Martin Wolf, glavni ekonomski komentator v Financial Timesu:

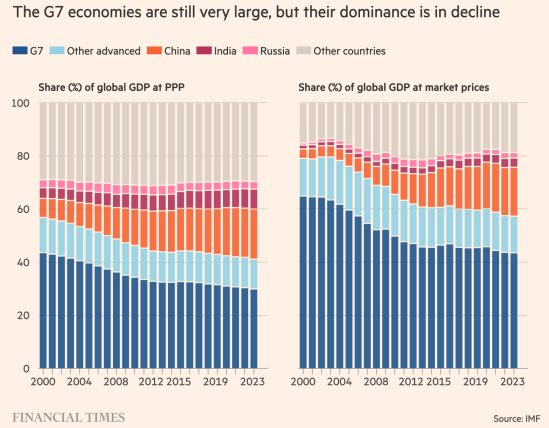

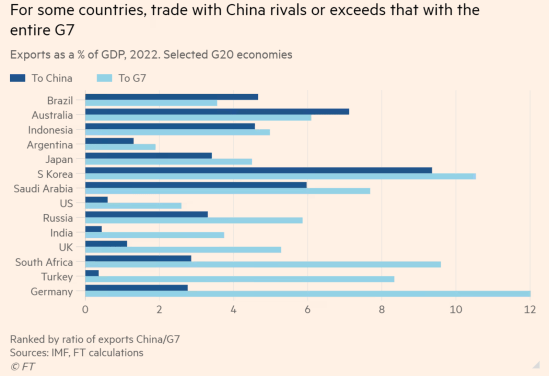

Moreover, both the “unipolar” moment of the US and the economic dominance of the G7 are history. True, the latter is still the most powerful and cohesive economic bloc in the world. It continues, for example, to produce all the world’s leading reserve currencies. Yet, between 2000 and 2023, its share in global output (at purchasing power) will have fallen from 44 to 30 per cent, while that of all high-income countries will have fallen from 57 to 41 per cent. Meanwhile, China’s share will have risen from 7 to 19 per cent. China is now an economic superpower. Via its Belt and Road Initiative it has become a huge investor in (and creditor of) developing countries, though, predictably, it is having to deal with the consequent bad debts so familiar to G7 countries. For some emerging and developing countries, China is a more important economic partner than the G7: Brazil is one example. President Luiz Inácio Lula da Silva may have attended the G7, but he cannot sensibly ignore China’s heft.

The G7 are also reaching out to others: their meeting in Japan included India, Brazil, Indonesia, Vietnam, Australia and South Korea. But 19 countries have apparently applied to join the Brics, which already include Brazil, Russia, India, China and South Africa. When Jim O’Neill invented the idea of the Brics back in 2001, he thought this would be an economically relevant category. I thought the Brics would be about just China and India. Economically, that was right. But the Brics now seem to be on the way to being a relevant worldwide grouping. Clearly, what brings its members together is the desire not to be dependent on the whims of the US and its close allies, who have dominated the world for the past two centuries. How long, after all, can (or, for that matter, should) the G7, with 10 per cent of the world’s population, continue to do so?

…

If we turn to economics, it is also a good thing that the notion of decoupling, a damaging nonsense, has turned instead into one of “de-risking”. If the latter can be transformed into focused and rational policymaking, that would be even better. But it will be much harder to do this than many now seem to imagine. It makes sense to diversify supplies of energy and vital raw materials and components. But, to take a salient example, just diversifying the supply of advanced chips from Taiwan will be really hard.

…

An even bigger issue is how the global economy is to be managed. Are the IMF and World Bank to be bastions of G7 power in a world increasingly divided? If so, how and when are they going to get the new resources they need to deal with today’s challenges? How, too, will they co-ordinate with organisations that China and its allies are creating? Would it not be better to admit reality and adjust the quotas and shares, to recognise the huge shifts in economic power in the world? China is not going to disappear. Why should we not allow it a bigger say in return for full participation in debt negotiations? Similarly, why should we not reignite the World Trade Organization, in return for China’s recognition that it can no longer expect to be treated as a developing country?

Beyond all this, we must recognise that any talk of “de-risking” that does not focus on the two biggest threats we face — those of war and climate — is to strain at gnats, while swallowing camels. Yes, the G7 must defend its values and its interests. But it cannot run the world, even though the world’s fate will also be that of its members. A path to co-operation must be found, once again.

Vir: Martin Wolf, Financial Times

You must be logged in to post a comment.