Moje stališče, da cenovna kapica na rusko nafto ne more delovati, je znano lani od maja ali junija. In kapica, ki je bila uvedena lani decembra, res nikoli ni delovala (padec cen ruske premijske nafte Ural je bil sicer uradno pod kapico več kot pol leta, vendar je to bolj posledica dinamike cen na naftnem trgu nasploh, hkrati pa se po tej kotaciji proda malo ruske nafte). Obstoječi ladjarji so se izognili kapici s potrdilom naročnika, da je bila nafta kupljena po ceni izpod kapice, ali pa so prodali stare tankerje neznanim novim lastnikom. Hkrati je Rusija prek slamnatih lastnikov oblikovala sivo floto zastarelih tankerjev, ki niso potrebovali zahodnega zavarovanja itd. In v teh dveh zadnjih manipulacijah je glavna nevarnost. Vsaj polovico ruske nafte prevažajo zastareli tankerji, ki bi sicer šli v razrez, in s teh tankerjev se nato na odprtem morju nafta pretaka v “legalne” tankerje, ki prevažajo nafto v zahodna pristanišča. Obstaja nevarnost za naravno katastrofo, ki pa ne bo zavarovana pri zahodnih zavarovalnicah.

In zaradi slednjega v Bloombergu kličejo k odpravi kapice, ki itak ne deluje.

_________

It gives me no pleasure to say this, but it’s time to scrap the Russian oil price cap.

The truth is, it isn’t working, and, worse, by forcing ever more Russian oil onto rusting old tankers that are engaging in inherently risky operations like ship-to-ship transfers, it raises the likelihood of an environmental disaster.

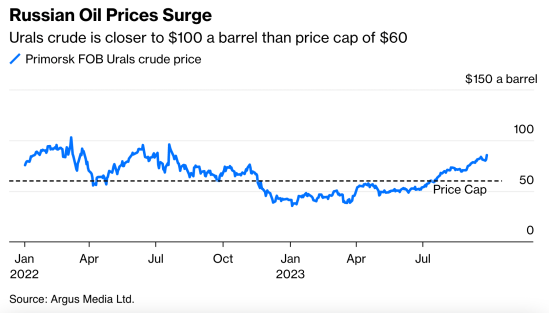

Back in December, the Group of 7 nations and several others introduced a $60-a-barrel cap on the price of Russian crude. Buyers can still pay more, but then they are deprived of access to key services supplied by firms in the signatory countries. Those include the best insurance against risks, such as collisions and spills, and the European-based tanker fleet including ships owned in Greece and Cyprus. Similar caps on refined products were introduced in February.

The aim was to allow Russian oil to keep flowing, while hitting the Kremlin’s income by forcing it to accept lower prices. The effectiveness of the cap would depend on Russia’s need for Western ships and services to keep its oil moving to international markets and its willingness to sell below the capped price.

The initiative seemed to work for a while. The country’s main Urals export grade traded below the threshold for most of the first eight months that the cap was in existence.

But that had more to do with broader oil market dynamics than with the cap mechanism. As global oil prices have risen in recent months, so has the value of Russian crude. Urals is now closer to $100 a barrel than it is to $60, with most of it carried on ships whose owners are prepared to ignore the cap.

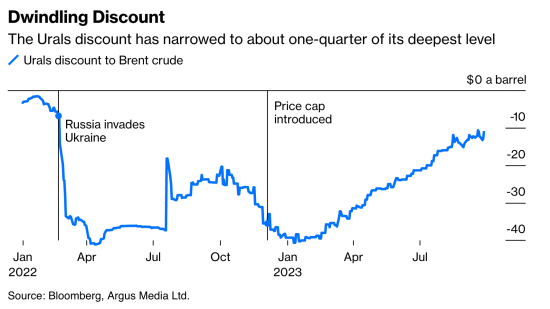

If we look at the discount to Brent instead of absolute prices, we see a rather different picture.

The discount continued to widen after the price cap came into effect, but it never exceeded the levels it reached in the first months after Russia’s attack and it wasn’t long before it began to narrow again.

The widest discounts correspond with periods when there weren’t enough ships whose owners were prepared to carry Russian crude. But since the invasion, a host of new tanker operators have amassed a fleet of aging vessels, many of which would previously have been sold for scrap, to transport Russian oil. Those rusty old tankers have raised concerns in the United Nations about an increased risk of a major oil spill. UN officials are also worried about the practices some of the ships have adopted of turning off the transponders that signal their position and of transferring cargoes from one aging vessel to another.

As this shadow fleet carries a larger and larger proportion of Moscow’s oil shipments, so the discount for Russian cargoes against international benchmarks — the primary measure of success for the price cap — has narrowed.

And although laudable in its aim, the price-cap mechanism lacks teeth.

Shipowners merely need an affidavit from the cargo owner that the consignment was purchased at a price below the cap. But there has been no appetite to check, and there’s no way of telling if what’s written in the affidavit is true. There is no realistic chance that either the seller (a Russian oil company) or the buyer (most likely a newly formed trading company set up far from the scrutiny of the US Treasury) is going to be found out if the affidavit is false.

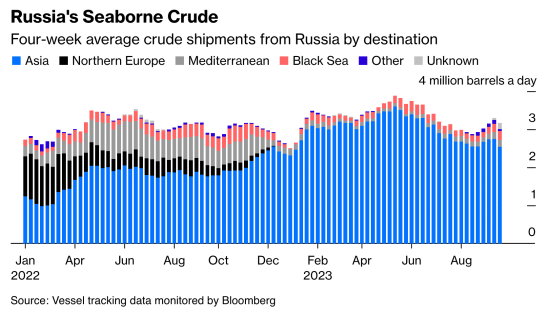

The result is that there is no enforcement of the cap. About 40% of vessels lifting crude from Russia’s Baltic and Black Sea ports were owned by companies based in countries signed up to the cap. A large number also still have insurance routed through London.

Revising the price cap to a level closer to market prices might leave some cargoes trading below the new limit, but it would do nothing to restrict the Kremlin’s income. Improving enforcement and banning rusty old ships would alleviate the risk of an oil spill, but there seems to be no appetite for anything that might hamper Russian oil flow.

With crude trading near $95 a barrel, up about 27% since the end of June, that’s no surprise.

Scrapping the cap would make no difference to the amount of Russian crude on the market — it would flow just as it has done throughout the war in Ukraine. With sufficient ships already available to carry all that oil, it’s unlikely it would make any difference to the price either. What it would affect is the quality of the vessels being used to haul the oil and who’s earning the fees for doing it.

The oldest tankers now engaged in the Russian trade would then likely end up on the beaches of Bangladesh, India and Pakistan, where they would be cut up for scrap, averting what seems like an inevitable environmental disaster the longer they continue to haul crude halfway around the world.

Better still, if Russia has already paid billions of dollars for those old ships, it would become a wasted expenditure.

Vir: Bloomberg

You must be logged in to post a comment.