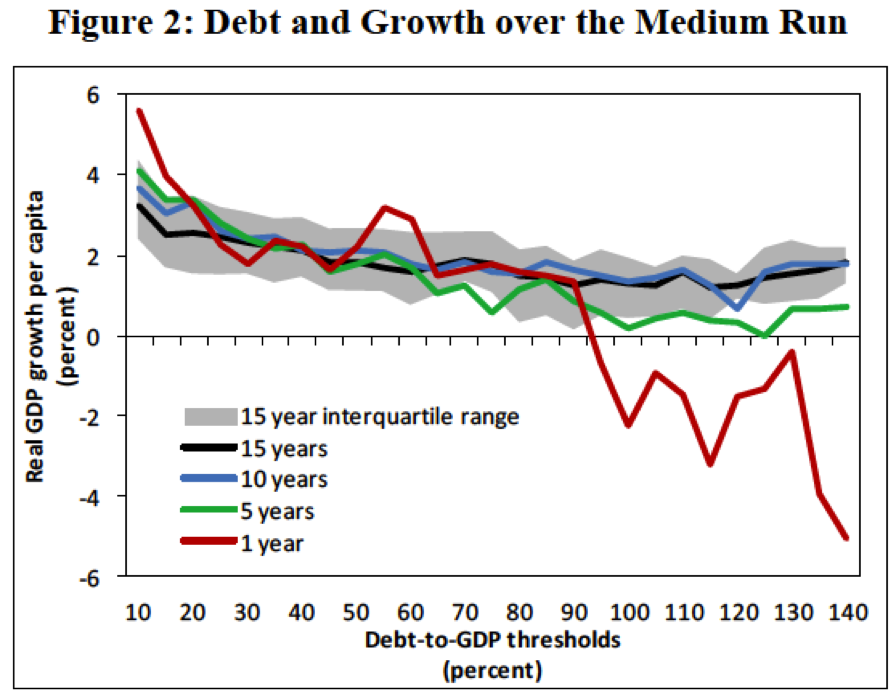

Še vroča študija raziskovalcev IMF (Pescatori, Sandri & Simon (februar 2014) “Debt and Growth: Is There a Magic Threshold?“) kaže, da med dolgom in gospodarsko rastjo ni značilne povezave. Ali drugače, ugotavljajo, da ne obstaja neka magična meja, nad katero bi dolg negativno vplival na gospodarsko rast, kot sta denimo trdila Reinhartova in Rogoff (2010) v njuni kontroverzni in s številnimi napakami obremenjeni študiji. Pescatori et al (2014) pravijo, da je pri povezavi med dolgom in rastjo treba gledati daljše časovne učinke in ne zgolj na kratkoročne učinke. Te razlike najbolje prikazuje spodnja slika:

Vir: Pescatori, Sandri & Simon (2014)

Vir: Pescatori, Sandri & Simon (2014)

Če gledamo učinke dolga samo na rast v naslednjem letu, je visok dolg problematičen za rast, pri 5-letni dinamiki rasti že manj, medtem ko je pri 10- ali 15-letni dinamiki rasti dolg nad 120% BDP ni nič bolj problematičen kot dolg v višini 50% ali 70% BDP. To z drugimi besedami pomeni, da države, ki so zašle v recesijo, ne bi smele zaiti v histerično zniževanje dolga na vrat na nos (s politiko varčevanja), pač pa predvsem zagnati gospodarsko rast (tudi z višjim dolgom) in tako na srednji rok prek rastočega BDP uspešno znižati povečan dolg (relativno glede na BDP). To so nenazadnje pokazale tudi ostale študije IMF v zadnjih dveh letih.

Pri tem je treba gledati tudi na dinamiko dolga, saj je gospodarska rast manj obremenjena z visokim dolgom, kadar ta trendno upada, kot pa obratno. To je seveda logično, saj se v recesiji (v času negativne rasti) države zadolžujejo (tudi če dolg ostane enak, se kazalec dolg glede na BDP zaradi manjšega imenovalca povečuje), v času pozitivne rasti pa zmanjšujejo dolg. Vzročnosti med obema je težko povsem priti do konca.

Seveda pa zgornje ugotovitve še ne pomenijo, da visok dolg ni problematičen sam po sebi. Problematičen je denimo lahko zaradi omejitev na strani monetarne in fiskalne politike ter zaradi zmanjšane zmožnosti zadolževanja v tujini po sprejemljivih obrestnih merah, saj ob višjem in naraščajočem dolgu finančni trgi zahtevajo višje obrestne mere (razen, če se država imenuje ZDA ali Japonska). To z drugimi besedami pomeni, da lahko poslabšan dostop na finančne trge in omejitve fiskalne politike ob visokem dolgu vplivajo na večjo volatilnost gospodarske rasti države. Natanko to ugotavljajo tudi Pescatori et al (2014).

Še kratek povzetek njihovih ugotovitev v originalu:

Is there a particular threshold in the level government debt above which the medium-term growth prospects are dramatically compromised? The answer to this question is of critical importance given the historically high level of public debt in most advanced economies. Yet there is currently no agreement on the answer and it is the subject of heated academic and political debate. One camp has argued that high levels of debt are associated with particularly large negative effects on growth. For example, an influential series of papers by Reinhart and Rogoff (2010, 2012) argues that there is a threshold effect whereby debt above 90 percent of GDP is associated with dramatically worse growth outcomes.

An opposing perspective is advanced by those who dispute the notion that there is a clear debt threshold above which debt sharply reduces growth and raise endogeneity concerns whereby weak growth is the cause of particularly high levels of debt. Thus, according to this view, the priority should be increasing growth rather than reducing debt and, consequently, that much less short-term fiscal austerity is appropriate.

This paper makes a contribution to the debate by presenting new empirical evidence based on a different way of analyzing the data and a sizeable dataset. Our methodology is based on the analysis of the relation between debt and growth over longer periods of time that has the potential to attenuate the concerns of reverse causality from growth to debt. Our results do not identify any clear debt threshold above which medium-term growth prospects are dramatically compromised. On the contrary, the association between debt and medium-term growth becomes rather weak at high levels of debt, especially when controlling for the average growth performance of country peers.

We also find evidence that the debt trajectory can be just as important, and possibly more important, than the level of debt in understanding future growth prospects. Indeed, countries with high but declining levels of debt have historically grown just as fast as their peers. We also find, however, that high levels of debt are weakly associated with higher output volatility. This suggests that high levels of debt may still be associated with market pressure or fiscal and monetary policy actions that, even if they do not have particularly large negative effects on medium-term growth, destabilize it.

As with previous empirical studies, however, caution should be used in the interpretation of our empirical results. While our methodology may attenuate problems of reverse causality from growth to debt, our methodology is still unable to formally establish a firm causality.

Vir: Pescatori, Sandri & Simon (2014)

You must be logged in to post a comment.