Eno najbolj pogostih vprašanj zadnje tedne je, zakaj kljub zgodovinskemu strmoglavljenju gospodarske aktivnosti v razvitih državah zaradi korona pandemije borzni indeksi bikovsko divjajo. Različne razlage so na voljo, najbolj popularne gredo v smer “norosti finančnih vlagateljev ob poplavi likvidnosti, s katero centralne banke v nepojmljivih količinah zalivajo trge”. No, Davide Delle Monache, Ivan Petrella in Fabrizio Venditti so v zadnjem članku postregli z zelo racionalno razlago:

Pozitiven dohodkovni tok, diskontiran z ničelno obrestno mero, je vreden neskončno. Drugače povedano, ker so obrestne mere na (varne) državne obveznice, ki jih investitorji uporabljajo kot diskontni faktor pri vrednotenju, so vrednotenja delnic poletela v nebo.

Evidence from the investigation suggests that, from a longer-term perspective, high asset valuations may reflect more than just investor optimism. The greater expected income, in comparison to government bonds, could be the key as to why investors are continuing to trust in the stock market, irrespective of the turbulent wider economic climate.

…

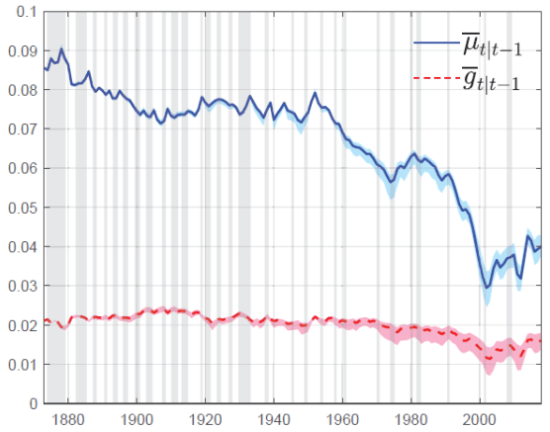

We document that the secular rise in valuations is mainly due to lower expected stock returns, which have fallen from approximately 8% to 4% over the last 150 years (Figure 2, blue line). The long run growth of dividends has also fallen, but only mildly (from 2% to 1.5%, Figure 2 red line), and cannot account quantitatively for the rise in valuations. This result is fairly intuitive. In a world of secular stagnation, i.e. low growth and low rates, one would not expect dividend growth but rather low discount rates to raise stock prices. Our work provides an exact decomposition of the contribution of these two factors.

Figure 2 Long-run expected returns, expected dividend growth and price dividend ratio.

Note: Estimated long-run component of expected returns (blue) and dividend growth (red). Bands around the estimates correspond to the 68% confidence interval obtained through simulation. Vertical shadows indicate recessions as identified by the National Bureau of Economic Research (NBER).

But why have discount rates fallen so much? Stocks are valued like ‘bonds plus risk’. Hence, either the long-run expected return on bonds (a measure of ‘r-star’) has fallen, or risk appetite has increased. In our paper, we further delve into this question and use our methodology to decompose expected stock returns into a safe component and a long-run equity premium. We find that the former is mostly responsible for the rise in stock valuations. According to our analysis, r-star has fallen from around 3% in the 1950s to a current value of about 0.5% (Figure 3, blue line). It should be noted that these results are not distant from estimates of r-star obtained by Laubach and Williams (2003). The long-run equity premium, on the other hand, has remained roughly. If anything, it has slightly risen after 2000, a result that is broadly consistent with the evidence in Farhi and Gourio (2018).

Our findings have important implications for interpreting current market conditions. First, our work confirms that discount rates, rather than dividend growth, need to take centre stage in the debate over stock prices (Cochrane 2011). Further, the behaviour of stock prices throughout the Covid-19 crisis is, in this respect, no exception. The pandemic recession has dealt yet another blow to the equilibrium interest rate, and global monetary policy accommodation has further reduced the yield on short- and long-term dated government bonds. As the bond yield squeeze is set to persist for a long time, investors will keep reaching for yield, and valuations will remain above their long-term average.

Second, the low level of interest rates at which markets entered the current crisis could have further exacerbated this reach for yield. In a recent paper, Campbell and Sigalov (2020) show that investors (i) reach for yield as risk-free rates fall and the equity premium remains constant (exactly what has happened in the past 150 years according to our analysis), and (ii) the lower the initial level of interest rates, the more investors reach for yield as rates fall further.

Third, our analysis sheds some light on the role that monetary policy (relative to other secular factors) has played in boosting stock prices. According to our results, the fall in the safe real rate of interest pre-dates the wave of liquidity injected by central banks into financial markets since the global crisis. This suggests that secular factors like population ageing, rising scarcity of safe assets, and the fall in the equilibrium rate of economic growth (Caballero et al. 2017) are mostly responsible for persistently high stock valuations, rather than monetary policy itself.

Vir: Delle Monache, Petrella & Venditti, COVID-19 and the stock market: Long-term valuations

You must be logged in to post a comment.