Zadnje leto in pol z enim očesom z zanimanjem spremljam veliko bitko v ekonomski blogosferi o t.i. “neofisherizmu“. Gre za bitko za interpretacijo istega pojava: ali zvišanje (nominalne) obrestne mere znižuje inflacijo ali pa obratno da zvišanje obrestne mere tudi dvigne inflacijo. Prva trditev je konvencionalna monetarna politika, druga pa sledi Fisherjevi enačbi, po kateri je nominalna obrestna mera vsota realne obrestne mere in inflacije. Torej če centralna banka znižuje obrestno mero, posledično (ob približno konstantni realni obrestni meri) tudi znižuje inflacijo. Dolgo obdobje nizkih obrestnih mer ima za posledico deflacijske trende. Torej tudi kvantitativno sproščanje kot zadnje in najbolj masovno orožje centralnih bank, da bi spodbudile rast cen, dejansko še poglablja deflacijske težnje.

Podatki kažejo v smer nefisherjanskega mehanizma, toda nihče (razen nekaj neomonetaristov) si pravzaprav ne upa v to zares “verjeti”. Ker je izven konvencionalne logike monetarne politike in ker to pomeni, da so centralne banke zamešale predznake. The jury is still out. Spodaj je zanimiv poljuden opis problema s strani vedno lucidnega Noaha Smitha:

Over the last three years, a quiet rebellion seems to have sprung up in macroeconomic circles. So far, it’s limited to a few whispers, a couple of papers, and the odd blog post or dinner speech, but it represents a striking break from conventional thinking. And despite my best efforts, I find myself unable to convince myself that it’s wrong. The rebellious idea – which I’ve decided to call “Neo-Fisherite” – is that low interest rates cause deflation, and high interest rates cause inflation.

First, the basic idea. The Fisher Relation says that nominal interest rates are the sum of real interest rates and inflation:

R = r + i

That’s not an assumption, that’s just a definition (actually it’s an approximation, but close enough). What I call the “Neo-Fisherite” assumption is that in the long term, r (the real interest rate) goes back to some equilibrium value, regardless of what the Fed does. So if the Fed holds R (the nominal interest rate) low for long enough, eventually inflation has to fall. This is exactly the opposite of the “monetarist” conclusion that if the Fed holds R very low for long enough, inflation will trend upward.

The opening shot of the Neo-Fisherite rebellion was fired by Minneapolis Fed President Narayana Kocherlakota, in a speech in 2010:

The fed funds rate is roughly the sum of two components: the real, net-of-inflation, return on safe short-term investments and anticipated inflation. Monetary policy does affect the real return on safe investments over short periods of time. But over the long run, money is, as we economists like to say, neutral. This means that no matter what the inflation rate is and no matter what the FOMC does, the real return on safe short-term investments averages about 1-2 percent over the long run.

Long-run monetary neutrality is an uncontroversial, simple, but nonetheless profound proposition. In particular, it implies that if the FOMC maintains the fed funds rate at its current level of 0-25 basis points for too long, both anticipated and actual inflation have to become negative. Why? It’s simple arithmetic. Let’s say that the real rate of return on safe investments is 1 percent and we need to add an amount of anticipated inflation that will result in a fed funds rate of 0.25 percent. The only way to get that is to add a negative number—in this case, –0.75 percent.

To sum up, over the long run, a low fed funds rate must lead to consistent—but low—levels of deflation. (emphasis mine)

This sparked a furious backlash in the blogs (see here, here, and here for just a few examples). Especially note the detailed critiques by Andy Harless and Brad DeLong.

Following that controversy, Kocherlakota famously converted to a more conventional monetarist position and began arguing for more QE and higher inflation (raising the interesting, but almost certainly fantastical, possibility that his conversion is a deep-cover operation and he really still thinks “easy” monetary policy will be deflationary!).

But others emerged to pick up the banner of rebellion.

The second outbreak of the rebellion came when Steve Williamson wrote a paper in which QE is deflationary. This touched off possibly the most entertaining and explosive debate in the history of the macroeconomics blogosphere. “Monetarist”-leaning bloggers like Scott Sumner and Nick Rowe teamed up with “Keynesian”-type bloggers like Brad DeLong and Paul Krugman to assail Williamson’s idea, while a few mavericks like Tyler Cowen, David Andolfatto, and me came cautiously to Williamson’s defense (without believing in his model per se). I have no idea how much of a splash the paper made within academia itself, but that would be interesting to know.

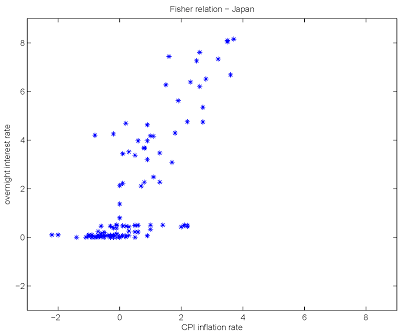

Anyway, unlike Kocherlakota, Williamson has stuck to his guns. Last December, he wrote a blog post suggesting that Paul Volcker whipped inflation in the early 80s not by raising interest rates in the short term, but by lowering them in the long term. In February he wrote that “there’s a clear Fisher relation in the data” for both Japan and the U.S., posting this graph:

The graph shows a positive contemporaneous correlation between inflation and interest rates (which monetarists, of course, would claim is evidence that interest rates are lowered in response to deflationary shocks).

In a recent “debate” with Mark Thoma (who took a fairly conventional monetarist view), Williamson again reiterated the Neo-Fisherite idea.

Last December, Williamson’s revolt got some heavyweight support when it was joined by John Cochrane:

I’ve been following with interest the rumblings of economists playing with an amazing idea — what if we have the sign wrong on monetary policy? Could it be that raising the interest rate raises inflation, and not the other way around?

Conventional wisdom says no, of course: raising interest rates lowers inflation in the short run and and only raises inflation in a very long run if at all.

The data don’t scream such a negative relation. Both the secular trend and the business cycle pattern show a decent positive association of interest rates with inflation, culminating in our current period of inflation slowly drifting down despite the Fed’s $3 trillion dollars worth of QE.

Cochrane proceeds to write down a reduced-form model in which a long period of low interest rates causes inflation to jump up for a short while but then trend downward in the long run. He concludes cautiously:

Obviously this is not the last word. But, it’s interesting how easy it is to get positive inflation out of an interest rate rise in this simple new-Keynesian model with price stickiness.

So, to sum up, the world is different. Lessons learned in the past do not necessarily apply to the interest on ample excess reserves world to which we are (I hope!) headed. The mechanisms that prescribe a negative response of inflation to interest rate increases are a lot more tenuous than you might have thought. Given the downward drift in inflation, it’s an idea that’s worth playing with.

I don’t “believe” it yet (I hate that word — there are models and evidence, not “beliefs” — but this is the web, and it’s easy for the fire-breathing bloggers of the left to jump on this sort of playfulness and write “my God, that moron Cochrane ‘believes’ monetary policy signs are wrong” — so one has to clarify this sort of thing.) We need to explore the question in a much wider variety of models.

About a month ago, Cochrane followed up with a simple structural model that includes the Fed and the Treasury, and gets the same results. He also notes how normal monetary policy deals with the Fisher Relation:

Nominal rate = real rate plus expected inflation. Tradition says though that you temporarily steer the wrong way. First lower the nominal rate, then inflation picks up, then deftly raise the nominal rate to match inflation. If you instead raise rates and then just sit there waiting for inflation to catch up all sorts of unstable things happen…But maybe not.

Just a few days ago, Williamson evaluated Lars Svensson’s policy advice from a Neo-Fisherite point of view, summing up the core of the rebellion quite well:

For simplicity, think about a world with perfect certainty. In the long run, standard asset pricing gives us the Fisher relation, which is

R = r + i,

where R is the short-term nominal interest rate, r is the real interest rate, and i is the inflation rate…Therefore, in the long run, if R is targeted at its lower bound by the central bank,

i = – r – t

So, if we think that r is invariant to monetary policy in the long run, then if the central bank pegs the nominal interest rate at its lower bound, and central bank liabilities are taxed, this will make long-run inflation lower.

(Note that the Neo-Fisherite idea is NOT that a fall in interest rates causes the price level to jump up and then drift back down to its original level. If the Neo-Fisherites are right, holding interest rates at low levels for a long time will cause a long-term deflationary trend that will eventually push the price level lower than if interest rates had been kept at the old, higher level.)

So why do I find myself unable to convince myself that the Neo-Fisherite idea is wrong? Well, like Cochrane, I don’t really “believe” in any of these specific models (or any others). But two things make me unwilling to discount the Neo-Fisherites. The first is a thought experiment, and the second is the evidence.

The thought experiment is this: Suppose there was no government debt, and the Fed raised nominal interest rates to 20% and held them there forever. What would happen to real rates? Well, they wouldn’t rise to 20% forever, because there’s just no way that our society can physically, technologically deliver a 20% riskless rate of return to bondholders. Eventually, one of two things would have to happen: either 1) the Fed’s control over the nominal interest rate would break down, or 2) inflation would rise (the Neo-Fisherite result). If the Fed can’t control the nominal interest rate, then our standard models of monetary policy all break down, and we have to think about the microeconomics of money demand, which is hard to do. But the only alternative would be the Neo-Fisherite result.

As for the evidence, the U.S. case is more interesting to me than the case of Japan. In Japan, population growth is negative and Total Factor Productivity is stagnant, raising the obvious possibility of a Larry Summers-style “secular stagnation”, where interest rates look low but are in fact high. But in the United States, productivity and population both continue to grow at a reasonable clip, so while “secular stagnation” seems possible, it would require some more stuff in the basic model that I haven’t seen yet. Meanwhile, QE, while it produces slight jumps in inflation expectations whenever a policy change is announced or an asset purchase is made, has overall coincided with a downward drift in inflation. Monetarists will say that this is because of expectations that the Fed’s asset purchases won’t be permanent, and of course we can’t rule that out. We can’t really rule anything out in macro, even serious academic macro, much less the “eyeball-it-and-see-what-you-think” approach taken on the blogs (and in much of the private sector).

But what I’m saying is, there seems as of yet no obvious reason for me to write off the Neo-Fisherite idea. And – as Cochrane and Williamson have both shown – it’s possible to write down models where the idea works. The structural models so far all rely on rather odd and rigid fiscal policy rules, so the microfoundations are still kind of crazy. But I see no reason why those models are substantially crazier than any of the more mainstream, monetarist-type (or RBC-type) models. So for now, count me on the side of the Neo-Fisherite rebels, just because I think the idea is neat, and potentially very important, and I want to see where it leads.

Because the idea is very important. Everything the Fed does, pretty much, is based on the idea that the longer you hold interest rates at low levels, the “easier”- i.e. the more pro-growth and inflationary – your monetary policy is. The Neo-Fisherite idea doesn’t just discount the effectiveness of monetary policy(like RBC models do, or like the MMT people do) – it stands that whole monetary policy universe on its head. If the Neo-Fisherites are right, then not only is the Fed massively confused about what it’s doing, but much of the private sector may be reacting in the wrong way to monetary policy shifts.

Vir: Noah Smith