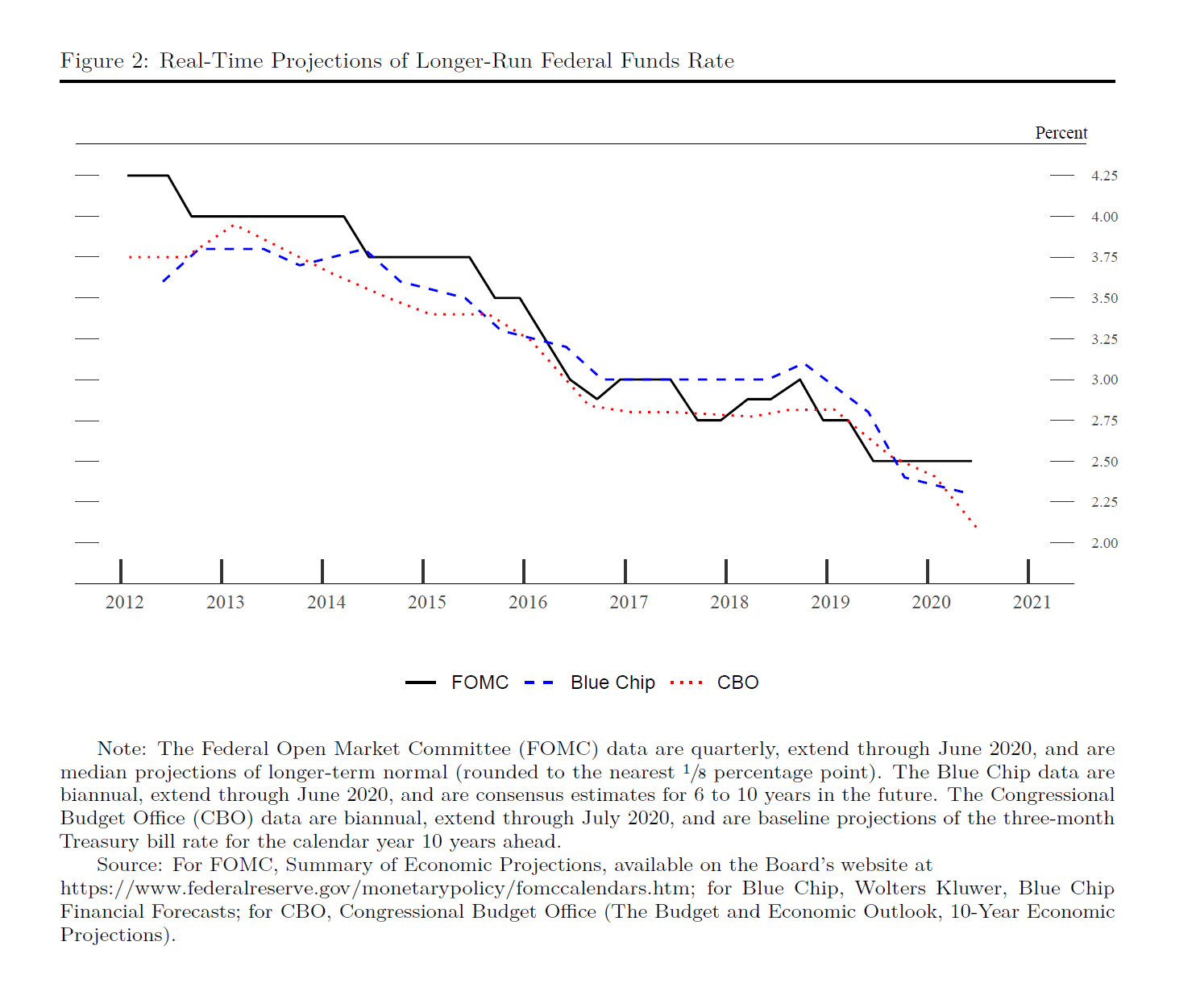

Second, the general level of interest rates has fallen both here in the United States and around the world. Estimates of the neutral federal funds rate, which is the rate consistent with the economy operating at full strength and with stable inflation, have fallen substantially, in large part reflecting a fall in the equilibrium real interest rate, or “r-star.” This rate is not affected by monetary policy but instead is driven by fundamental factors in the economy, including demographics and productivity growth—the same factors that drive potential economic growth.11 The median estimate from FOMC participants of the neutral federal funds rate has fallen by nearly half since early 2012, from 4.25 percent to 2.5 percent (see figure 2).

This decline in assessments of the neutral federal funds rate has profound implications for monetary policy. With interest rates generally running closer to their effective lower bound even in good times, the Fed has less scope to support the economy during an economic downturn by simply cutting the federal funds rate.12 The result can be worse economic outcomes in terms of both employment and price stability, with the costs of such outcomes likely falling hardest on those least able to bear them.

Third, and on a happier note, the record-long expansion that ended earlier this year led to the best labor market we had seen in some time. The unemployment rate hovered near 50-year lows for roughly 2 years, well below most estimates of its sustainable level. And the unemployment rate captures only part of the story. Having declined significantly in the five years following the crisis, the labor force participation rate flattened out and began rising even though the aging of the population suggested that it should keep falling.13 For individuals in their prime working years, the participation rate fully retraced its post-crisis decline, defying earlier assessments that the Global Financial Crisis might cause permanent structural damage to the labor market.

Moreover, as the long expansion continued, the gains began to be shared more widely across society. The Black and Hispanic unemployment rates reached record lows, and the differentials between these rates and the white unemployment rate narrowed to their lowest levels on record.14 As we heard repeatedly in our Fed Listens events, the robust job market was delivering life-changing gains for many individuals, families, and communities, particularly at the lower end of the income spectrum.15 In addition, many who had been left behind for too long were finding jobs, benefiting their families and communities, and increasing the productive capacity of our economy. Before the pandemic, there was every reason to expect that these gains would continue. It is hard to overstate the benefits of sustaining a strong labor market, a key national goal that will require a range of policies in addition to supportive monetary policy.

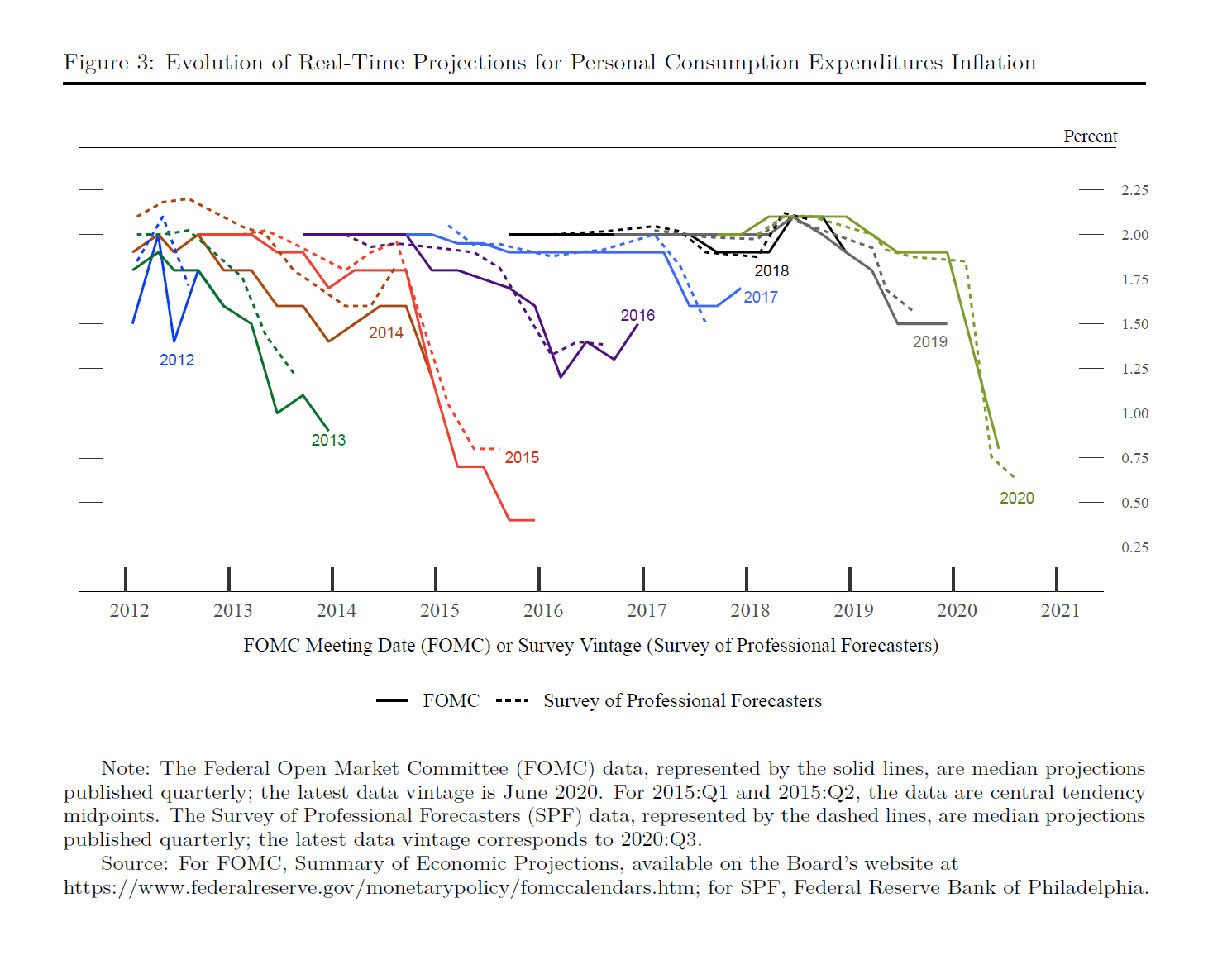

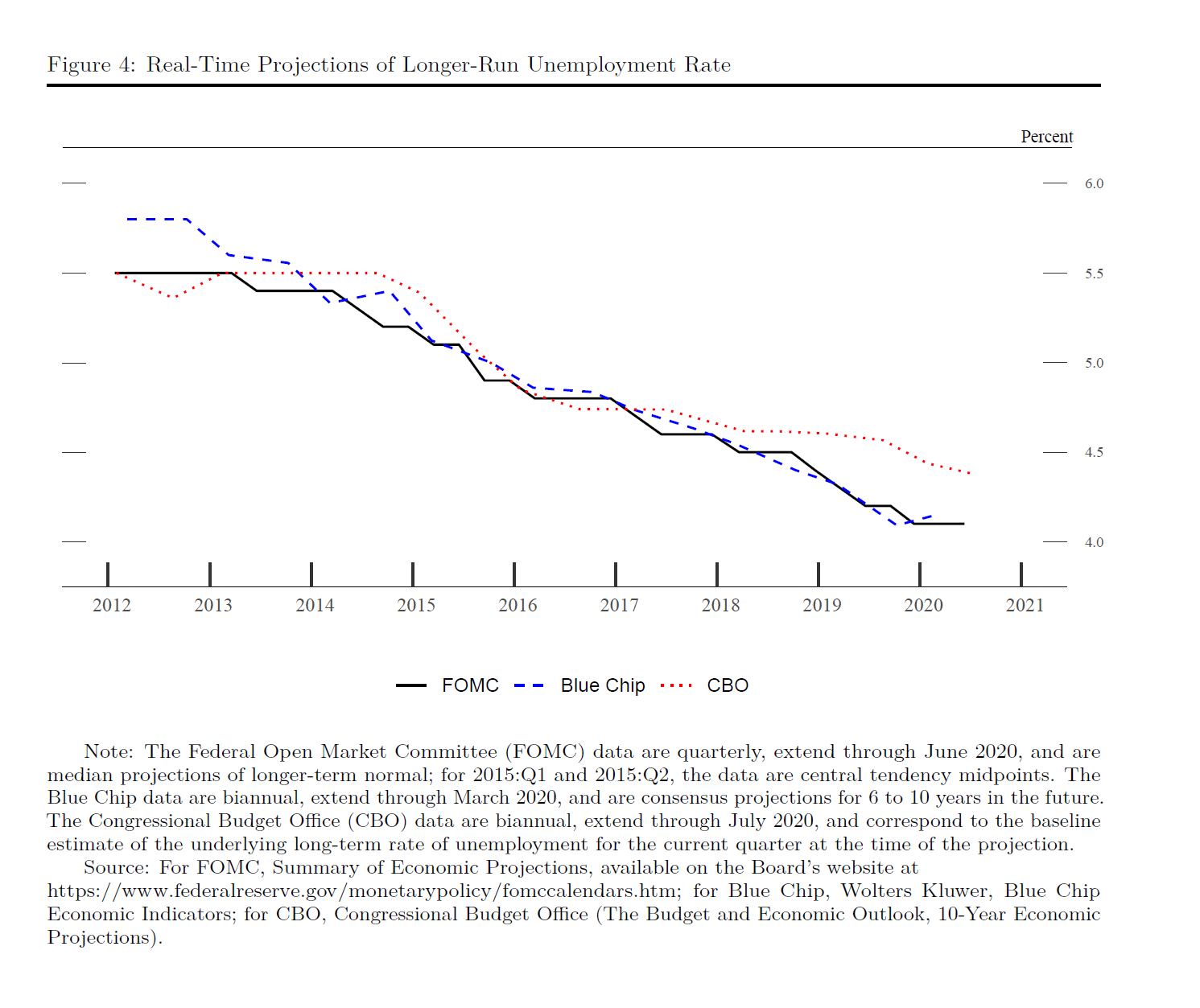

Fourth, the historically strong labor market did not trigger a significant rise in inflation. Over the years, forecasts from FOMC participants and private-sector analysts routinely showed a return to 2 percent inflation, but these forecasts were never realized on a sustained basis (see figure 3). Inflation forecasts are typically predicated on estimates of the natural rate of unemployment, or “u-star,” and of how much upward pressure on inflation arises when the unemployment rate falls relative to u-star.16 As the unemployment rate moved lower and inflation remained muted, estimates of u-star were revised down. For example, the median estimate from FOMC participants declined from 5.5 percent in 2012 to 4.1 percent at present (see figure 4). The muted responsiveness of inflation to labor market tightness, which we refer to as the flattening of the Phillips curve, also contributed to low inflation outcomes.17 In addition, longer-term inflation expectations, which we have long seen as an important driver of actual inflation, and global disinflationary pressures may have been holding down inflation more than was generally anticipated. Other advanced economies have also struggled to achieve their inflation goals in recent decades.

The persistent undershoot of inflation from our 2 percent longer-run objective is a cause for concern. Many find it counterintuitive that the Fed would want to push up inflation. After all, low and stable inflation is essential for a well-functioning economy. And we are certainly mindful that higher prices for essential items, such as food, gasoline, and shelter, add to the burdens faced by many families, especially those struggling with lost jobs and incomes. However, inflation that is persistently too low can pose serious risks to the economy. Inflation that runs below its desired level can lead to an unwelcome fall in longer-term inflation expectations, which, in turn, can pull actual inflation even lower, resulting in an adverse cycle of ever-lower inflation and inflation expectations.

This dynamic is a problem because expected inflation feeds directly into the general level of interest rates. Well-anchored inflation expectations are critical for giving the Fed the latitude to support employment when necessary without destabilizing inflation.18 But if inflation expectations fall below our 2 percent objective, interest rates would decline in tandem. In turn, we would have less scope to cut interest rates to boost employment during an economic downturn, further diminishing our capacity to stabilize the economy through cutting interest rates. We have seen this adverse dynamic play out in other major economies around the world and have learned that once it sets in, it can be very difficult to overcome. We want to do what we can to prevent such a dynamic from happening here.

…

New Statement on Longer-Run Goals and Monetary Policy Strategy

[…] Our new consensus statement, like its predecessor, explains how we interpret the mandate Congress has given us and describes the broad framework that we believe will best promote our maximum-employment and price-stability goals. Before addressing the key changes in our statement, let me highlight some areas of continuity. We continue to believe that specifying a numerical goal for employment is unwise, because the maximum level of employment is not directly measurable and changes over time for reasons unrelated to monetary policy. The significant shifts in estimates of the natural rate of unemployment over the past decade reinforce this point. In addition, we have not changed our view that a longer-run inflation rate of 2 percent is most consistent with our mandate to promote both maximum employment and price stability. Finally, we continue to believe that monetary policy must be forward looking, taking into account the expectations of households and businesses and the lags in monetary policy’s effect on the economy. Thus, our policy actions continue to depend on the economic outlook as well as the risks to the outlook, including potential risks to the financial system that could impede the attainment of our goals.

The key innovations in our new consensus statement reflect the changes in the economy I described. Our new statement explicitly acknowledges the challenges posed by the proximity of interest rates to the effective lower bound. By reducing our scope to support the economy by cutting interest rates, the lower bound increases downward risks to employment and inflation.22 To counter these risks, we are prepared to use our full range of tools to support the economy.

With regard to the employment side of our mandate, our revised statement emphasizes that maximum employment is a broad-based and inclusive goal. This change reflects our appreciation for the benefits of a strong labor market, particularly for many in low- and moderate-income communities.23 In addition, our revised statement says that our policy decision will be informed by our “assessments of the shortfalls of employment from its maximum level” rather than by “deviations from its maximum level” as in our previous statement.24 This change may appear subtle, but it reflects our view that a robust job market can be sustained without causing an outbreak of inflation.

In earlier decades when the Phillips curve was steeper, inflation tended to rise noticeably in response to a strengthening labor market. It was sometimes appropriate for the Fed to tighten monetary policy as employment rose toward its estimated maximum level in order to stave off an unwelcome rise in inflation. The change to “shortfalls” clarifies that, going forward, employment can run at or above real-time estimates of its maximum level without causing concern, unless accompanied by signs of unwanted increases in inflation or the emergence of other risks that could impede the attainment of our goals.25 Of course, when employment is below its maximum level, as is clearly the case now, we will actively seek to minimize that shortfall by using our tools to support economic growth and job creation.

We have also made important changes with regard to the price-stability side of our mandate. Our longer-run goal continues to be an inflation rate of 2 percent. Our statement emphasizes that our actions to achieve both sides of our dual mandate will be most effective if longer-term inflation expectations remain well anchored at 2 percent. However, if inflation runs below 2 percent following economic downturns but never moves above 2 percent even when the economy is strong, then, over time, inflation will average less than 2 percent. Households and businesses will come to expect this result, meaning that inflation expectations would tend to move below our inflation goal and pull realized inflation down. To prevent this outcome and the adverse dynamics that could ensue, our new statement indicates that we will seek to achieve inflation that averages 2 percent over time. Therefore, following periods when inflation has been running below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time.

In seeking to achieve inflation that averages 2 percent over time, we are not tying ourselves to a particular mathematical formula that defines the average. Thus, our approach could be viewed as a flexible form of average inflation targeting.26 Our decisions about appropriate monetary policy will continue to reflect a broad array of considerations and will not be dictated by any formula. Of course, if excessive inflationary pressures were to build or inflation expectations were to ratchet above levels consistent with our goal, we would not hesitate to act.

The revisions to our statement add up to a robust updating of our monetary policy framework. To an extent, these revisions reflect the way we have been conducting policy in recent years. At the same time, however, there are some important new features. Overall, our new Statement on Longer-Run Goals and Monetary Policy Strategy conveys our continued strong commitment to achieving our goals, given the difficult challenges presented by the proximity of interest rates to the effective lower bound. In conducting monetary policy, we will remain highly focused on fostering as strong a labor market as possible for the benefit of all Americans. And we will steadfastly seek to achieve a 2 percent inflation rate over time.

Vir: Jerome Powell, FED Chair

{kind=link}

{kind=link}

{kind=link}

{kind=link}