Luis Garicano (London School of Economics) kritično komentira nov članek Sanderja Tordoirja in Brada Setserja (How German industry can survive the second China shock), v katerem predlagata, da Nemčija in države EU nasploh uporabijo paleto mehanizmov za zaščito avtomobilske industrije. Predlagala sta program “Kupuj evropsko”, kompleksen sistem zaščitnih mehanizmov, v okviru katerih bi prek uveljavljanja socialnih in okoljskih standardov izločili kitajske dobavitelje in proizvajalce končnih izdelkov ter tako naredili zaščiten prostor za razvoj evropske industrije. Garicano pravi, da je to brez veze, da je to Nemčija z obilnimi subvencijami že preizkusila od leta 2010 naprej na področju solarnih panelov in baterij, pa so vsa velika evropska podjetja navkljub subvencijam propadla. Namesto tega Garicano predlaga, da Evropa opusti tradicionalne panoge, kjer so novi programi (električni avtomobili, zelene tehnologije) že izgubili bitko s kitajskimi proizvajalci (in naj zaradi višjih cen evropskih izdelkov v primeru uvozne zaščite ne ogrozi ciljev razogljičenja) in se raje posveti področjem, kjer še ima primerjalne prednosti (proizvodnja specialnih orodij itd.) ali kjer lahko naredi inovativni napredek (morda na področju umetne inteligence).

Garicano ima prav, da je bitka pri električnih avtomobilih za Evropo izgubljena in da nima smisla tukaj zapenjati in vlagati ogromnih količin sredstev v luknjo brez možnosti uspeha. Problem pa je, da Evropa razen tradicionalne industrije in storitev nima nič drugega, kajti zanašala se je samo na obstoječo strukturo gospodarstva in ni razvijala nič novega. Pri kateri od ključnih tehnologij prihodnosti so evropske države oziroma njihovi znanstveniki in razvojniki sploh špica v svetu? Večkrat sem že citiral avstralski ASPI Critical Technologt Tracker, ki kaže, da pri 64 ključnih tehnologijah prihodnosti ni nobene evropske države med prvimi dvemi državami (Kitajska je prva pri 57 tehnologijah, ZDA pa pri 7).

Torej kaj še ostane Evropi (razen podpiranja nadaljevanja vojne v Ukrajini in kupovanja 4-krat dražjega ameriškega plina do bridkega konca)?

____________

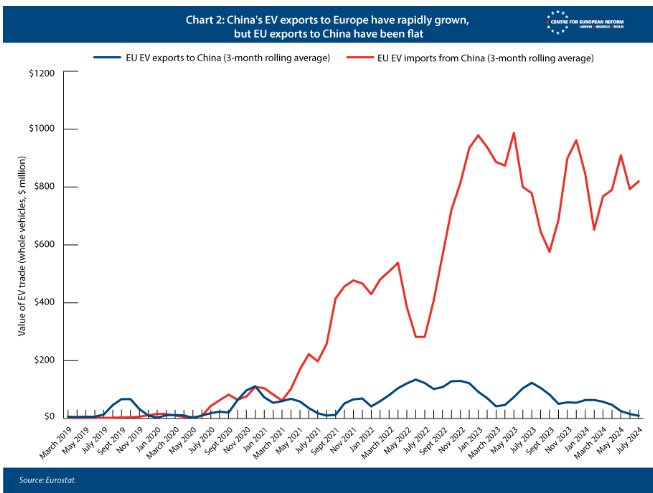

Sander Tordoir and Brad Setser just released a new CER policy brief. I strongly recommend that our European readers read it. It diagnoses well the grave challenge facing the German industry. German industrial production has declined for five years, China now exports 5 million more vehicles than it imports while German net exports have halved, and Chinese firms dominate emerging sectors like electric vehicles and solar panels. The second China shock is here, and it will be much worse for Europe than the first.

“The EU, with Germany at its industrial core, boasts 30 million manufacturing jobs: almost twice as many as the US had before the first China shock.”

China’s manufacturing dominance is nearing unique levels in history:

“China’s manufacturing surplus is now 10 per cent of its GDP – a staggering number… US trade surpluses in manufactured goods peaked at 6 per cent of American output early in World War I”

They are right to argue that this will force a dramatic restructuring of our industrial base. However the brief prescribes the wrong medicine.

Tordoir and Setser’s Proposals

Some of what Tordoir and Setser argue is uncontroversial. They are right that solid numbers on China’s trade surplus from the IMF are essential. I agree that Germany needs to rely on Chinese supply when efficient, it needs to stand with its allies, it needs to impose trade measures when and if China’s sectoral subsidies have distorted competition:

Where I part company with them is in their third and fourth recommendations. The third is their ”Buy European” provisions. These paragraphs give you a flavour of how crazy it can get :

One possible lever to enforce such criteria across the EU would be competition policy: the Commission’s enforcers could condition approval of national subsidy schemes on criteria that favour EU production, such as adherence to social standards, and exclude products associated with high emissions from long-distance transportation or coal-intensive production processes.

There may, however, be sectors like non-greentech machine-building or energy-intensive chemical production where existing EU regulations (like the NZIA) or product standards (such as the ESPR) provide insufficient hooks to do so. The EU could then pass new directives to co-ordinate subsidies. Unlike an EU regulation, an EU directive is a legislative act that sets out a goal all member-states must achieve, but allows them to decide how to transpose it into their national laws.

They enumerate a whole list of other complex, specific rules based on distance, social and environmental standards to make it de facto a rule to “buy European”. I would call this proposal (if the readers excuse the lack of decorum) a call for an increasing the “enshittification” of the Single Market- a continuing process of increasing regulatory complexity that is doing much to make our firms less competitive. Also, these clever rules will create all sorts of trouble with our friends in the US, Japan, Korea, Brazil, and South Africa. This is the path towards European decadence.

The fourth set of measures is doubling down on industrial policy by using the tariff revenue from the China tariffs towards an EU industrial policy fund. I think this gets it wrong by making it appear as if Germany (and Europe) has simply not attempted industrial policy. In fact the two examples where China is delivering its biggest blows are two where Europe, and Germany, did try.

In the early 2000s, Germany was first with solar subsidies that created the world’s largest solar market.

“In 2010, Chinese production of solar Photovoltaic (PV) panels depended on imported German equipment. Now solar PV production globally relies on equipment imported from China.”

These subsidies helped build a substantial European solar manufacturing industry. By 2012, European firms like Q-Cells, Solarworld, and Centrotherm were global leaders. Yet despite these advantages and continued trade protection, the European solar industry collapsed. Q-Cells went bankrupt in 2012, SolarWorld followed in 2017, and today China controls over 80% of every step in the solar supply chain and produces at half the cost of non-Chinese producers. This happened despite aggressive EU anti-dumping tariffs on Chinese panels in 2013 — exactly the kind of trade defense Tordoir and Setser now advocate.

European governments have poured billions into EV development and production: Germany provided €5 billion in EV purchase subsidies between 2016-2023; the big hope for EU batteries, Northvolt, just went bankrupt despite large EU and German subsidies.

Yet despite this massive support, Chinese EVs are now one generation ahead in technology — superior in range, charging speed, and software integration — and significantly cheaper to produce.

The issue isn’t that Europe didn’t try hard enough — it’s that the fundamental conditions for successful industrial policy, as discussed previously in Silicon Continent, are absent in Europe’s automotive sector:

Europe’s auto industry is dominated by powerful legacy producers and unions who fiercely resist change. Unlike South Korea in the 1960s or China in the early 2000s, where there were few entrenched interests to oppose transformation, Europe’s industrial system prioritizes protecting existing jobs and companies.

European industrial policy suffers from competing and often contradictory goals. Should it prioritize climate change (suggesting openness to Chinese EVs to accelerate adoption), protect jobs (favoring trade barriers), ensure technological sovereignty, or maintain competitiveness? This confusion has led to halfway measures – tariffs too low to protect the industry but high enough to slow the green transition.

The EV transition represents a classic case of disruptive innovation where incumbents struggle to adapt and survive. Just as Kodak couldn’t adapt to digital photography, traditional automakers face fierce internal resistance to fully embracing electric vehicles. More worryingly, Europe has failed to produce new EV-native companies like Tesla, Rivian, or BYD.

Doubling down in these areas will mean throwing good money after bad. Europe has lost on wind, solar, and batteries. There are gigantic learning curves, and Chinese firms are way ahead. If we care about climate change, we fortunately have cheaper and cheaper solar, wind, and batteries. Europe’s scarce resources should be used in the most productive way possible: areas where competitive advantage is still possible — complex industrial machinery, specialized chemicals, and high-end engineering where German firms still lead.

For policymakers: please stop regulating the industries that remain to death. We are here wringing our hands at how we lost solar panels while doing everything in our power to lose in AI. Europe needs to be the most innovative continent. Where are the new EV companies from Germany?

I don’t want to minimize the serious challenge the German industry faces. The potential loss of high-wage manufacturing jobs could devastate communities. But the solution isn’t to repeat failed industrial policies with higher spending and stronger trade barriers.

Postcript: I wake up today to news in the Financial Times that European carmakers will have to pay billions in credits to Chinese electric vehicle manufacturers. While we are supposedly trying desperately to save our car industry, we are creating distorted fleet-wide quotas. This makes no sense. We should focus on removing harmful policies rather than dreaming up fancy new bureaucratic schemes.

Iluzorno je iskati panogo, kjer je Evropa sploh še bolj inovativna od Kitajske. Glede na to, da imajo na Kitajskem samovozeče taksije brez voznika in da moj kitajski zvonec s kamero za 150 € prepozna obraze ne samo tistih, ki pozvonijo, ampak vseh mimoidočih in če jih pozna napiše ime človeka v aplikaciji, tudi pri AI Evropa nima možnosti. Prej sem imel dve leti francoski podoben pameten zvonček in niti približno ni znal česa podobnega, pa tudi kvaliteta celotnega produkta je bila dosti slabša. Ampak enako stanje je praktično povsod, pa naj bo to Renault, Mercedes, sončne celice in verjetno kmalu tudi medicinska oprema. Enostavno bo treba malo več napora pri evropskih podjetjih ali protekcionizem ali bo pa kmalu popolnoma vse tehnično prišlo iz Kitajske. Ampak glede na to, da imajo popolnoma enak problem Američani, bo Evropa pač uporabila ameriško rešitev problema, verjetno v malo blažji obliki. Ali pa bo Kitajska morala dovoliti, da bodo tuja podjetja lahko postala večinski lastnik pomembnih kitajskih podjetij.

Iluzorno je iskati panogo, kjer je Evropa sploh še bolj inovativna od Kitajske. Glede na to, da imajo na Kitajskem samovozeče taksije brez voznika in da moj kitajski zvonec s kamero za 150 € prepozna obraze ne samo tistih, ki pozvonijo, ampak vseh mimoidočih in če jih pozna napiše ime človeka v aplikaciji, tudi pri AI Evropa nima možnosti. Prej sem imel dve leti francoski podoben pameten zvonček in niti približno ni znal česa podobnega, pa tudi kvaliteta celotnega produkta je bila dosti slabša. Ampak enako stanje je praktično povsod, pa naj bo to Renault, Mercedes, sončne celice in verjetno kmalu tudi medicinska oprema. Enostavno bo treba malo več napora pri evropskih podjetjih ali protekcionizem ali bo pa kmalu popolnoma vse tehnično prišlo iz Kitajske. Ampak glede na to, da imajo popolnoma enak problem Američani, bo Evropa pač uporabila ameriško rešitev problema, verjetno v malo blažji obliki. Ali pa bo Kitajska morala dovoliti, da bodo tuja podjetja lahko postala večinski lastnik pomembnih kitajskih podjetij.

Všeč mi jeVšeč mi je