Tisti, ki se malce zanimate za energetiko, ste v zadnjem desetletju in pol hypa glede “zelenega prehoda” zasledili, da naj bi v tem zelenem prehodu (razogljičenju proizvodnje električne energije, transporta in industrije) ključno vlogo odigral vodik. Naj osvežim spomin. Iz viškov električne energije iz (obnovljivih virov) sonca in vetra naj bi prek elektrolize vodo (H2O) pretvarjali v vodik (H2), vodik shranjevali, ga nato pretvorili v sintetični metan, tega pa nato kurili namesto zemeljskega plina za proizvodnjo elektrike. Avtomobili naj bi vozili na vodik, kamioni in ladje pa na sintetični metanol. In industrija naj bi namesto zemeljskega plina uporabljala vodik za proizvodnjo toplotne energije. Lepota vodika je v tem, da je brezogljičen in da torej pri njegovem “kurjenju” ne nastajajo emisije CO2.

Nič čudnega, da so “najbolj napredne države, na čelu z Nemčijo, Evropska komisija in mednarodne organizacije, kot je Mednarodna agencija za energijo (IEA), ponoreli za “zelenim vodikom” in ga proglasili kot ključni element v razogljičenju planeta.

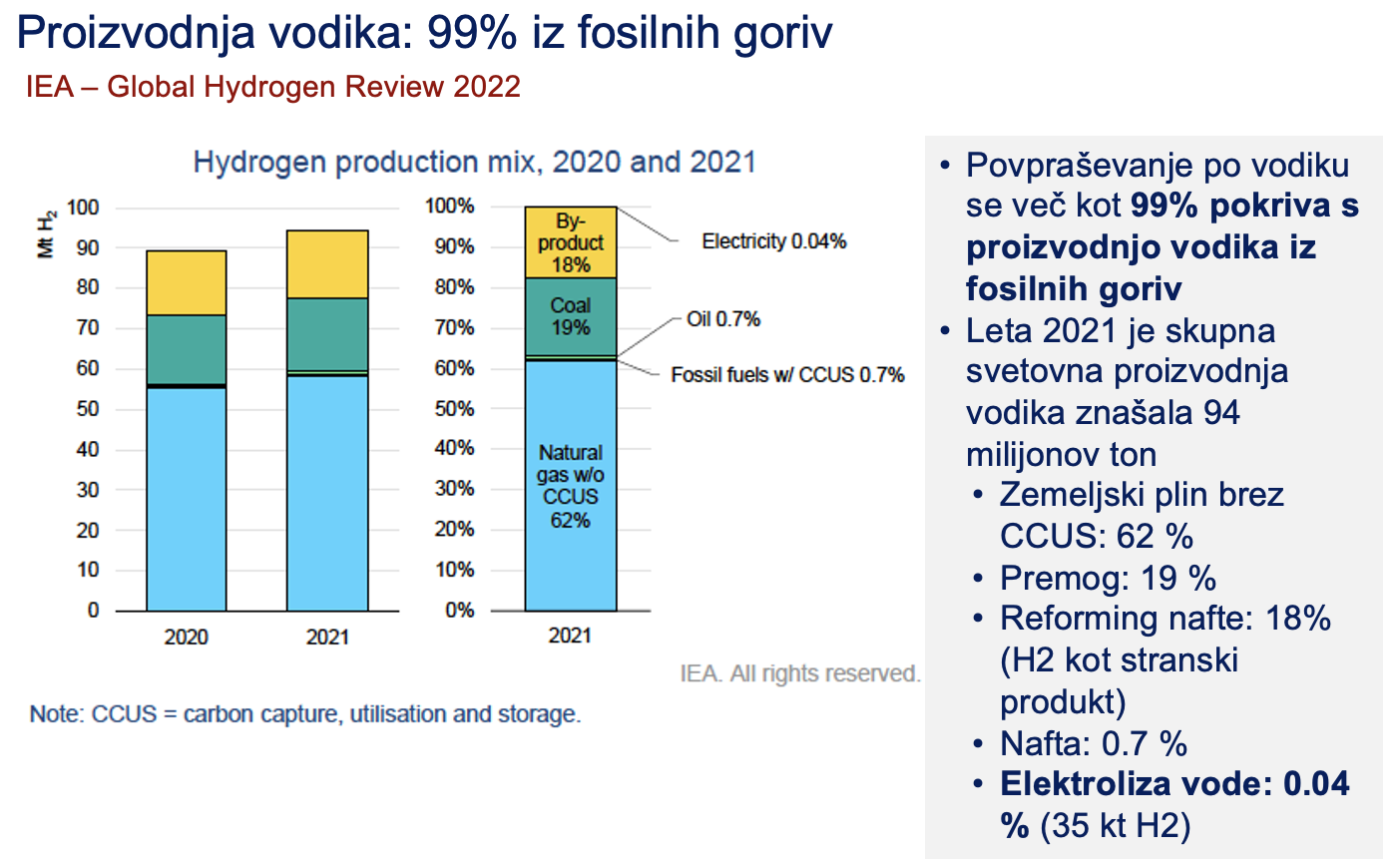

Zadeva se sliši super, mar ne? Ja, v teoriji. In dokler se ne soočimo z “težavnimi” značilnostmi vodika, z “neprijetnimi” tehničnimi dejstvi glede energetskih pretvorb in izgub energije, pa tudi ali predvsem s samimi številkami ekonomike vodikove verige. V nadaljevanju se bom malce posvetil le zadnjemu delu – ekonomiki vodika. Največji porabnik vodika danes je industrija (99.9 %) in več kot 99 % tega vodika se pridobi iz fosilnih goriv (večinoma iz zemeljskega plina, nato premoga in nafte), gre za t.i. sivi vodik, le 0.04 % pa z elektrolizo vode (zeleni vodik).

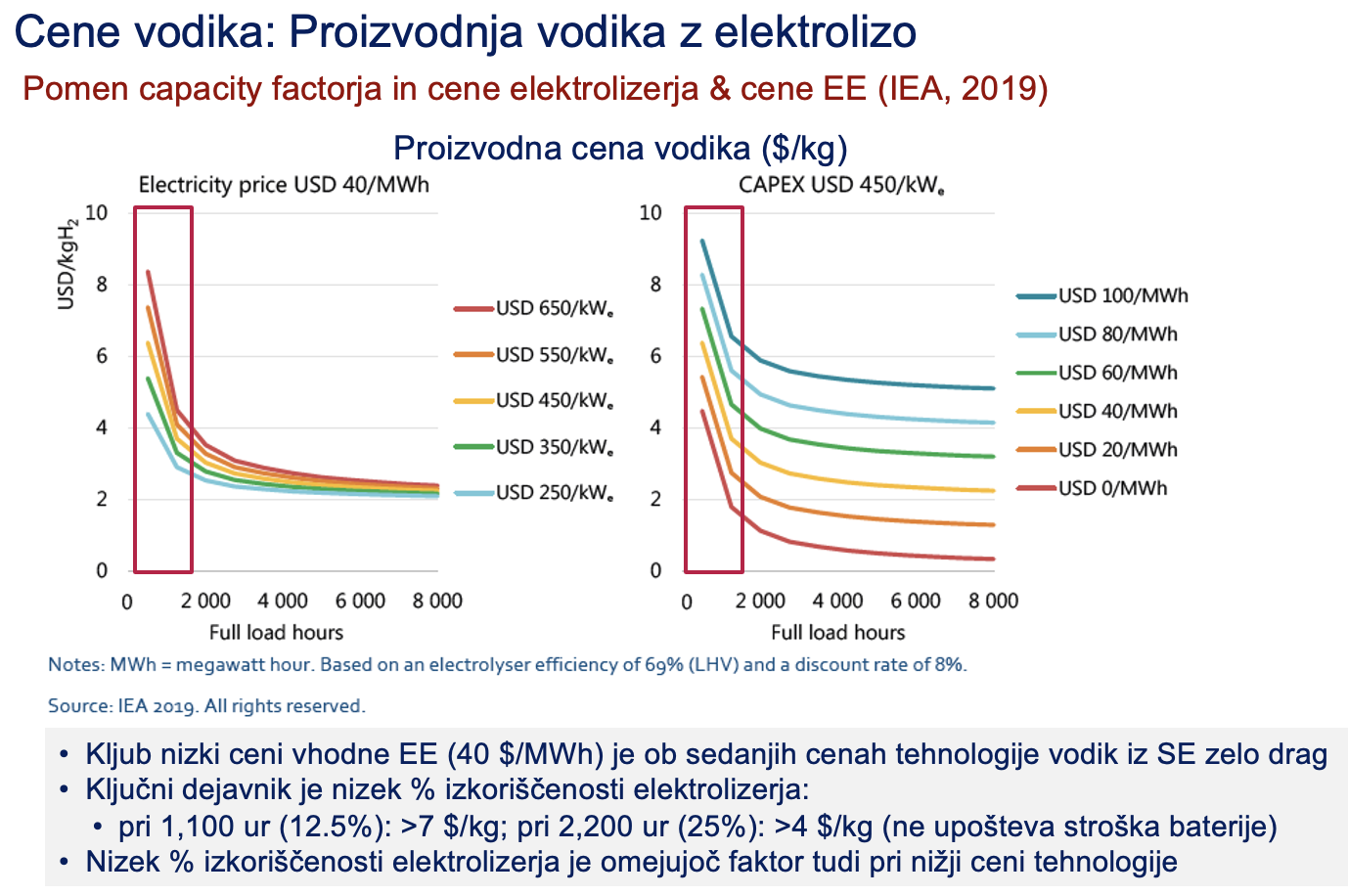

Proizvodna cena vodika iz fosilnih goriv je okrog 1.5 do 2 $ za kilogram. Če bi vodik proizvajali iz viškov sončne energije v Evropi, bi v najugodnejšem primeru (visoka stopnja izkoriščenosti elektrolizerjev, nizke cene tehnologije, nizki stroški kapitala) proizvodni strošek znašal med 6 in 7 evrov za kilogram.

Torej zeleni vodik je v najboljšem primeru za 3 do 4-krat (za 300 % do 400 %) dražji od “sivega” ali “rjavega” vodika. Ključna problema ekonomike proizvodnje vodika z elektrolizo vode sta stopnja izkoriščenosti elektrolizerjev in cena elektrike. Če bi vodik proizvajali iz viškov elektrike iz sončnih elektrarn, se nobena kalkulacija ne izide. V osrednji Evropi sonce pač sije samo okrog 1/8 časa (12.5 %) v letu, kar pomeni, da bi bili elektrolizerji skoraj 90 % časa neizkoriščeni. Nobena investicijska kalkulacija se pri tem seveda ne izide. Tudi če bi dogradili baterije za shranjevanje dnevnih viškov elektrike in tako podvojili izkoriščenost elektrolizerjev, se kalkulacija ne izide. Pri uporabi elektrike iz vetrnih elektrarn je ekonomika nekoliko manj slaba, vendar še vedno mnogo preslaba za komercialno uspešno poslovanje. In noben investitor se ne bo odločil za proizvodnjo, ki deluje samo 10 % ali (v najbolj ugodnem primeru) 40 do 50 % časa. Preostanek časa bi morali elektrolizerje poganjati na elektriko iz omrežja, ki pa je v državah z velikim deležem obnovljivih virov energije v omrežju zelo draga.

Zeleni vodik bi bilo mogočle stroškovno konkurenčno proizvajati samo ob stanovitnem viru električne energije in pri njeni zelo nizki ceni. V praksi je to mogoče samo z elektriko iz amortiziranih hidro in jedrskih elektrarn, ki poslujejo z nizkimi obratovalnimi stroški (cena elektrike med 25 in 30 EUR/MWh). Vsi ostali viri elektrike so mnogo predragi ali nestanovitni.

Hype, ki je nastal pred desetletjem glede zelenega vodika kot svetega grala zelenega prehoda danes pospešeno upada. Mednarodna agencija za energijo (IEA) je v svojem rednem letnem Global Hydrogen Review vsako leto napovedovala veliko zanimanje za investicije v proizvodnjo zelenega vodika, nakar nato vsako leto za nazaj zapiše, da je bil “lani” odstotek končnih investicijskih odločitev (final investment decision) zelo nizek. In tako leto za letom. Investitorji se ne odločajo za proizvodnjo zelenega vodika.

Spodaj sta dva članka, ki zelo nazorno kažeta, zakaj projekt zelenega vodika ne more zaživeti. Odgovor je preprost: ker zeleni vodik nima kupcev. Razlog, da jih nima, pa so mnogo previsoke cene zelenega vodika.

Ta teden so mediji objavili, da je največje podjetje na svetu za proizvodnjo električne energije iz vetrnih elektrarn, danski Ørsted, opustilo investicijo v gradnjo največje komercialne proizvodnje zelenega vodika v Evropi (v bistvu e-metanola za pogon ladij), in sicer FlagshipONE projekt v švedskem Ornskoldsviku. Pri čemer je Ørsted izgubil 220 mio evrov že investiranih sredstev. Ørsted je sicer v težavah že pri svojem osnovnem poslu, to je proizvodnji elektrike iz vetrnic, saj zaradi zmanjšanja subvencij enega za drugim opušča nove projekte vetrnih elektrarn (lani je imel 2.3 milijarde evrov izgube). Toda pri proizvodnji zelenega vodika Ørsted ni nameraval uporabljati elektrike iz nestanovitnih vetrnih elektrarn, pač iz bolj stanovitnih švedskih hidroelektrarn. Kljub temu je Ørsted sredi investicije ocenil, da projekt ne bo komercialno uspešen. Zakaj ne? Ker nikakor ni uspel pridobiti kupcev, da bi lahko zagnal proizvodnjo. Njegov vodik (e-metanol) bi bil namreč za 3 do 5-krat dražji od drugih ladijskih pogonskih goriv.

Orsted has ceased the development of its pioneering FlagshipONE eMethanol project under construction in northern Sweden, citing slow market progress and an inability to sign long-term offtake contracts, the company said Aug. 15.

he company took a final investment decision on the project in 2022 after acquiring it from Liquid Wind and was targeting emerging demand in the marine fuel sector.

“While we were aware of the substantial uncertainties and risks associated with the development of a pioneering and immature liquid e-fuel project and market at the time of the FID, it was a strategic choice to take a leading position in shaping the industry,” Orsted said in a results statement.

FlagshipONE in Ornskoldsvik was to make green hydrogen from a 70-MW electrolyzer to produce up to 55,000 metric tons per year of e-methanol from 2025 using renewable energy and biogenic CO2 captured from the nearby biomass-fired Horneborgsverket heat and power plant.

“We continue to believe in the long-term market for e-fuels, but the industrialization of the technology as well as the commercial development of the offtake market have progressed significantly slower than expected,” it said.

The cancelation of FlagshipONE, previously described by the Danish renewable energy firm as “the largest eMethanol project under construction in Europe,” came as most shipping firms remained reluctant in committing to long-term procurement contracts for methanol produced via sustainable means.

While methanol has emerged as the most popular alternative population in newbuild orders over the past year, ship operators are not willing to swallow the high costs of sustainable methanol with limited scope of passing incremental expanse onto their customers, industry participants said.

Platts bunker assessments for 0.5% sulfur fuel oil, the world’s most common type of marine fuel, stood at $13.39/Gj in Rotterdam on Aug. 14, compared with $18.01/Gj for fossil-based methanol. Industry estimates suggest sustainable methanol would be at least two to five times more expensive. Platts is part of S&P Global Commodity Insights.

Orsted said the FlagshipONE’s business case had deteriorated since taking FID, “due to the inability to sign long-term offtake contracts at sustainable pricing and significantly higher project costs.”

The company has ceased execution of the project and is to de-prioritize work within the liquid e-fuel sector, it said.

Orsted regional CEO for Europe Olivia Breese told Commodity Insights the company had advanced dialogues with several possible offtakers, but these did not progress to signing long-term contracts, despite market interest.

“We believe that this reflects the immaturity of the regulatory environment for the decarbonization of industry,” Breese said.

…

Breese said that decarbonization projects across the board were challenged by higher energy, equipment and capex costs.

“The industry is facing a significant cost-gap between e-fuels and fossil fuels,” she said, noting other decarbonization options for many offtakers are seen as more competitive. “The e-fuels industry doesn’t have firm commercial visibility on the offtake side.”

And although much of the needed EU regulation is in place, short- and medium-term regulatory requirements, such as sub-quotas for e-fuels and greenhouse gas reduction requirements, do not deliver a clear enough incentive, while national implementation and enforcement is not yet in place, Breese added.

“As a result, timelines no longer match the most matured projects, where developers struggle to find offtakers willing to match the industry production costs for such commercial scale first-of-a-kind projects,” she said.

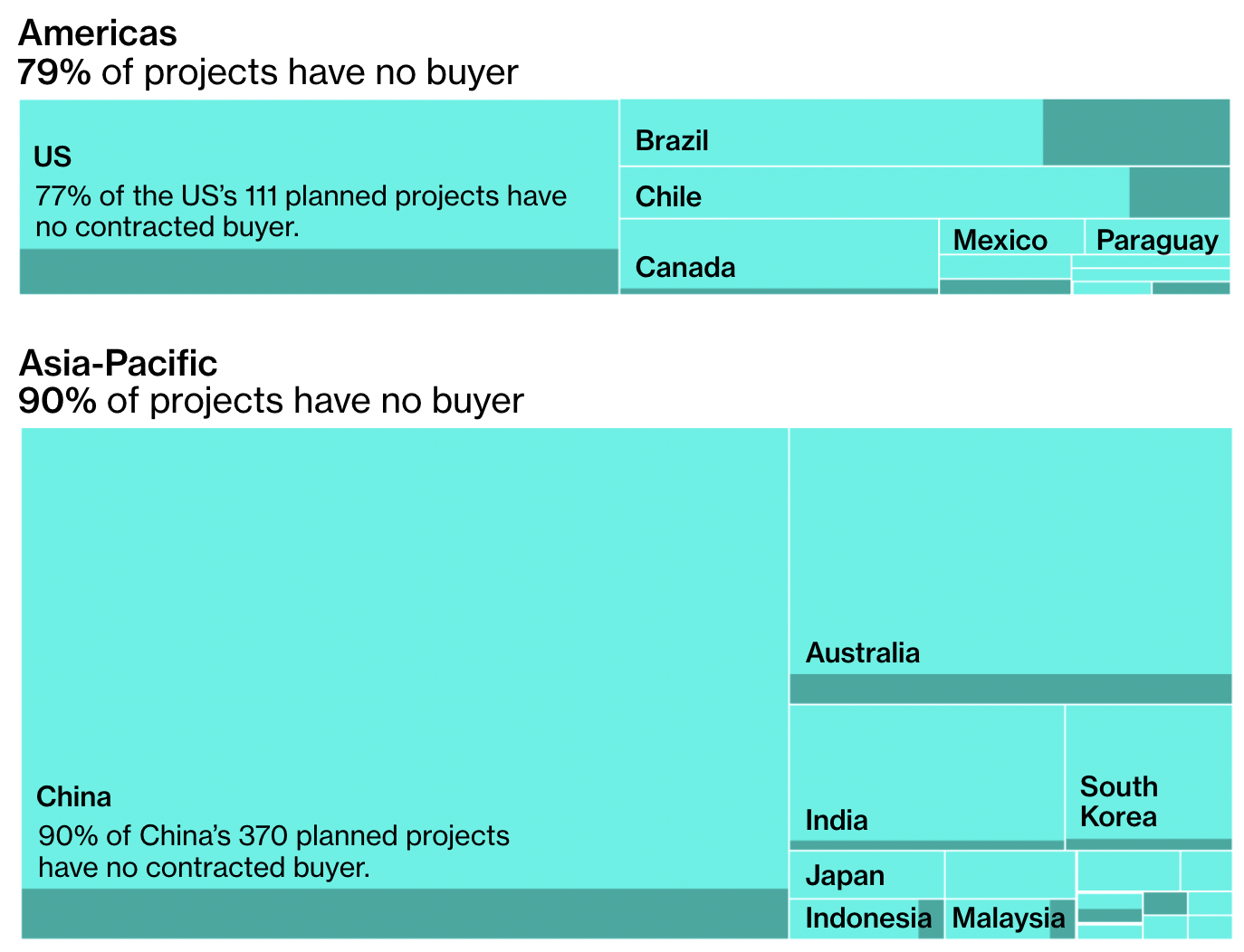

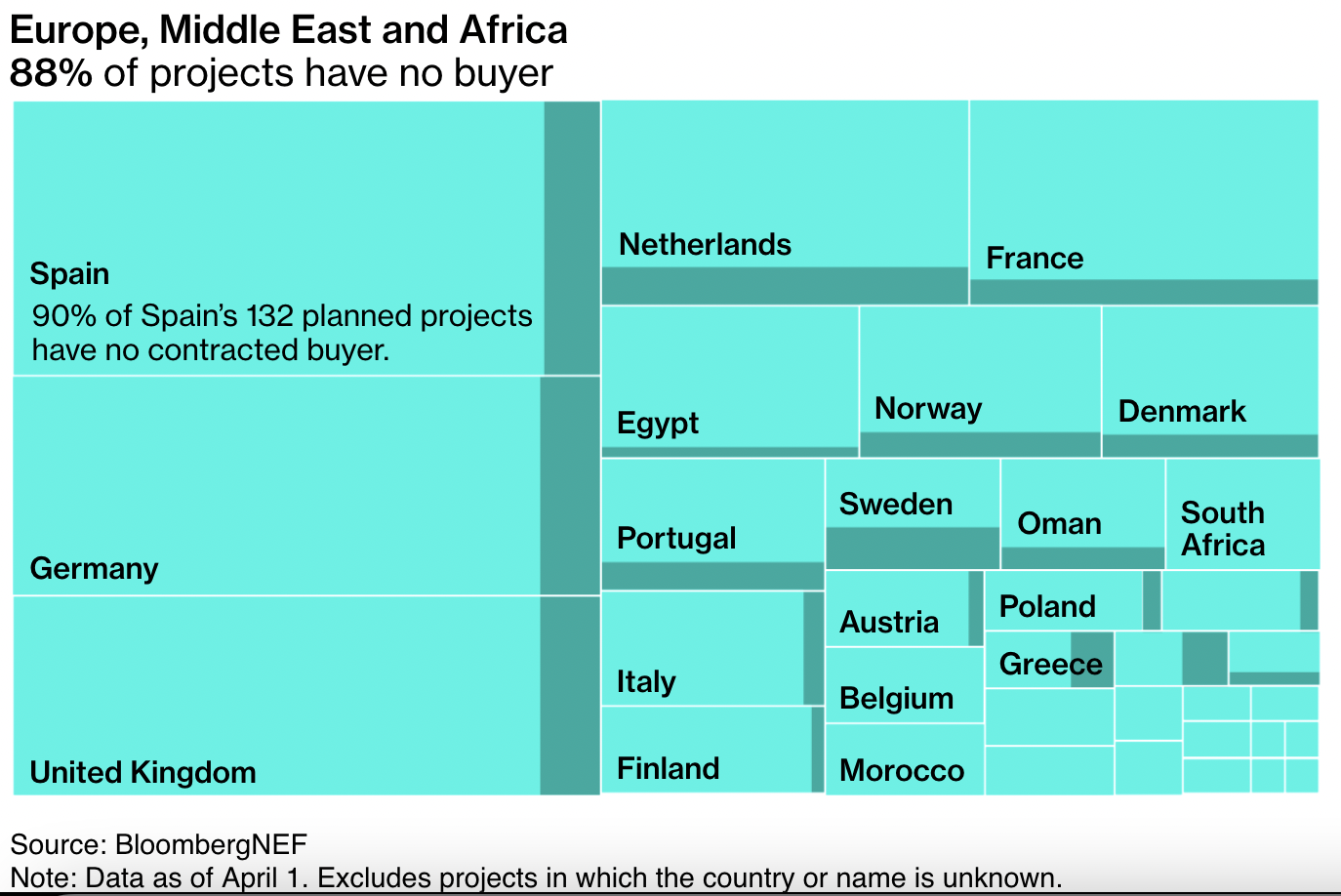

Prejšnji teden je Bloomberg objavil članek z naslovom “Zakaj skoraj nihče ne kupuje zelenega vodika?“. Članek je napisan na podlagi podatkov Bloombergove specializrane edicije za energijo BloombergNEF. V glavnem, članek ugotavlja, (1) da je zelo malo projektov za proizvodnjo zelenega vodika dobilo končno investicijsko odločitev, in (2) da se tudi tisti projekti, ki so v procesu investicije, ubadajo s kroničnim pomanjkanjem kupcev, saj 90 % projektov nima zagotovljenega niti enega kupca (pogodbe za dolgoročni odjem vodika). V ZDA 77 % izmed 111 načrtovanih projektov nima niti enega kupca, v Kitajski 90 % izmed 370 načrtovanih projektov nima niti enega kupca, v Španiji 90 % izmed 132 načrtovanih projektov nima niti enega kupca itd.

V Bloombergu kot pot k večji uspešnosti projekta zeleni vodik navajajo potrebo po subvencijah in državni regulaciji, hkrati pa kot pot h komercialni uspešnosti navajajo tudi, da je treba izgraditi celoten ekosistem, ne zgolj proizvodnje vodika. Torej, da morajo biti proizvodnja elektrike in vodika ter nato tudi industrijska poraba vodika geografsko locirani skupaj. Pri tem se sklicujejo na “uspešen švedski primer” takšnega vodikovega ekosistema, ki naj bi kot največji na svetu na leto proizvedel 50,000 tisoč ton zelenega vodika za nemške proizvajalce “zelenega jekla”.

Hydrogen’s potential as a carbon-free fuel has provoked no end of excitement. From the deserts of Australia and Namibia to the wind-blasted straits of Patagonia, companies and governments worldwide plan to build almost 1,600 plants to make it. The gas can be produced cleanly by using wind- or solar-powered electricity in a process that splits the molecule from water. There’s only one problem: The vast majority of those projects don’t have a single customer stepping up to buy the fuel.

Among the handful with some kind of fuel purchase agreement, most have vague, nonbinding arrangements that can be quietly discarded if the potential buyers back out. As a result, many of the projects now touted with great fanfare by countries vying to become “the Saudi Arabia of hydrogen” will likely never get built. Just 12% of hydrogen plants considered low-carbon because they avoid natural gas or mitigate emissions have customers with agreements to use the fuel, according to BloombergNEF.

“No sane project developer is going to start producing hydrogen without having a buyer for it, and no sane banker is going to lend money to a project developer without reasonable confidence that someone’s going to buy the hydrogen,” says BNEF analyst Martin Tengler.

…

Countries with the potential to generate abundant renewable power, such as Chile with wind and Australia and Egypt with solar, have announced grand goals to make the fuel, often for export. More than 360 plants have been announced in China alone, according to BNEF.

The European Union has set a target of producing 10 million metric tons of carbon-free hydrogen by 2030 while importing an equal amount. In the US, President Joe Biden has devoted $8 billion to creating “hydrogen hubs,” clusters of businesses making and using the fuel.

Lots of Plants, Few Customers

Almost 90% of hydrogen plants have no buyers with contracts to use the fuel

Andy Marsh, CEO of Plug Power Inc., says his company has engineering and design work underway on European projects that together would use about 4.5 gigawatts of renewable power to generate hydrogen. “If half of it comes to fruition, we’ll be happy,” he says. “If a quarter of it comes to fruition, we’ll be happy.” Although the EU has set ambitious goals, Marsh says, member states are still incorporating them into their own regulations, delaying private investments.

…

Many analysts see no other way to decarbonize steel, maritime shipping and other industries that can’t easily run on electricity. BNEF predicts we’ll need to use 390 million tons of hydrogen per year worldwide in 2050 to eliminate carbon emissions from the global economy, more than four times the amount used today.

But it’s not a simple switch. Most of the businesses that could run on hydrogen would need expensive new equipment to use it, a leap they’re reluctant to make. Hydrogen produced using clean energy costs four times as much as hydrogen made from natural gas, according to BNEF. And it’s hard to build the infrastructure to supply hydrogen—not just plants to make it but pipelines to move it—when the demand may not materialize for years.

…

Ponikwar says those likely to succeed today are ones that include “the whole ecosystem,” locating a hydrogen plant near a clean energy source, with a ready customer close at hand. His company, for example, is supplying equipment to a hydrogen plant in northern Sweden that will in turn feed an iron and steel mill being developed by H2 Green Steel, which has secured €6.5 billion ($6.9 billion) in funding for the project. The region’s abundant hydropower will provide the electricity, and Mercedes-Benz Group AG has agreed to buy 50,000 metric tons of the mill’s steel per year. “With green steel, there’s a market that’s interested to buy, and they’re willing to pay a premium for it,” Ponikwar says.

Zeleni vodik je mnogo predrag in brez visokih subvencij, državne regulacije (prisile k uporabi določenega odstotka zelenega vodika v industriji) in velikih investicij v vodikovo infrastrukturo (skladišča, vodikovodi) ne bo nikoli zaživel kot alternativa. Toda tudi takrat ne more biti racionalna alternativa, če brez stalnih subvencij države, brez državne prisile in brez državnih investiicij ne zmore biti komercialno uspešen.

Zelo zanimivo.

Všeč mi jeVšeč mi je