Kitajska letno proizvede 31 % vseh globalnih emisij CO2, drugi največji CO2 onesnaževalec so ZDA s 13.6 %, sledita pa Indija in države EU-27 s po 7.5 %. Torej potrebno znižanje globalnih CO2 emisij, da bi preprečili segrevanje planeta za več kot 2 stopinji Celzija, lahko efektivno naredi le Kitajska. Vsi ostali igralci so premajhni, da bi imeli bistveni vpliv.

Kitajska se glede tega močno angažira, tudi s politiko ničelnih emisij do leta 2060, vprašanje pa je, če bo to zadostovalo za zaustavitev rasti globalnih temperatur. Spodaj je dober prispevek Adama Toozeja na to temo.

The escalating climate crisis will be driven by natural mechanisms and tipping pionts, whose effects we are now seeing every day. Business decisions and technological developments are crucial. But insofar as policy matters, and it does, it is China’s policy that matters most, no longer that of the USA or the EU. Time is running out. If we are serious about stabilization by mid-century, decisions have to be made now to significantly accelerate the pace of decarbonization worldwide.

As Lauri Myllyvirta has highlighted in a recent blogpost on the timetable set by the Paris accords, to which China has subscribed since 2015, Beijing is approaching a decision point. Xi Jinping’s momentous decision in 2020 to announce the goal of carbon neutrality by 2060 now needs to be given teeth. By next year Beijing’s policy-makers must chart a national decarbonization path for the next decade. This can either set China, and thus a huge part of the world economy, on the path to rapid energy transition, or it may spell disaster.

The good news is that given China’s huge recent surge in renewable investment, on its current trajectory, rapid decarbonization compatible with stabilization around 2 degrees of warming is not out of reach. If, on the other hand, Beijing chooses not to double down on this momentum and opts, instead, for what may seem like a more “prudent path”, it will undermine the credibility of the green transition, slow the pace of change and store up even bigger problems for the future. A hugely promising avenue for Chinese development will be blocked. And the planet will be en route to massive heating.

If this sounds dramatic, I make no apology. In the next 12 months there are two crucial cliffhangers in global climate policy. The one that will hog all the attention in the West is the American election on November 5 2024. The one that matters more is Beijing’s decision on the next phase of its decarbonization program.

Since the mid-2000s, China’s huge emissions have made it into the decisive force in the global climate equation. Of course, the historic emissions of the West are disproportionately larger. From that follows an inescapable responsibility for the West and in particular the USA to do far, far more than it does.

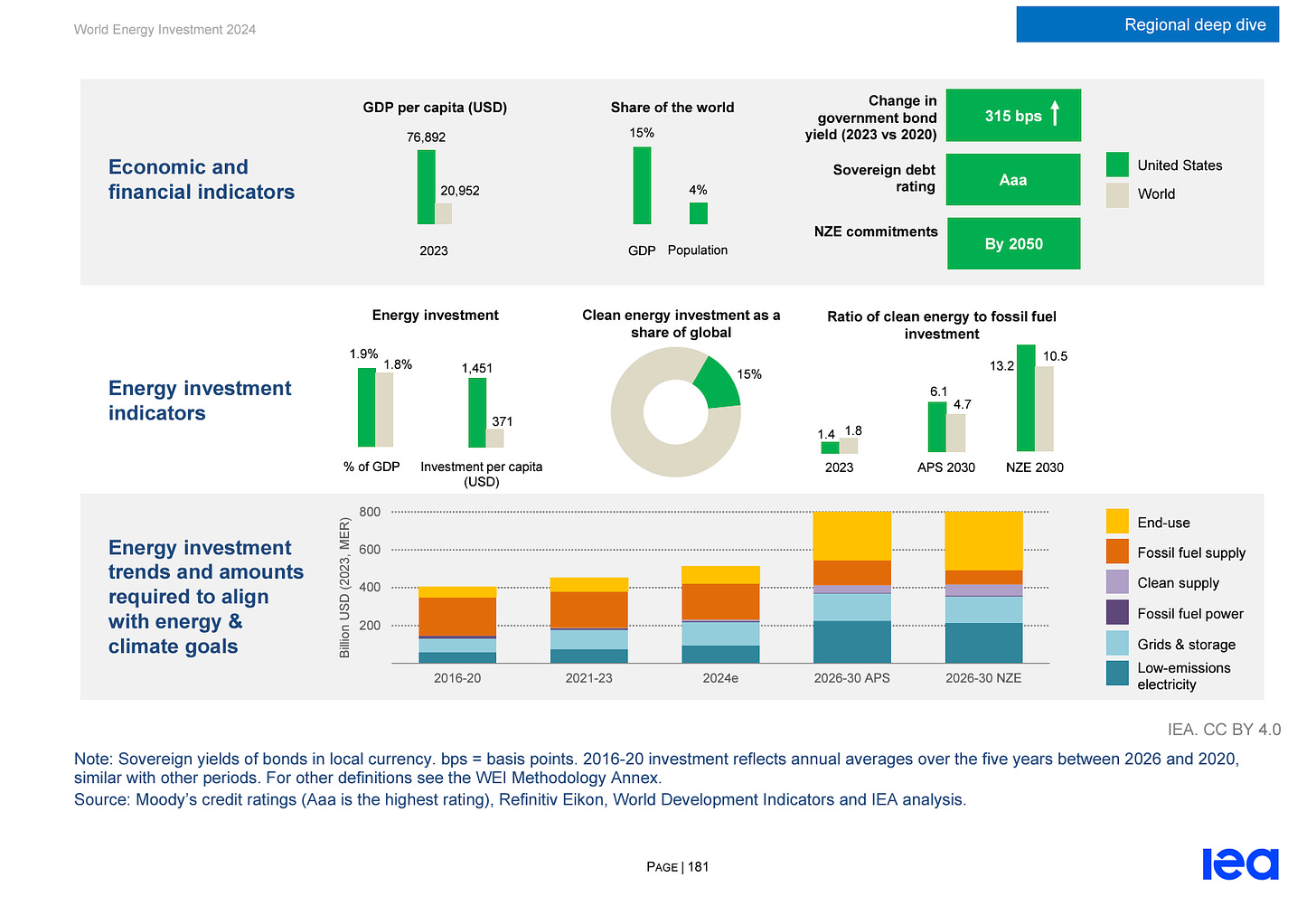

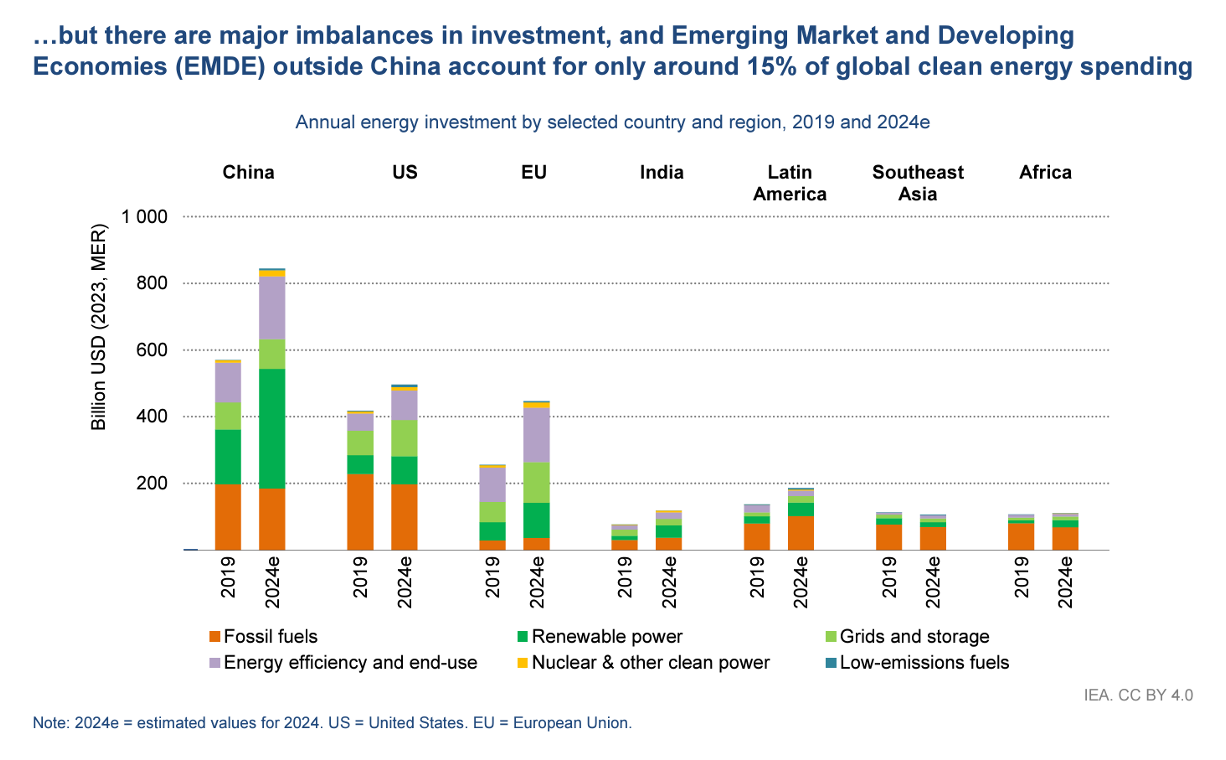

Despite all the hype around Bidenomics, as the latest data from the IEA on energy investment show, the USA is far from being a “climate leader”. Relative to GDP, emissions and climate goals, the pace of renewable investment in the USA is modest. US business interests, with the active encouragement of the Biden administration, are major investors in oil and gas expansion. The IEA is diplomatic, but this is the message from its latest report:

Given its unusually heavy energy consumption, to conform to any kind of stabilization path the US needs to even further raise its basic investment in clean energy and multiply its downstream spending on electric vehicles and heat pumps. At the same time, it must slash its new investment in fossils. Those messages are still very hard to convey in American politics.

The historic playing field for the rest of the world is not level. But we cannot shape the future by undoing history, at least not until we develop massive carbon capture technologies. The only way we can shape the future is to shape emissions in the present and in years to come. And this means that China is decisive.

With a share of global emissions in excess of 30 percent, the world’s largest coal-based energy sector, average per capita emissions higher than those in most European countries and a large, super-polluting elite, China’s policy choices matter at the global level. And they matter not only for China. China’s cheap green technology and its overseas investment are crucial for the trajectory of decarbonization worldwide.

The good news is that, as confirmed by the most recent IEA energy investment report, the development of China’s renewable energy sector is by far the most dynamic in the world.

Though it may be symptoms of deep political-economy imbalances, China’s overall investment rate of 43 percent of GDP (2023) gives it huge scope for action. The climate problem is urgent and requires nothing more than huge investment. Though tumbling out of one paradigm of heavy industrial and infrastructure investment into a new one of investing in renewable energy, may be a symptom of the same underlying macro imbalances, the green areas offer huge room for China’s resources to be put to good use. In green energy, China and the rest of the world are far from from reaching the point of diminishing returns that made the old heavy industrial paradigm increasingly inefficient and counter-productive. And China has a long and difficult rode ahead.

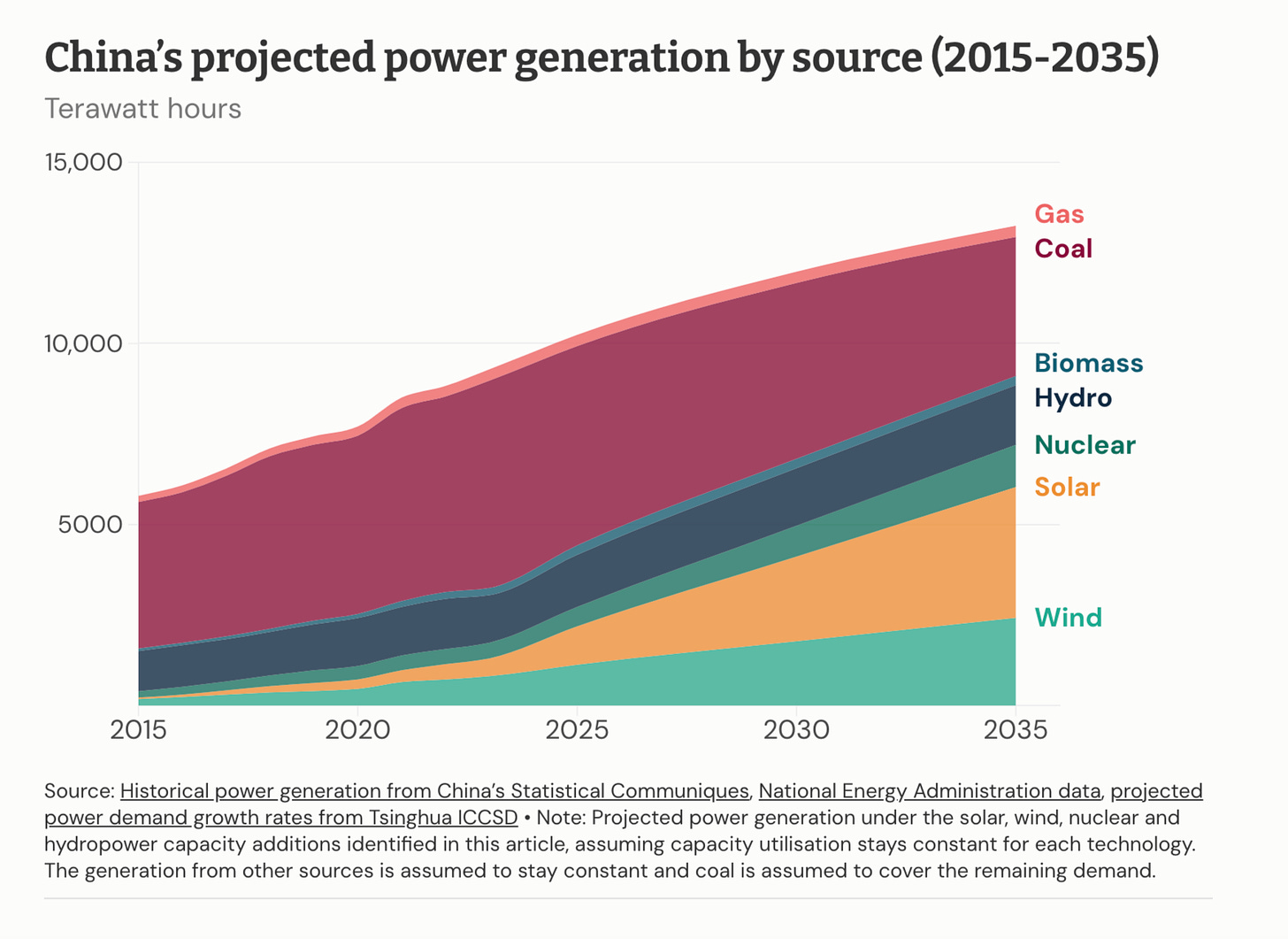

Though the pace of China’s solar and wind expansion are extraordinary, the share of Chinese electricity generated by the new renewables is still modest compared to the levels reached in large economies like Germany or the most advanced American states, such as California.

On the green energy transition, the continuity of CCP-rule and the high profile commitment of Xi Jinping to neutrality by 2060, provide a relatively stable environment for green investment. This differentiates China from the USA, where the elections may hand the Presidency to Donald Trump by the end of the year.

But China has its own problems and its own political dilemmas. Even if the framework of China’s climate policy seems comparatively robust, Beijing has huge, complex and difficult decisions to make. The energy transition for China is daunting. Far larger than anything contemplated in the West. This graph captures in stylized form the comparative scale of the challenge facing Beijing. It is a recurring feature in these newsletters because it will define world history for decades to come.

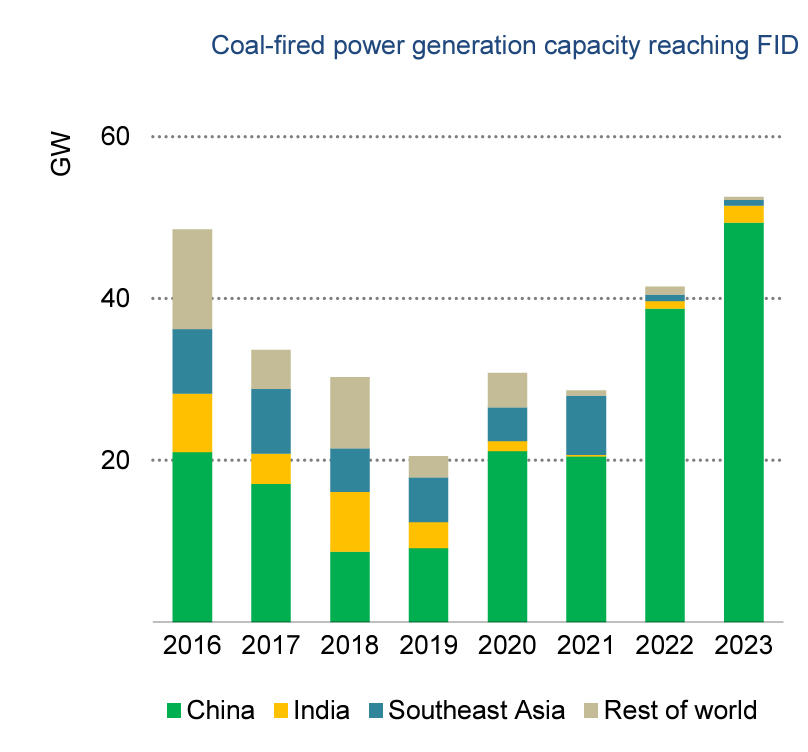

China has a giant coal interest and worldwide China is the only significant new investor in coal.

Source: IEA

The trump card of China’s domestic coal lobby is the concern for security of energy supply, both with regard to the domestic balance of domestic supply and demand, and a possible interruption of energy imports. During the energy crisis in China of 2021-2022, “coal came to the rescue”.

But, China now faces a crucial juncture. The momentum of its green energy build out is dramatic. PV, wind, batteries and EV have all hit a new pace of expansion. The transmission grid is expanding to keep pace. In the next 12 months Beijing has to decide whether it will underwrite that historic shift by committing to an ambitious path of further investment under the Paris Agreement, or whether it will shrink back to a more cautious path.

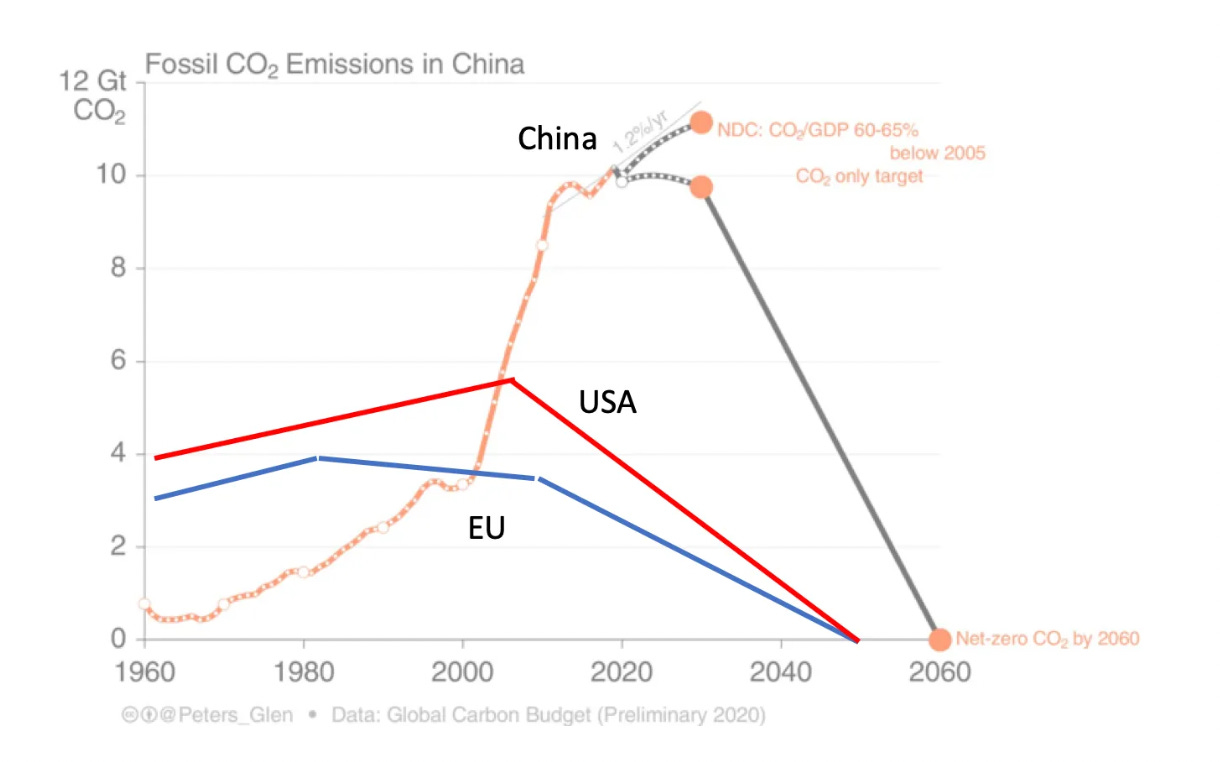

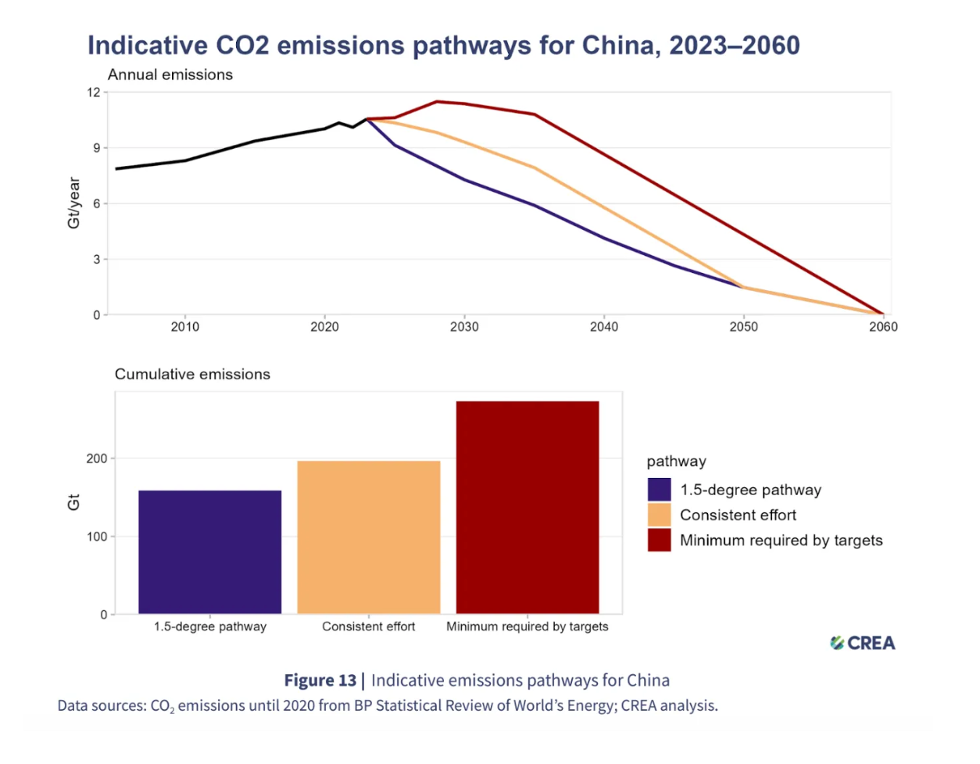

As was highlighted in Chartbook Carbon Note 11, as far as the global climate balance is concerned, everything depends on path that China chooses. And time counts. A decision delayed now cannot be retrieved in the few decades left. If China chooses to meet its 2060 neutrality goal with a last-minute effort – even if that is plausible – it significantly constrains the room for global stabilization. The graph below spells out the trade offs.

For neutrality by 2060, there is no escaping the fact that China must at some point take a hairpin bend the question is when and on what terms. If China were to make a crash effort between 2023 and 2060 to achieve 1.5 degree conformity, cumulative emissions would be 160. The “consistent” effort path yields, 200 Gt in cumulative emissions and the “minimum effort” path implies 270 Gt of cumulative emissions. Comparing those numbers to China’s current emissions of c. 11 Gt per annum gives an idea of how demanding all of these trajectories are.

The impact on the global balance is huge. This is where the “community of common future” so often invoked by the Chinese leadership gets real. If we rule out stabilization at 1.5 degrees as no longer realistic, then for a two-thirds chance of stabilizing at 2 degrees we have 940 Gt remaining. Assuming it actually meets the objective of neutrality by 2060, the path Beijing chooses will determine whether it claims 17 percent or 29 percent of that total. Either way, it changes the climate outlook for the entire planet.

Furthermore, it is not just the final balance but the means of getting there that matter. A slower transition may seem easier, but that may be an illusion, because it lacks credibility. It sends a less powerful signal as to the direction of travel. By contrast, a faster transition generates momentum. It makes future decisions easier, not harder. It encourages business investment and technological development around the path of advance.

The question facing Beijing in the next 12 months is what to promise for the next ten years. To give the world a chance of 2 degree stabilization, the climate models suggest that China’s emissions must peak and then decline by c. 30 percent by 2035.

This is fast and more abrupt than any country has previously achieved. But this is what the situation dictates. Delay may seems safer in the short-run, but unless China pivots now, in 2030 or in 2035 China’s leaders will face even more insuperable problems in hitting the goal of carbon neutrality by 2060.

…

China’s remarkably dynamic green energy sector has opened up a new range of possibilities for both China and the world. It has crushed the cost curves for key green energy equipment. That is the fruit of years of China’s policy, entrepreneurship and technological sophistication. Those achievements have come at the cost of labour and capital mobilization. In 2022-2024 we are seeing a historic surge in China’s green energy capacity. Despite their obvious benefits, the West is not welcoming those Chinese goods. The advocates of a new green protectionism argue that keeping Chinese goods out of rich Western markets is essential to maintaining political coalitions behind the green energy transition there. Who knows? We are in uncharted territory and we easily underestimate the interests of consumers of affordable green energy products. Be that as it may, it would be a tragedy if Beijing for its own part failed to capitalize on China’s world-changing surge in green investment, settled for a policy of go-slow and in so doing undercut the dynamism of China’s green energy sector, whose dynamism is our single best hope of climate stabilization.

You must be logged in to post a comment.