Kot dodatek moji današnji kolumni v Dnevniku o inflacijski paniki, je spodaj dobra nit Vitorja Constancia (podpredsednika ECB 2010-2018 in pred tem guvernerja portugalske centralne banke 2000-2010) o empirični (ne)pomembnosti inflacijskih pričakovanj. Inflacijska pričakovanja so bila ad hoc prevzeta v makroekonomske modele, brez da bi za njihov dejanski pomen obstajala kakšna empirična podpora (Phelps (1967) in Friedman (1968) sta jih vključila zgolj na podlagi svojih “a priori predpostavk“, ostali pa so jih nato vzeli kot suho zlato in nihče jih ni več osporaval).

No, do Ruddovega paperja (FED) letos septembra, ki je razgalil, da za pomen inflacijskih pričakovanj pri napovedovaanju bodoče inflacije ni relevantne teoretične in empirične podpore. Podobno kaže novi working paper ECB, ki poizkuša izkristalizirati, kateri indikatorji inflacijskih pričakovanj bi lahko bili relevantni, pri čemer pa se pokaže, da so razlike v napakah pri napovedi bodoče inflacije z ali brez upoštevanja inflacijskih pričakovanj v modelih ekstremno majhne (“The gains in forecast accuracy from incorporating inflation expectations are typically not large”). Preprosto povedano, ko centralne banke spremljajo “izmerjena” inflacijska pričakovanja za 1, 2, 3 ali 5 let vnaprej, ne dobijo s tem nobene pomembne informacijske vrednosti.

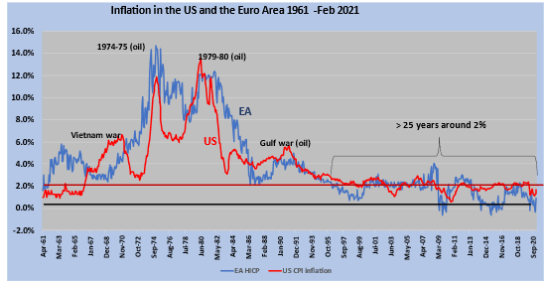

Inflacija ima svojo dinamiko in zadnjih 25 let je v razvitih državah stabilna na ravni okrog 2%. Edini šoki v zadnjih 60 letih v inflaciji so bili posledica šokov v cenah energentov ali vojn, medtem ko od konca 1960.-ih let naprej ni nobene empirične podpore, da bi se stroški dela prenašali naprej v cene proizvodov in storitev (inflacijo). Tudi v 1970.-ih letih, ko je bila inflacija res visoka, te stroškovno-inflacijske spirale ni mogoče empirično potrditi (glejte mojo kolumno).

Torej, kdaj bodo centralne banke prenehale s tem pretvarjanjem, da je namen njihovih monetarnih ukrepov v tem, da “trdno zasidrajo inflacijska pričakovanja“?

The ECB just published a relevant working paper about which inflation expectations indicators are the best to help forecast inflation ecb.europa.eu/pub/pdf/scpwps…

J, Rudd, in a FED WP asked “Why Do…Inflation Expectations Matter for Inflation?”, federalreserve.gov/econres/feds/f… 1/18

Rudd points that the role of inflation expectations as a cause of inflation has been accepted as “an established truth” since Phelps (1967) & Friedman (1968) introduced them with “a priori assumptions”. Since then, there was hardly a debate on why that causality should work 2/

Expectations became almost everything. From the classic 2003 book by Woodford “Interest and Prices”: “..successful monetary policy is not so much a matter of effective control of..interest rates as it is of shaping market expectations..” “…very little else matters” 3/

Rudd points that the arguments of Phelps & Friedman assumed the absence of money illusion by workers and firms when they negotiated wages. Friedman also assumed that workers targeted expected future real wages, and there was a timing mismatch w/ firms´ expectations 4/

Expectations were then related to collective wage negotiations between trade unions & firms, assuming they could cause wage-price spirals stemming from accelerating expectations. This assumption was perhaps warranted in the 60s w/ trade unions still relevant. No longer.. 5/

After the early 70s oil shocks, there are no signs in advanced countries of wage-price spirals feeding inflation. That is one fact behind the stable inflation around 2% in the last 25 years. The chart shows that inflation spikes were in the past due mostly to oil & war shocks 7/

Expectations stayed in models to forecast inflation without reference to which agents they belonged and the mechanism that made them relevant for pricing decisions. Expectations by firms should, in principle, matter but not those by households or financial markets. 8/

Still, surveys of firms for the US in 98 & the EA in 2005 about price decisions didn´t find a role for expectations of future inflation: Blinder et al. (98)“Asking for prices” & ecb.europa.eu/pub/pdf/scpwps… In the EA, a majority of firms used cost/mark-up to decide prices 9/

Still. surveys of firms´s inflation expectations are not good. For the US, the Atlanta FED survey on firms’ expectations of their own costs, not inflation, and for the EA, the Commission survey is on qualitative expectations of firms´ selling prices ec.europa.eu/economy_financ…

When so-called new Keynesian models with rational expectations (DSGE) appeared, they included a new Phillips curve w/ forward-looking expectations and the output gap. Expectations were made endogenous, but the early model versions didn´t forecast well 11/

So, pure ad-hoc changes were made to include inertia (past inflation) and import prices. Later, Coibion & Gorodnichenko (2012,2015) started the use of expectations from household surveys in hybrid Phillips curves. How those would cause inflation? 12/

The same authors promoted, in 2018, a survey about firms´ inflation expectations (ftp.iza.org/dp14378.pdf ). With more data, we will see its econometric usefulness. There are, then, many approaches to expectations as causing inflation 13/

The quoted ECB new WP tries to determine which expectations better contribute to inflation forecasting: households, financial markets, firms or professional forecasters. Many models (ADLs, Phillips curves, BVARS) are estimated with/without expectations & data 2001-19 14/

The quoted ECB new WP tries to determine which expectations better contribute to inflation forecasting: households, financial markets, firms or professional forecasters. Many models (ADLs, Phillips curves, BVARS) are estimated with/without expectations & data 2001-19 14/

“The gains in forecast accuracy from incorporating inflation expectations are typically not large”, but the Survey of Professional Forecasters (or Consensus) gives the highest contribution. Models “do not improve” w/expectations from households, firms or financial markets 15/

The EU Commission surveys of households and firms inflation expectations were used, and they only give qualitative indicators in terms of “balances” between positive and negative answers. Better surveys would be needed for the exercise. 16/

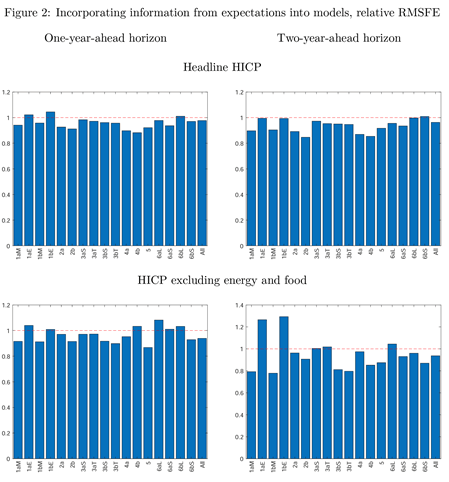

The chart below shows the out-of-sample ratio of RMS Forecast Error for the models with/without different expectations. Most outcomes are below but very close to 1, showing that the improvement from including expectations is indeed small. 17/

Professional Forecasters’ expectations won the model contest, but what do they represent, and why do they influence price decisions in an economy dominated by monopolistic competition where firms have some pricing power? Rudd’s paper raised a worthwhile debate. 18/18

Vir: Vitor Constancio, Twitter

You must be logged in to post a comment.