Standardna učbeniška makroekonomija uči, da padec v agregatnem povpraševanju povzroči recesijo, v kateri tekoči BDP pade izpod potencialnega glede na dane proizvodne možnosti. Vendar je ta učinek kratkotrajen, saj se z okrevanjem gospodarstvo kmalu vrne k trendu potencialne rasti. Oscilacije BDP naj ne bi prizadele potenciala za rast. Toda Blanchard & Summers sta že leta 1986 pojasnila, da ima lahko trajno visoka brezposelnost dolgoročno negativne učinke na sam potencial za rast. Ta učinek sta imenovala “histereza”. Danes učinek makroekonomske histereze razumemo širše, in sicer kot dolgoročno negativni učinek trajajoče krize na obseg in kvaliteto obeh produkcijskih faktorjev (dela in kapitala). Trajajoča kriza ciklično (kratkotrajno) brezposelnost spreminja v strukturno (dolgoročno), pri čemer gredo v nič znanja in potenciali trajno brezposelnih. Na drugi strani pa zaradi dolge krize trajno izostanejo investicije podjetij. Oboje skupaj pa z vsakim letom podaljševanja krize zmanjšuje potencialno rast BDP.

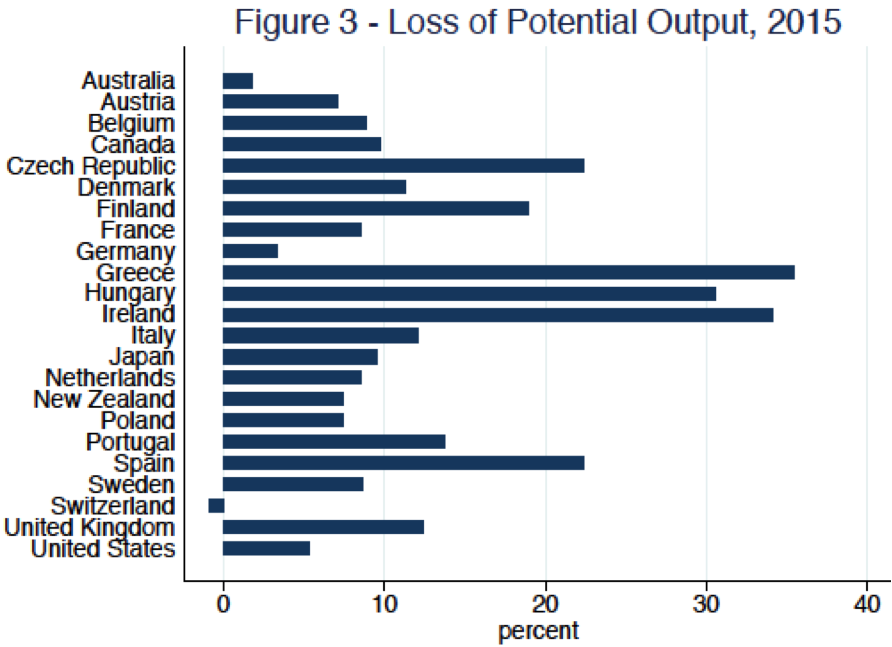

Letos je Ball (2014) okvantificiral učinek histereze sedanje dolge recesije na dolgoročno znižanje potencialne rasti BDP. Primerjal je, kako z vsakim letom podaljševanja krize upada potencial za bodočo rast in ugotovil, da je sedanja kriza med 23 državami OECD glede na leto 2007 v povprečju zmanjšala potencialni BDP za 8.4% (kot da bi kdo izbrisal BDP celotne Nemčije). Pri tem v nekaterih državah ni negativnih učinkov (Avstralija, Švica), medtem ko je v Češki in Španiji učinek histereze zmanjšal potencialni BDP za več kot 20%, v Grčiji, Madžarski in Irski pa za več kot 30% (glejte sliko).

According to textbooks in macroeconomics, a fall in aggregate demand causes a recession in which output drops below potential output–the normal level of production given the economy’s resources and technology. This effect is temporary, however. A recession is followed by a recovery period in which output returns to potential, and potential itself is not affected significantly by the recession.

This textbook theory is called into question by Cerra and Saxena (2008), Reinhart and Rogoff (2009), and IMF (2009). These studies examine deep recessions around the world and find highly persistent effects on output. Haltmaier (2012) and Reifschneider et al (2013) argue that these effects occur because a recession reduces an economy’s potential output. Potential output falls because a recession reduces capital accumulation, leaves scars on workers who lose their jobs, and disrupts the economic activities that produce technological progress. Some economists use the term “hysteresis” for these long-term effects of recessions (Blanchard and Summers, 1986).

Experience since the global financial crisis and Great Recession of 2008-2009 has strengthened the evidence for long-term effects of recessions. Reinhart and Rogoff (2014) point out that output in many countries is still highly depressed in 2014, with authorities such as the IMF forecasting little recovery in the next five years. As Summers (2014) puts it: “This financial crisis has confirmed the doctrine of hysteresis more strongly than anyone might have supposed.”

This paper uses OECD estimates of potential output in 23 countries to quantify the long-term damage from the Great Recession. For each country, I take the path that potential output was following before the financial crisis, according to OECD estimates from December 2007, and I extrapolate this path through 2015. I compare this pre-crisis trend to estimates of potential output in the most recent vintage of OECD data (May 2014), and interpret the differences as effects of the recession. To check robustness, I do a similar exercise using IMF estimates of potential output from October 2007 and from April 2014.

I find that the loss in potential output from the Great Recession varies greatly across countries, but is large in most cases. Based on current forecasts for 2015, the loss ranges from almost nothing in Switzerland and Australia to over 30% of potential output in Greece, Hungary, and Ireland. The average loss for the 23 countries, weighted by the sizes of their economies, is 8.4%.

The analysis also yields two related results. First, in most countries the loss of potential output is almost as large as the shortfall of actual output from its pre-crisis trend. This finding implies that hysteresis effects have been very strong during the Great Recession.

Second, in the countries hit hardest by the recession, the growth rate of potential output is significantly lower today than it was before 2008. This growth slowdown means that the level of potential output is likely to fall even farther below its pre-crisis trend in the years to come.

Vir: Ball (2014)

You must be logged in to post a comment.