Jože Damijan, Jozef Konings, Črt Kostevc and Katja Zajc Kejžar

Spodaj je povzetek naše raziskave Explaining the Low Level of Investment in Slovenia, ki jo je naročila Evropska komisija in smo jo izvedli leta 2021. Evropsko komisijo je zanimalo, zakaj je stopnja investicij v Sloveniji, primerjalno glede na druge EU države, tako drastično upadla po letu 2008. V analizi smo vzroke za upad investicijske stopnje preučevali na treh ravneh: makro, sektorski in na ravni podjetij.

Zame sta ključni dve ugotovitvi: Prvič, stopnja investicij v Sloveniji trendno upada že od konca 1990. let, vendar je ta trend zakril val hiperinvestiranja v času pred finančno krizo (2004-2008). In drugič, v Sloveniji se investicije po finančni krizi niso pobrale navkljub izjemno nizkim obrestnim meram in navkljub pospešitvi gospodarske rasti po 2014 (kar je v nasprotju z ekonomsko teorijo, vendar v skladu s poslovnim obnašanjem podjetij), glavni razlog pa je process razdolževanja podjetij, ki so se preveč zadolžila pred 2008. Seveda pa so še drugi razlogi za upad investicij, med njimi predvsem neugodna gospodarska struktura, ki temelji na proizvodnji in izvozu sestavnih delov, namesto končnih izdelkov z višjo dodano vrednostjo. Oboje se pokaže relevantno na vseh treh ravneh naše analize.

Spodaj je povzetek analize na makro ravni (ugotovitve so vsebinsko enake tudi na bolj razdelani sektorski ravni in ravni podjetij). Upam, da vas ne moti, da je zadeva v angleščini.

Comparative analysis of investment trends in Slovenia versus EU member states

Slovenia experienced several distinct periods of investment activity since gaining independence in the early 1990s. Total investment in Slovenia rose steeply between 1995 and 2004, and speeded up additionally during the pre-GFC boom, only to fall after the outburst of the GFC by almost 40 percent by 2012 and remain depressed at that level until 2016 (Figure 9). After 2016, total investment rebounded and exceeded 2006-investment-levels by 2019. Investment plummeted again with the outbreak of the Covid-19 pandemic in 2020.

Source: SURS

Most strikingly, while after 2016 Slovenia’s investment levels in absolute terms appear to recover from the impact of the GFC, adopting a similar steep upward trend as during the 2005-2008 boom, however, investment relative to GDP remain depressed. The total investment-to-GDP ratio in 2020 lags the 2008 ratio by almost 10 percentage points (19.9 versus 29.4 percent) and lags even the transition-level investment-to-GDP ratio from 1995 by more than 3 percentage points (Figure 9).

A striking picture emerges when comparing the current evolution in Slovenia’s investment gaps to the “old” EU member states (EU-15) and the four most industrialized new EU member states (CEE -4: Czech Republic, Hungary, Poland, Slovakia). The investment gaps are not closing but appear to be persistent notwithstanding the surge in absolute investment and improvements in investment ratios after 2016. In the period 2015-2019, the Slovenian corporate sector invests on average 2.4 and 2.5 percent of GDP less than the corporate sectors in the EU-15 and CEE-4 countries, respectively.

Figure 10: Decomposition of total investment to GDP ratio gap in Slovenia relative to EU-15 and CEE-4 by investment type, 1999-2019 (percentage points)

Note: CEE-4: Czechia, Hungary, Poland, Slovakia. Source: Eurostat

This development suggests that there are structural reasons for the poor investment performance of firms in Slovenia. Given the negative impact of the COVID-19 pandemic on the Slovenian corporate sector reflected also in the decline of absolute investment levels (see Figure 9), the investment gap in Slovenia relative to other EU countries is likely to widen. This may significantly hamper the potential future growth of the Slovenian economy.

Stylized facts on macro determinants of investment

To explore to what extent the selected variables in our model (1) can contribute to explain the declining business investment in Slovenia relative to other European countries, we start by presenting the evolution of the correlation between the investment rate and the key variables of interest in Figures. The overview for the other countries in our sample is provided in the Appendix.

For most countries, gross business investment rates at the aggregate level are highly correlated with the business cycle (captured by the lagged GDP growth). This is particularly true for the period before the GFC, while after 2008 in many countries there is a disconnect between the investment rate and the business cycle (Figure A1 in Appendix). Slovenia (Figure 11a) along with most of the EU new member states from CEE region belong to the latter group suggesting that despite the macroeconomic recovery the investment rate did not pick up after the outbreak of the GFC. At the same time, the gross business investment rate is strongly correlated to lagged corporate liabilities growth in Slovenia (Figure 11b). This indicates that business investment, which in Slovenia is financed predominantly through bank loans, is heavily dependent on firms’ access to finance as well as their financial leverage. Between 2009 and 2016, overall corporate liabilities growth in Slovenia was mainly negative, indicating a process of deleveraging after a big surge in leverage in the pre-GFC boom. This is in line with Figure 5 above which demonstrated a sharp net contraction in bank loans to the corporate sector in Slovenia for six consecutive years between 2011 and 2016. With a few exceptions (such as the Czech Republic, Poland, and Sweden), similarly close correlations of corporate investment to corporate liabilities can also be observed in other European countries (Figure A2 in the Appendix).

Source: Eurostat, ECB.

Macroeconomic theory and all classes of macroeconomic models in the range of early Keynesian (IS-LM) to modern Post-Keynesian models (DSGE) are based on the key premise that corporate investment is a negative function of the interest rate. Companies are believed to respond positively to declines in interest rates and negatively to increases in interest rates. The evidence for the period 2002-2019 for European countries (Figure A3 in the Appendix), however, is at odds with this macroeconomic assumption as there is evidently a positive correlation between gross business investment rate and the lending rates. With the exception of a few countries (Belgium, France, Spain, Sweden and Switzerland), both 1-year and 5-year loan maturity lending rates generally move in the same direction as the gross investment rate.

Hambur and La Cava (2018) confirm similar positive correlations between the investment rate and the cost of borrowing for Australia. However, traditional Keynesian models do predict that in a liquidity trap, ever lower interest rates may have little effect on boosting the levels of investment. This situation has also been observed in the Euro Area and other advanced economies with loose monetary policy over the past decade after the GFC, where central banks had to resort to unconventional measures such as zero lending rates and negative deposit rates to encourage banks to increase lending. In Slovenia, these measures had little effect on boosting investment indicating a deeply depressed investment sentiments, both due to the prolonged economic crisis (until 2014) and the corporate needs for extensive deleveraging after 2008 (Figure 11c).

Business investment is generally driven by business sentiments captured by past profits. This is confirmed for most European countries (Figure A4 in the Appendix) showing a positive correlation between lagged corporate profit rates and investment ratios. In Slovenia, a strong positive correlation between lagged corporate profit rates and the investment rate is observed for the period 1995-2008, while after 2008 there is a disconnect between the two. Despite steadily rising profit rates after 2010, investment rates did not follow suit (Figure 11d).

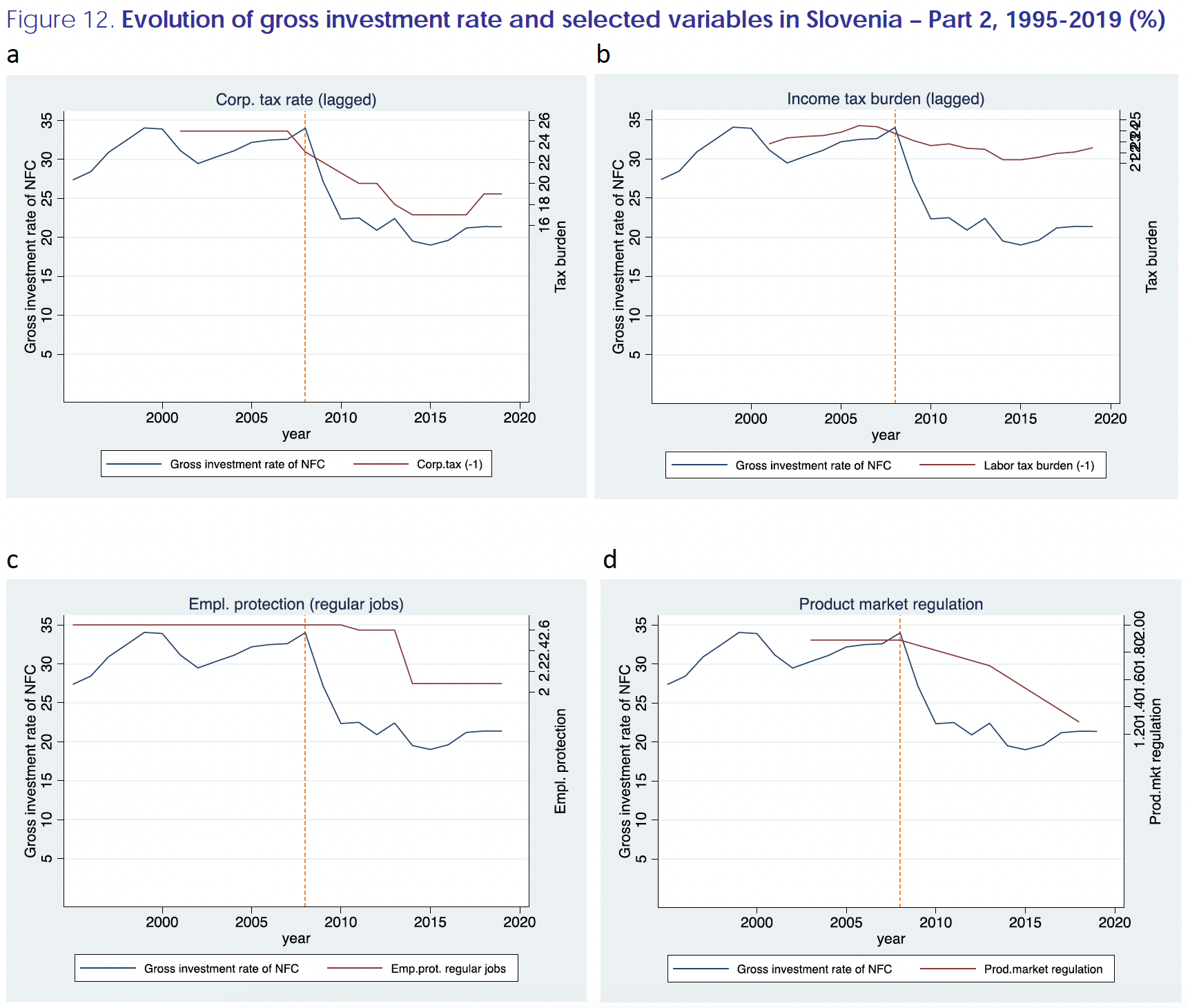

Among the institutional factors, there seems to be no consistent correlation pattern between the corporate tax rate and investment rate across countries. In spite of this, the relationship appears to be positive for most of the countries (see Figure A5 in the Appendix). This is due to the fact that in 2000s most EU countries started to decrease the corporate tax rates, while the investment rate was also declining. The same pattern, but more pronounced, is also observed for Slovenia (Figure 12a). Similar patterns are found also for the correlation between the labor income tax burden and investment rate across countries (see Figure A6 in the Appendix) and an even more pronounced positive correlation in Slovenia (Figure 12b). Hence, neither declining corporate tax rates nor declining labor taxes seem to have helped in reversing the trends of declining corporate investment rates across EU countries and in particular in Slovenia.

Source: Eurostat, OECD.

The same is true for the changes in employment protection legislation for regular full time employment, which was made more flexible after 2010 (Figure 12c), indicating the correlation is going in the opposite direction than expected. A positive correlation between employment protection and investment rates also seems to be a prevailing pattern for other countries (see Figure A7 in the Appendix). This implies that more flexible labor markets do not necessarily boost investment. A very similar picture emerges for overall competition and product market regulation. Regulation has improved after 2008, but contrary to expectations it is positively correlated with a declining trend in corporate investment rate (Figure 12d).

Government financed business R&D expenditures and indirect government support through R&D tax incentives also seem to be correlated with investment rate in Slovenia in the “wrong direction”. Both policy measures have been scaled up after 2008 but do not appear to have ended up promoting investment in a significant way (Figures 12e and 12f). For other European countries, the correlations of both variables to the corporate investment rates are mixed (Figure A8 – A9 in the Appendix).

Source: Eurostat, OECD, European Commission.

In terms of available foreign investment funds, both the stock of inward FDI and EU structural and investment funds (as a share of GDP) have been scaled up after 2008 (EU funds only until 2014), but did not seem to promote investment in a significant way (Figures 13a and 13b). This implies that the two policy measures were expanded but were not strong enough to offset other negative effects on the investment rate.

The share of information and communication technologies capital in total capital invested (ICT share) in Slovenia is steadily declining since early 2000s, notwithstanding that the overall investment rate was showing an upward trend prior to the GFC (Figure 14a). Evidence for other European countries is mixed (Figure A9 in the Appendix).

The Slovenian economy is heavily dependent on exports, which represent about 38% of GDP in value added terms. In the period until 2012, domestic value added as a share of gross exports steadily decreased (by 4 percentage points) but gained momentum afterwards (Figure 14b). According to the Global Value Chain Development Report 2019 (WTO, OECD, WB, IDE-JETRO, UIBE, 2019), the Slovenian economy is one of the 8 most integrated OECD economies into global value chains (GVCs) in terms of both backward and forward integration. However, the composition of exports is deteriorating. Figures 14c and 14d demonstrate an increasing share of intermediate goods’ exports (an increase of 5 percentage points) in the period 2000-2015 and a declining share of final consumption products in exports (a decrease by 6 percentage points). This indicates a structural shift in Slovenian exports away from final goods to intermediate products where markups are traditionally tighter, but also where the need for investing both in R&D and break-through technologies are lower. Hence, this shift in the composition of Slovenian exports could also be contributing to a declining trend of business investment.

Source: Eurostat, OECD.

Macro determinants of declining business investment in Slovenia

Based on the above historical comparative analysis of the investment climate in Slovenia and the EU, we conduct an econometric empirical study on the importance of various determinants of business investment in Slovenia in this section. In line with the recent literature, we model macroeconomic corporate investment as a function of standard macroeconomic determinants of investment, such as:

- GDP growth (capturing the demand factor via business cycle),

- lending interest rate (1-year and 5-year loan maturity),

- profitability of non-financial corporations,

- financial liabilities of non-financial corporations,

- availability of foreign funds (such as foreign direct investment and EU funds),

- use of ICT capital,

- composition of international trade, and

- institutional factors.

Institutional factors that we consider are the following:

- Corporate tax rate and average labor tax burden (income tax + social contributions),

- Overall competition and market regulation (in Slovenia: favouring indigenous firms and leading to significant barriers to entry);

- Flexibility of labour market regulation (in Slovenia: deterring new, domestic and foreign, investments);

- Government-financed Business enterprise R&D expenditures (BERD);

- Indirect government support through R&D tax incentives and through subnational R&D tax incentives;

- Other structural reasons leading to the fact that in spite of a robust economic recovery since 2014, the investment intensity does not seem to rebound at all. In particular, we look at the severity of financial crisis after 2008 resulting in prolonged overall corporate deleveraging. In Slovenia, more so than in other countries, this might have led to possible permanent effects due to reduced investment capacity or depressed investment sentiments (so-called hysteresis effect).

Results

Baseline results confirm the findings from the above descriptive analysis, showing that the main drivers of investment across Europe are the business cycle (lagged GDP growth) and corporate leverage (lagged), while investment is perversely related to the variation in bank lending rates (a positive and significant correlation).[1] These factors, including GFC crisis dummy and country fixed effects, can explain more than 70 percent of variation in investment rates across Europe in the past two decades.

While lagged GDP growth generally positively impacts the investment rates in Europe, the estimations show that during the prolonged period of recession and weak growth of 2009-2013, captured by the interaction term with GFC, the impact of the business cycle component as a driver of investment has weakened significantly. During the post-GFC period the business cycle coefficient has decreased in size by about 70 per cent. Note that the reduced impact of the business cycle during the post-GFC period is also characteristic of the Slovenian economy albeit to a lesser degree than in the other European countries (e.g. interaction coefficients in specification (6) between GDP, GFC and SVN).

On the other hand, the results show that the (positive) effect of corporate debt growth on investment dynamics across European countries remained intact also during the post-GFC period. In contrast, the impact of corporate debt on investment dynamics in Slovenia during the post-GFC period has become substantially more pronounced. Depending on the specification in table 1, the coefficient for corporate liabilities growth in Slovenia for the post-GFC period is bigger by a factor between 6 and 17 as compared to other European countries. Note that as the aggregate investment rate and corporate debt dynamics were moving in the same direction (declining) during the period 2009-2013, this result indicates the severity of the financial crisis and the importance of corporate sector deleveraging for investment potential and/or willingness to invest. Overleveraged firms were forced to deleverage, while also for financially sound companies access to credit during the financial crisis has deteriorated, limiting potential to invest for both groups of firms.

Our findings for Slovenia suggest that the drop in investment is driven by a lower sensitivity of corporate investment to the business cycle and a higher deleveraging process of highly leveraged firms. This raises two relevant questions. Firstly, why did investment drop that much in the first place before deleveraging took place, if it is not sensitive to the business cycle? Secondly, why investment did not recover when deleveraging ‘faded out’ in recent years?

More detailed explanation of this finding is as follows:

- Investment drop in Slovenia happened immediately after the start of GFC due to negative economic shock. There are two key issues to be taken in to account: First, the volume of investment and the investment rate were abnormally high in the boom period 2005-2008, hence the drop in investment after the boom was over was inevitable. Second, investment is part of the GDP (about 20%) and hence in 2009 GDP in Slovenia fell by 7.5% also due to a big drop in corporate investment following the drop in final demand (domestic and foreign)).

- The above implies that the external shock of the GFC turned an “overshooting” of investment into an “undershooting”, which was then reinforced by the corporate deleveraging process.

- Lower sensitivity of corporate investment to the business cycle applies to the whole post-crisis period which is picked up by the interaction term with the GFC dummy variable (i.e. 2009-2013) and in particular for the latter part of this period. While Slovenia’s GDP recovered briefly and marginally in 2010-2012, investment did not pick up as corporate deleveraging began. In 2012-2013, the Slovenian economy slipped into the next recession (double-dip). The process of deleveraging dragged on until after the bank restructuring at the end of 2013. For most of the over-indebted companies, this process lasted until 2015 or 2016. Although economic growth resumed in 2014, most companies were still in the middle of the deleveraging process due to the delayed bank restructuring.

____________

Celotna raziskava je objavljena v Damijan J., J. Konings, Č. Kostevc & K. Zajc Kejžar (2022). Explaining the Low Level of Investment in Slovenia. European Economy Discussion paper 169, July 2022.

[1] Results for 5-year interest rates show that this positive correlation between interest rates and investment rate is very robust.

* Vse reference na slike se nanašajo na originalno številčenje v študiji.

You must be logged in to post a comment.